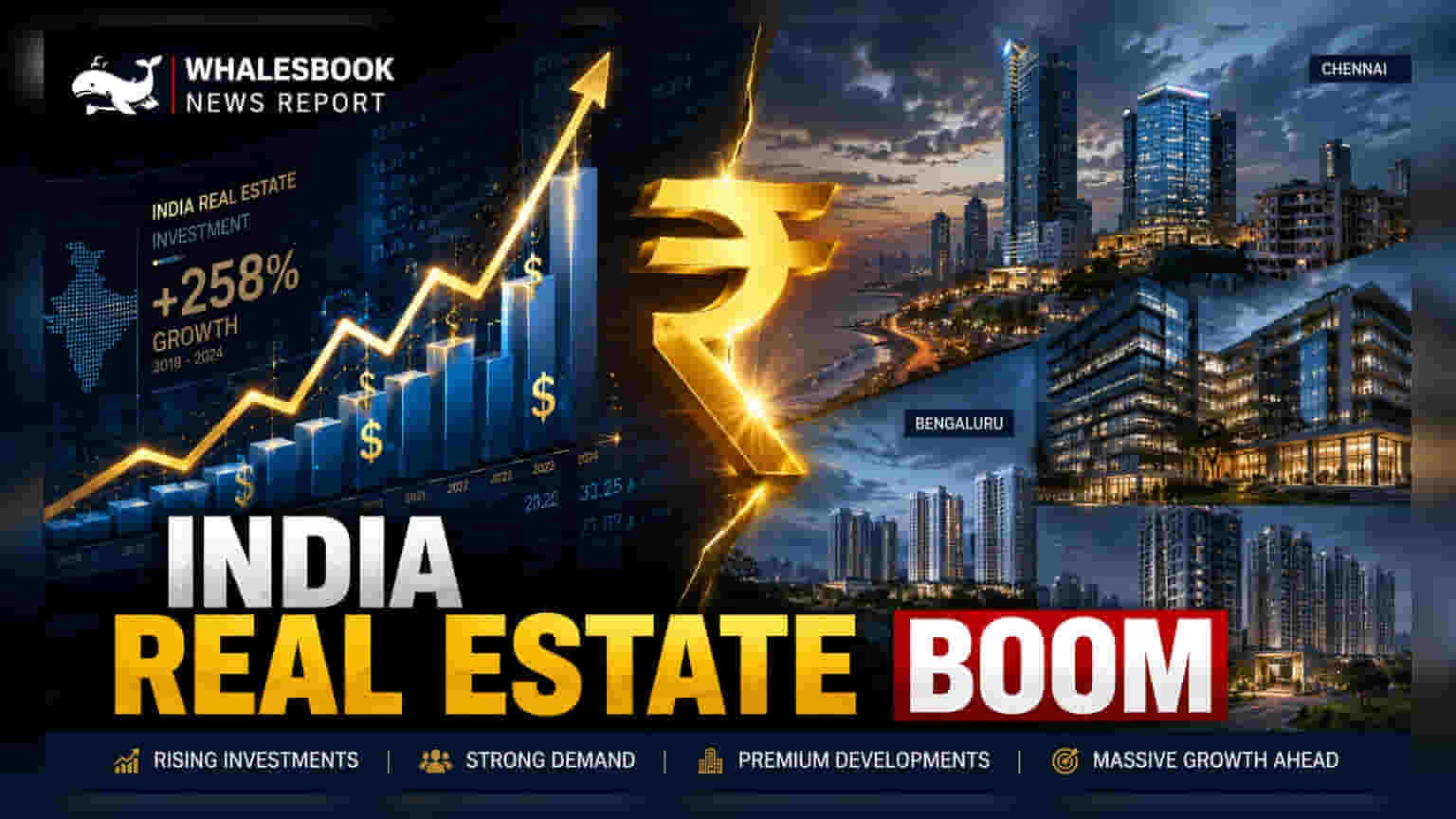

Institutional investment in Indian real estate climbed 70% year-on-year to $2.9 billion in the second quarter of 2026. While the office segment remains a favorite for foreign and domestic capital, residential property investment saw a sharp decline. Domestic investors are playing a larger role, with their contributions doubling to reach $1.33 billion during this period.

What Happened

Institutional capital flowing into the Indian real estate market rose significantly in the second quarter of 2026, reaching $2.9 billion. This marks a 70% increase compared to the same period last year. The growth was driven by a healthy mix of domestic and international funds, with domestic investors taking a more prominent role than in previous quarters. Chennai and Bengaluru have emerged as the most active markets, together attracting roughly 27% of the total investment value during this three-month window.

The Shift Toward Office and Mixed-Use Assets

The office segment continues to be the preferred choice for institutional investors, securing about $1.9 billion in the first half of 2026. This focus accounts for over 40% of total inflows for the half-year. Recent large-scale transactions have highlighted this trend, such as the Abu Dhabi Investment Authority’s $675 million investment in a mixed-use portfolio managed by Kotak Alternate Asset Managers. Additionally, the data center and alternative assets space saw major interest, exemplified by the $440 million investment from the Canada Pension Plan Investment Board into CtrlS.

Residential Segment Faces Pressure

While commercial and office spaces are seeing strong interest, the residential real estate sector is witnessing a decline. Investments in residential projects fell by 43% year-on-year during the first half of 2026, dropping to $0.5 billion. Investors may want to track whether this cooling reflects a change in demand for new large-scale residential projects or if it represents a shift in institutional strategy toward assets that promise more stable, long-term rental or operational returns.

Domestic Confidence and Tier II Growth

One of the most notable takeaways is the doubling of domestic investment, which reached $1.33 billion and now makes up 46% of all institutional inflows. This suggests that local financial institutions and alternative investment funds are playing a larger part in shaping real estate projects. Furthermore, institutional interest is expanding beyond the top metro cities. Regions including Coorg, Hosur, Coimbatore, Kochi, and Ujjain are seeing new capital deployments, particularly in hospitality, warehousing, and industrial segments, as these areas become more integrated into national logistics and tourism networks.

What Investors Should Track Next

Investors should keep an eye on how these inflows translate into project completion timelines and occupancy rates for the office segment. Since office space is currently the main driver of capital, the market's health will depend on sustained demand for commercial space. Furthermore, while the residential sector is currently facing a dip in institutional interest, any policy changes or shifts in home-buying demand could alter this trend in the coming quarters. Monitoring the performance of listed real estate developers and their specific exposure to office versus residential portfolios will be important for understanding how these broad capital trends impact individual company balance sheets.