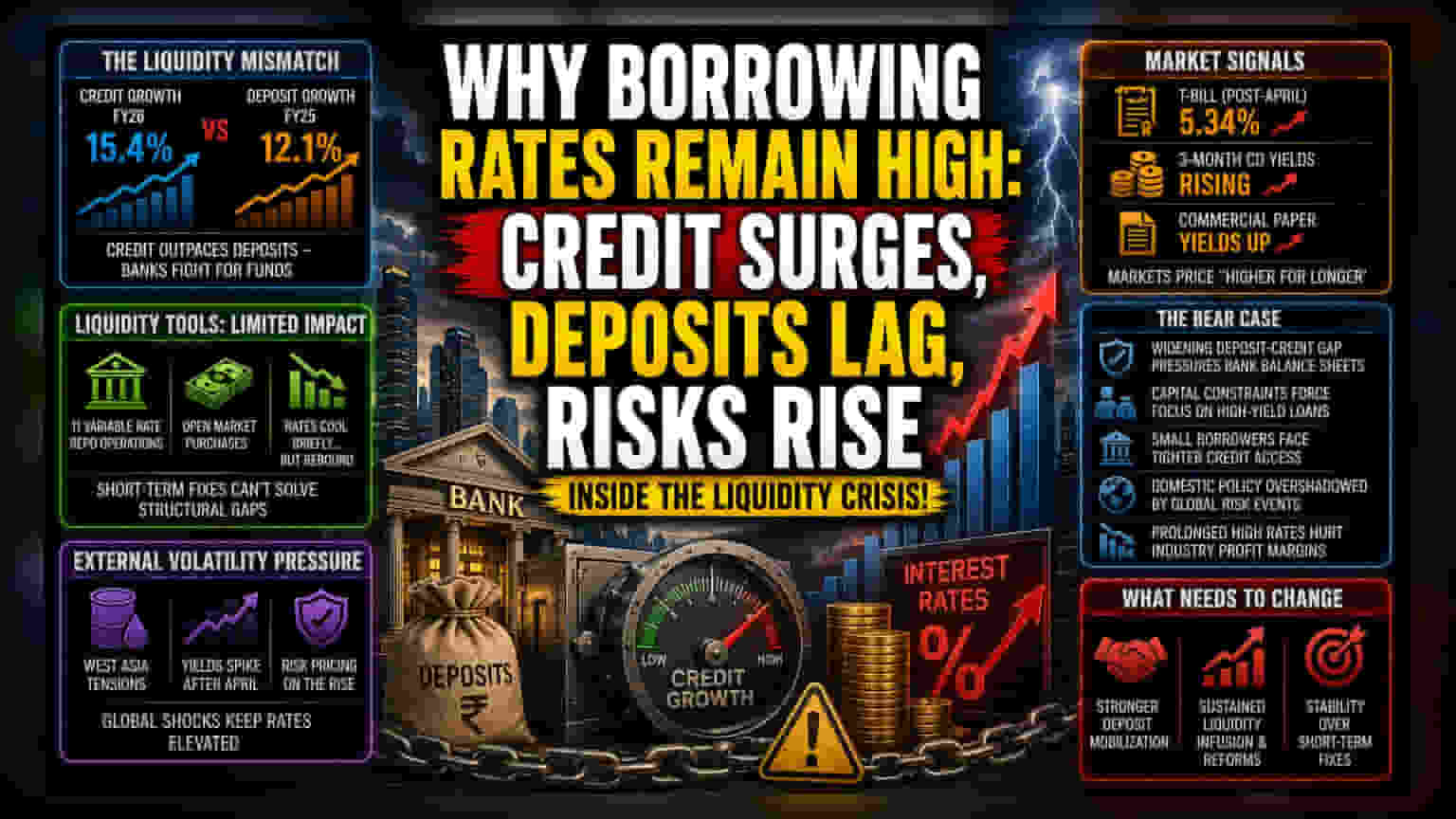

The Structural Liquidity Mismatch

The persistence of high lending rates stems from a fundamental imbalance between the supply of lendable funds and the aggressive appetite for credit. While credit expansion hit 15.4% for the 2026 fiscal year—a significant leap from the 12.1% growth observed in the prior period—the banking system is grappling with a widening deposit mobilization gap. Banks are effectively engaged in a defensive bidding war for household savings, keeping deposit rates high to prevent liquidity depletion. This competitive pressure forces lenders to protect their net interest margins by slowing the transmission of policy rate cuts to the retail and corporate borrowing segments.

The Failure of Liquidity Intervention

The central bank’s efforts to grease the gears of the credit market have faced diminishing returns. Even after executing eleven Variable Rate Repo operations and deploying open market purchases of government securities, the desired softening of rates has been elusive. While short-term market instruments like certificates of deposit and commercial paper showed a brief cooling trend during April, the subsequent reversal in May suggests that market participants are pricing in greater risk. The reliance on short-term liquidity tools has proven insufficient to overcome the structural preference for cash and the rapid pace of loan book expansion at major commercial banks.

The Risk of External Volatility

Geopolitical tremors emanating from West Asia have introduced a fresh layer of uncertainty, causing a sharp repricing of risk across the fixed-income spectrum. This external pressure has caused yields on short-term treasury bills to climb to 5.34% post-April policy, signaling that market expectations for a sustained easing cycle are eroding. The uptick in yields for 3-month certificates of deposit and commercial paper reflects a market that is increasingly hedging against a higher-for-longer rate environment. This volatility poses a direct challenge to the central bank's ability to maintain a balanced growth-inflation trajectory.

The Forensic Bear Case

The current financial architecture reveals a fragile reliance on external liquidity. Should the deposit-to-credit ratio continue to deteriorate, lenders will likely face mounting pressure on their capital adequacy ratios, forcing them to prioritize high-yield loans and further tightening access to credit for smaller borrowers. Moreover, the sensitivity of the Indian credit market to external conflicts suggests that domestic monetary policy is increasingly subservient to global risk-off events. If the current trajectory of credit growth continues to outpace deposits, the central bank may find its liquidity tools entirely blunted, leading to a period of protracted high interest rates that could erode the profit margins of credit-intensive industrial sectors.