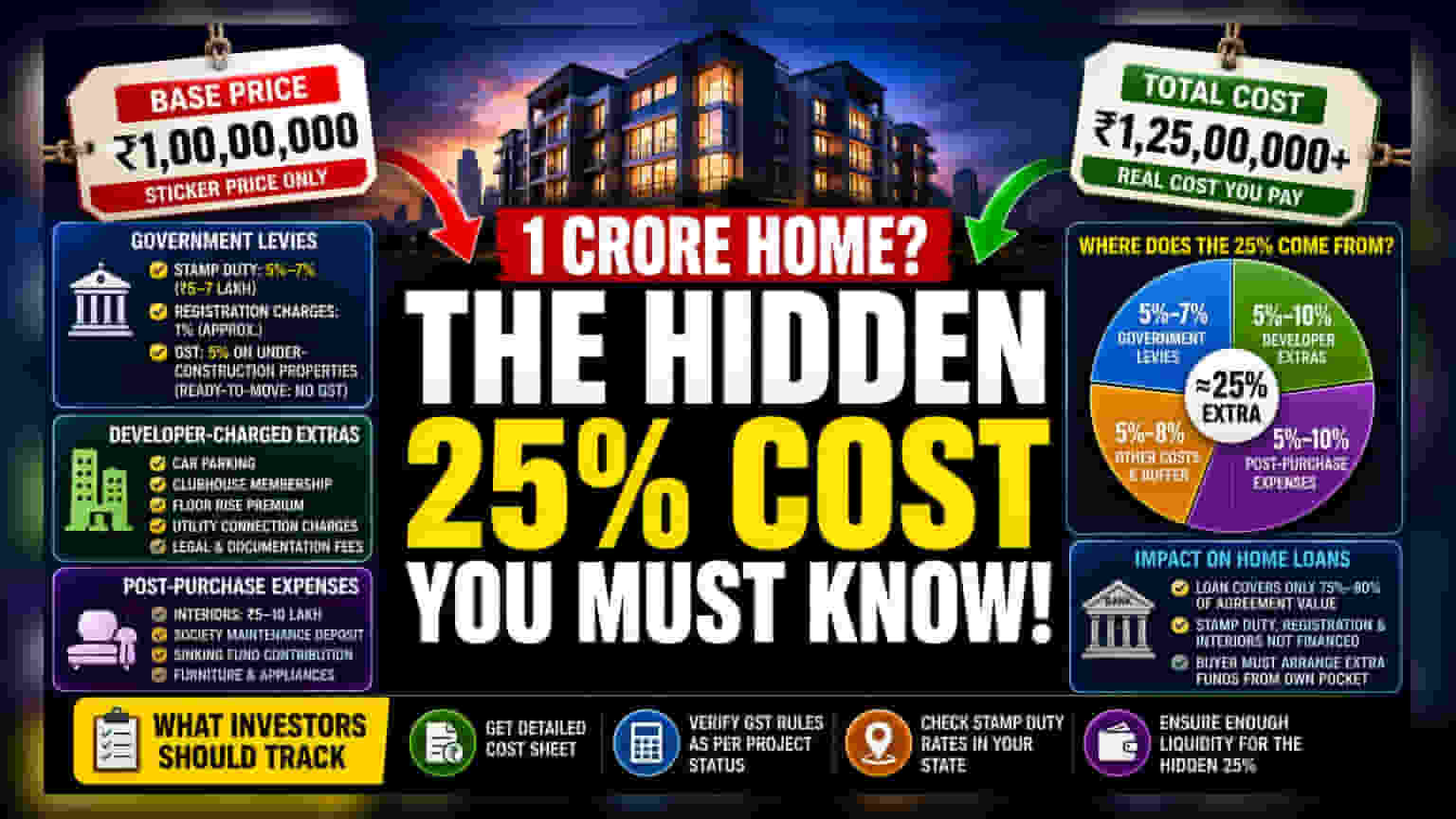

Purchasing a Rs 1 crore property often leads to an actual expense of Rs 1.25 crore due to various hidden costs. From stamp duty and GST to interior fit-outs and parking charges, these add-ons significantly increase the total financial burden. Understanding these components is essential for anyone planning a real estate investment or purchase.

The Gap Between Sticker Price and Final Cost

When looking at property listings, the base price is rarely the final amount a buyer pays. For a home advertised at Rs 1 crore, the total out-of-pocket expense can easily rise to Rs 1.25 crore. This 25% premium is not an accident; it is the result of government levies, developer charges, and necessary post-purchase expenses that are often overlooked until the final payment stage.

Government Levies and Taxes

The most immediate costs upon buying a property are government-mandated fees. Stamp duty and registration charges are required to legally transfer the title of the property. Depending on the state where the property is located, these fees typically range from 5% to 7% of the property’s value. On a Rs 1 crore property, this means setting aside at least Rs 5 lakh to Rs 7 lakh upfront.

Another significant expense for buyers is the Goods and Services Tax (GST). However, this applies differently based on the status of the project. For under-construction properties, GST is generally levied at 5%. Buyers looking at ready-to-move-in homes are often exempt from GST, which can be a major saving. Investors should note that these taxes are usually calculated on the base price and are non-negotiable.

Developer-Charged Extras

Beyond government fees, developers often bundle additional costs into the final price. These may include charges for car parking spaces, a clubhouse membership, or a 'floor rise' premium for units on higher levels of a building. In some cases, developers also add charges for utility connections, such as electricity and water meters, and legal fees. While these are often presented as standard, they are distinct from the basic sale price and should be reviewed in the cost sheet provided by the developer.

The Post-Purchase Burden

Even after the home is registered, the costs continue. Most new properties are delivered in a 'bare shell' state, requiring the buyer to spend on interior design, tiling, electrical fixtures, and furniture. For a standard 2BHK or 3BHK, these costs can range between Rs 5 lakh and Rs 10 lakh, depending on the level of finishing. Furthermore, buyers must account for the initial society maintenance deposit and the sinking fund, which are common practices in residential housing societies.

The Impact on Home Loans

An important factor for investors and homebuyers is how these costs affect home loan eligibility. Banks typically approve loans based on the agreement value of the property, often covering 75% to 80% of the cost. Crucially, most lenders do not fund the stamp duty, registration fees, or the cost of interiors. This means the buyer must arrange for these extra funds out of their own pocket, which requires higher liquidity than the advertised property price suggests.

What Investors Should Track

When evaluating a property, always request a comprehensive cost sheet that separates the base price from all other charges. Check the specific GST rules for the project status and verify the stamp duty rates in that particular state. Finally, ensuring enough liquidity for the 'hidden' 25% is vital to avoid last-minute financing stress.