Private equity inflows into Indian real estate dropped 23% to $1.13 billion in the first half of 2026, according to Knight Frank India. While office assets saw a 33% surge, attracting the bulk of capital, residential funding declined as investors turned cautious. This shift highlights a preference for stable rental yields over development risks in a high-interest-rate environment.

What Happened

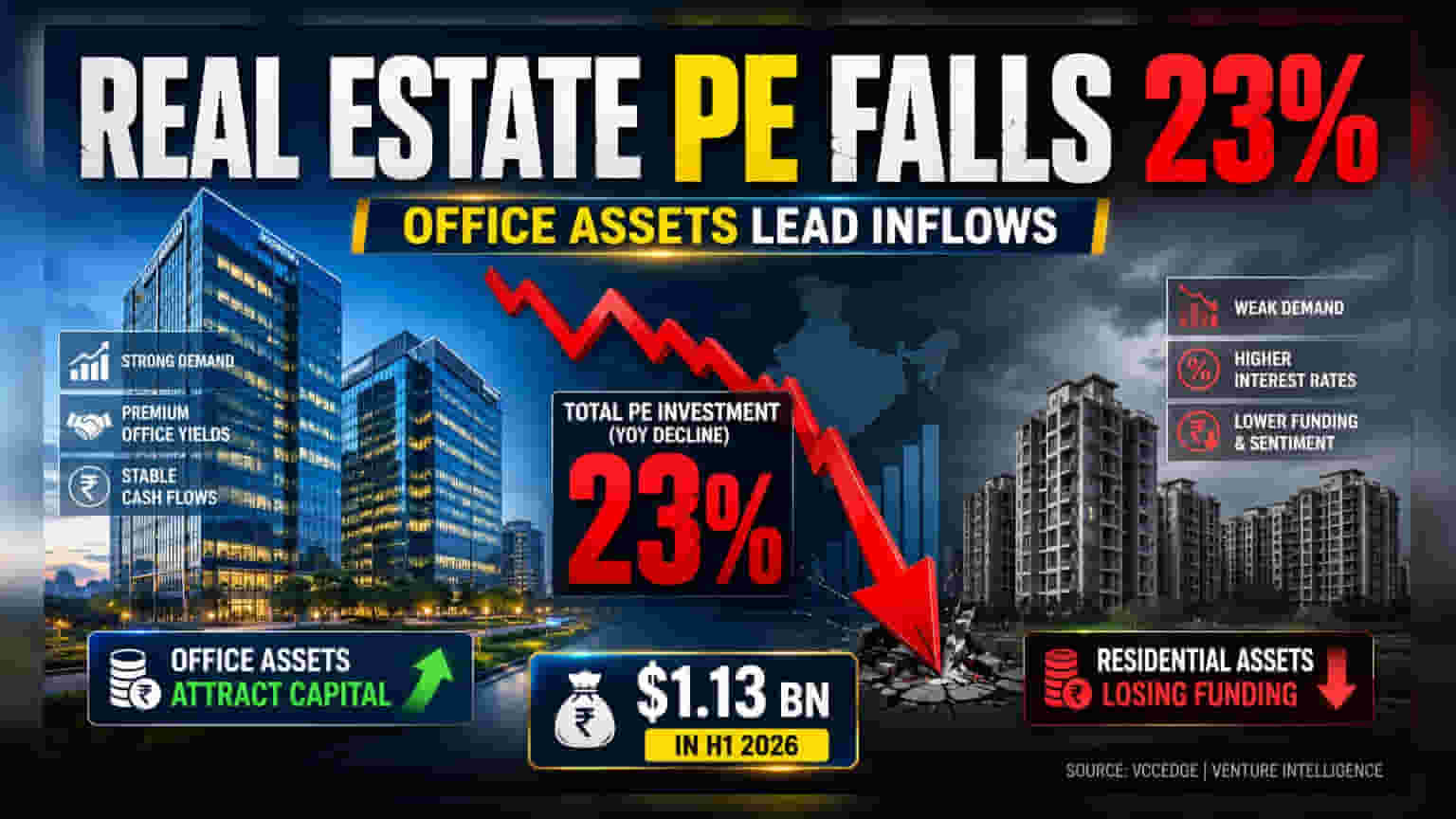

Private equity (PE) investment in the Indian real estate sector witnessed a 23% decline year-on-year in the first half of 2026, totaling $1.13 billion. This figure is lower than the $1.47 billion recorded during the same period in 2025, according to property consultant Knight Frank India. The data highlights a distinct change in how institutional investors are allocating capital, moving away from development-heavy residential projects toward income-generating commercial assets.

The Shift Toward Office Assets

Despite the overall decline in deal value, office properties emerged as the clear favorite for PE investors. Investments in the office segment surged by 33% to reach $998 million, up from $579 million a year earlier. This sector now accounts for nearly 89% of all private equity inflows into Indian real estate. For institutional investors like global pension funds and sovereign wealth funds, office assets offer more predictable and stable returns through long-term lease agreements, which remain attractive even when global interest rates remain elevated.

Why Residential Funding Is Falling

In sharp contrast to the office segment, private equity inflows into residential real estate dropped significantly, falling to $128 million from $297 million in the first half of the previous year. This contraction reflects a more cautious approach by capital providers toward development risks. When global borrowing costs rise, investors typically become stricter about the return profile of projects. Residential development involves higher execution risk, including construction delays and regulatory hurdles, compared to fully leased or pre-leased commercial office spaces.

What This Means For Real Estate Developers

For listed Indian real estate companies, the decline in private equity for residential projects does not necessarily signal a collapse in domestic demand. In fact, many large listed developers in India have moved toward a business model that relies heavily on 'pre-sales'—selling apartments before completion—rather than relying on private equity partners for project funding. By generating cash directly from homebuyers, developers are often able to reduce their reliance on expensive private equity capital, which usually demands a high return on investment. Consequently, while PE interest has moderated, developers with strong track records of delivery may remain financially stable, provided they continue to maintain robust sales velocity.

The Global Capital Context

Knight Frank India noted that the cooling of investment activity is primarily linked to the global capital environment rather than any fundamental weakness in India’s property market. Rising interest rates worldwide have made the 'yield advantage'—the extra return investors expect for taking risks in emerging markets—less attractive. When safe-haven assets in developed markets offer better returns, institutional investors naturally become more discerning, prioritizing liquidity, tax efficiency, and immediate cash flow over long-term capital appreciation.

What Investors Should Track

Investors should keep an eye on how these capital trends affect the balance sheets of real estate companies. Key monitorables include:

- Interest coverage ratios: With higher capital costs, companies with lower debt levels are better positioned.

- Presales velocity: Since PE funding for residential is cooling, developers' ability to self-fund via customer advances is crucial.

- Rental yield trends: As office assets attract the bulk of institutional money, companies with significant commercial portfolios may find it easier to refinance or raise capital through REITs (Real Estate Investment Trusts).

- Execution timelines: Any slowdown in institutional funding could put pressure on developers who are over-leveraged and dependent on external equity to finish ongoing projects.