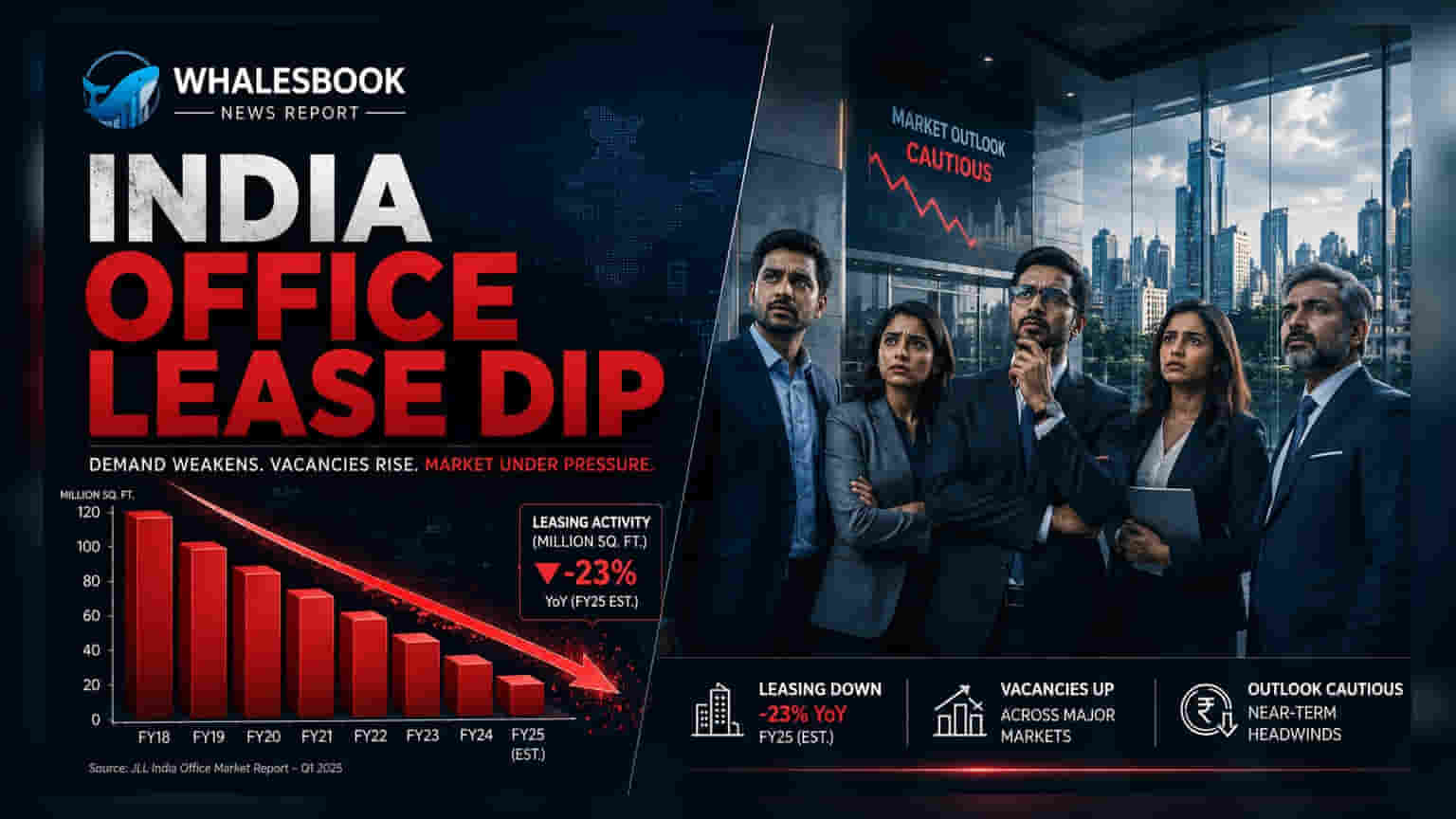

India's major office markets saw gross leasing dip by 1% to 21 million sq ft between April and June 2026. While net leasing fell by 14.5% due to limited prime space availability, demand from Global Capability Centres remains a strong growth driver.

What Happened

India’s commercial real estate market saw a modest contraction in the April-June 2026 quarter. Gross office space leasing across the top eight major cities—including Bengaluru, Mumbai, Delhi-NCR, Pune, Hyderabad, Chennai, Ahmedabad, and Kolkata—totaled approximately 21 million square feet, marking a 1% decline. While this drop appears minor, net leasing, which tracks the actual increase in occupied space, experienced a sharper 14.5% year-on-year decrease, reaching 11.6 million square feet.

Why Supply Is The Main Bottleneck

The decline in leasing activity is not primarily due to a lack of interest from tenants but rather a shortage of high-quality, ready-to-move-in office space. Over the past few years, many developers shifted their capital allocation toward the booming residential real estate market. This strategic preference led to fewer commercial project completions, creating a supply-side constraint that has pushed vacancy rates to low levels and put upward pressure on rental prices.

The Role Of Global Capability Centres

Despite the cooling in leasing volume, demand fundamentals remain resilient. Global organizations continue to view India as a primary destination for expansion, largely driven by the steady growth of Global Capability Centres (GCCs). These centers, which perform core business, IT, and research functions for multinational firms, act as a consistent source of demand for Grade A office spaces. Their continued focus on hiring and expanding operations in India provides a buffer against global macroeconomic uncertainty.

Rental Trends And Developer Strategy

With vacancy rates in prime office clusters tightening, rental growth has remained firm. For commercial real estate developers, this environment suggests that building more prime office space is becoming increasingly profitable. Investors should note that the current leasing dip is largely an issue of supply availability rather than weak demand. As developers begin to shift focus back toward commercial assets to capture higher rentals, a more robust supply pipeline is expected in the coming quarters.

What Investors Should Track Next

For those invested in real estate or property-linked companies, the next important monitorable is the completion schedule of new commercial projects. A faster-than-expected return of supply to the market could ease rental inflation but might also temper the high lease rates currently being commanded. Additionally, investors may observe the leasing pace of major listed commercial developers to see if they are successfully converting their land banks into high-yield commercial assets to meet the sustained demand from GCCs and large corporate occupiers.