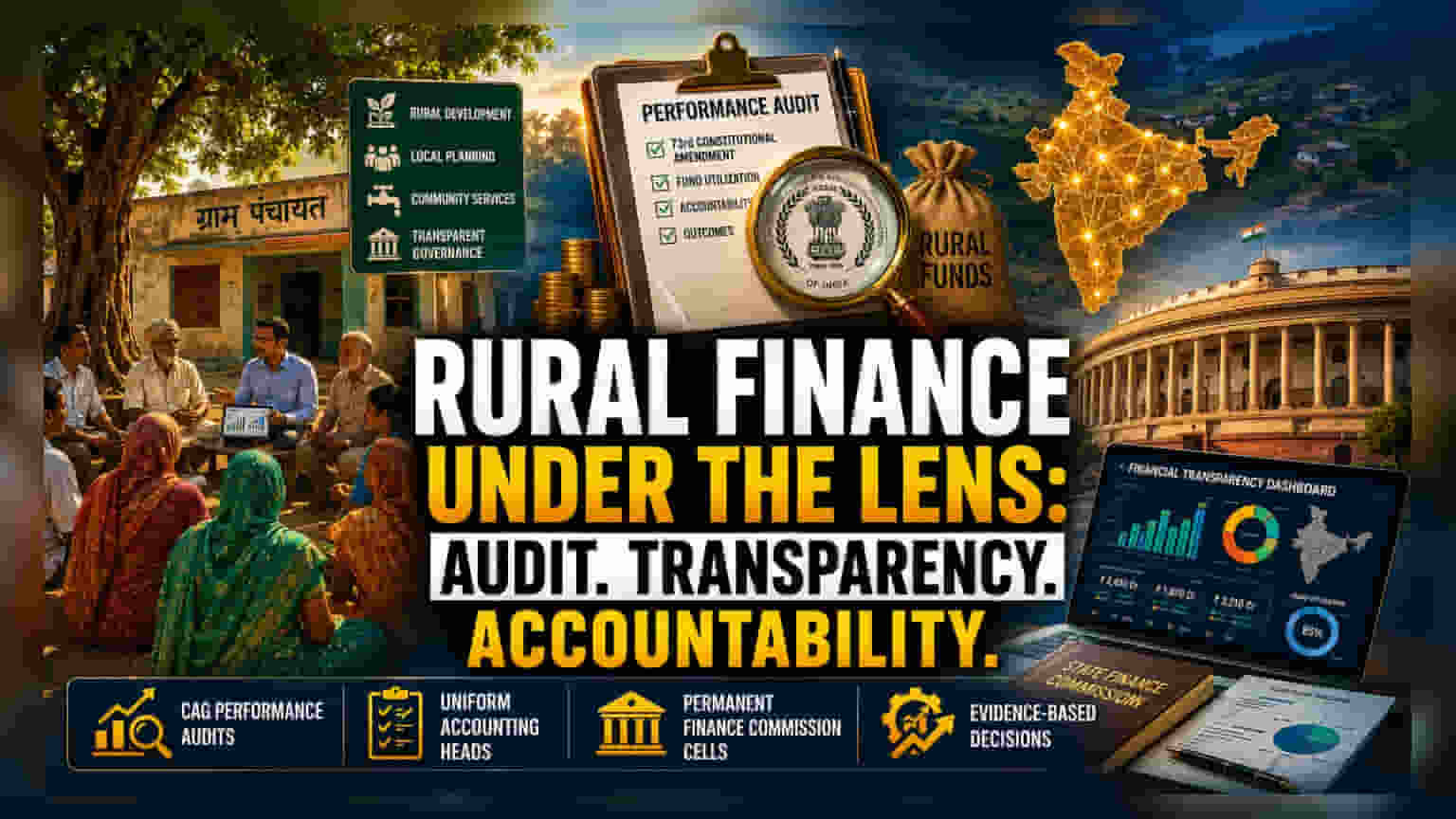

The Shift Toward Fiscal Precision

The push for independent oversight of rural financial flows represents a transition from broad fiscal devolution toward granular accountability. By seeking a comprehensive performance audit of the 73rd Constitutional Amendment, the administration is effectively moving to close a massive information asymmetry that has historically hindered state finance commissions. The current reliance on fragmented data at the gram panchayat level has long been viewed as a structural weakness, preventing a clear assessment of whether central transfers translate into genuine local economic development.

Standardizing State Financial Architecture

The proposed implementation of uniform accounting heads across states is the most significant technical hurdle in this initiative. By aligning disparate state-level reporting structures, the government intends to create a baseline for inter-regional comparison. This is intended to mitigate the current situation where finance commissions often operate without a reliable historical evidence base. Establishing permanent state finance commission cells is viewed as the necessary administrative mechanism to transform these theoretical recommendations into functional, real-time fiscal reporting systems. Without such standardization, central government oversight remains speculative at best, leaving significant portions of rural budget allocations unverified.

The Forensic Bear Case: Structural Implementation Risks

While the mandate for transparency is clear, the practical execution faces severe headwinds. The primary risk is the bureaucratic inertia inherent in local government bodies. Previous attempts to digitize or audit gram panchayat finances have frequently stalled due to a lack of technical personnel and the sheer volume of micro-transactions. Furthermore, there is a risk that additional reporting requirements may inadvertently slow down fund utilization, creating a bottleneck that contradicts the objective of enhancing rural governance. Critics within public policy circles argue that simply adding another layer of auditing without addressing the underlying capacity constraints in village-level administration may lead to a culture of compliance rather than efficiency, where officials prioritize form-filling over developmental impact.

Future Trajectory and Policy Implications

If the Ministry of Panchayati Raj successfully integrates these CAG-led performance audits, the resulting dataset will likely redefine how future devolution of funds is calculated. By quantifying the gap between constitutional intent and administrative output, the government may shift toward performance-based incentives for local bodies. Market observers should watch for potential legislative moves to formalize these accounting cells, as the move toward mandatory transparency will inevitably force states to reconcile their local expenditure data with centralized fiscal objectives.