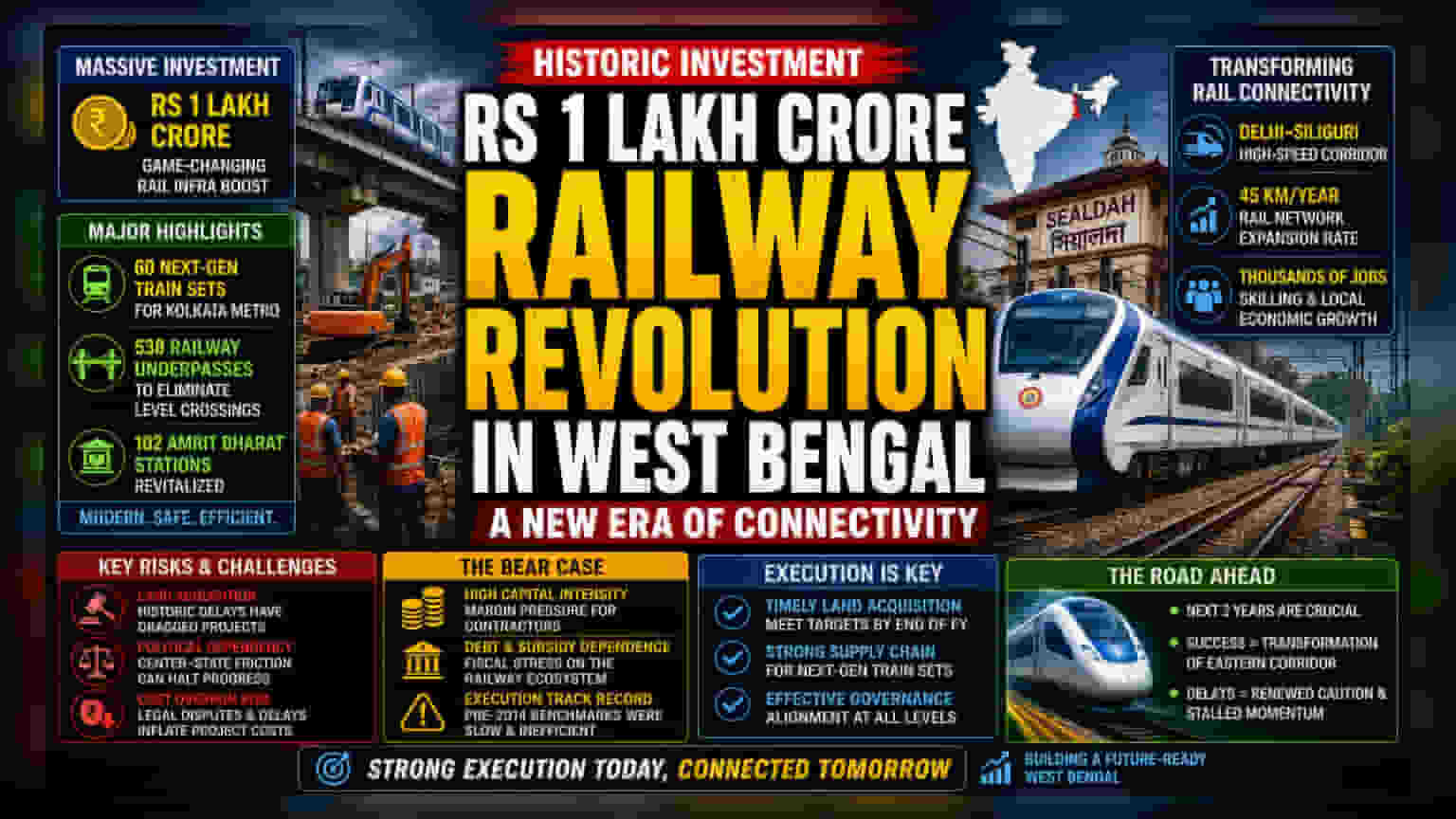

The Capital Expenditure Shift

This aggressive allocation of Rs 1 lakh crore for West Bengal railway infrastructure signals a departure from the fragmented project execution that defined the region for decades. By focusing on systemic modernization, including the introduction of 60 next-generation train sets for the Kolkata Metro, the government is attempting to move beyond maintenance-heavy budgets toward a high-velocity capital deployment model. Market observers note that this funding, while significant, remains subject to the historical volatility of land acquisition timelines in the state, which have traditionally acted as a primary drag on project internal rates of return.

Operational Risks and Execution Hurdles

While the mandate for 538 railway underpasses and the revitalization of 102 Amrit Bharat stations aims to optimize logistics, the success of these projects hinges on administrative alignment. The transition from the previous administration to the current state leadership has clearly prioritized the resolution of land disputes—a move intended to lower the risk premium associated with long-gestation infrastructure investments. Historically, projects in the region have suffered from significant cost overruns stemming from legal challenges and delayed site handovers. Investors are closely watching the newly announced land acquisition schedules to see if they deviate from the sluggish performance benchmarks seen in the pre-2014 era.

The Forensic Bear Case

Despite the optimistic tone surrounding the Delhi-Siliguri high-speed corridor, skepticism remains regarding the feasibility of such massive fiscal outlays amid tightening credit conditions. From an institutional perspective, the reliance on center-state cooperation introduces a political dependency; any future friction between the Railway Board and state authorities could trigger immediate project paralysis. Furthermore, while the current administration highlights a 45 km expansion rate as evidence of success, the sheer capital intensity of high-speed rail projects often leads to margin compression for the primary contractors involved. The market remains wary of whether the current project pipeline can sustain profitability without significant government subsidies or debt-backed financing, which could place further pressure on the broader balance sheet of the Indian railway ecosystem.

Forward Trajectory

Industry consensus suggests that the next two years will be defining for these projects. If the mandated land acquisition targets are met, the focus will likely shift to the supply chain capacity of domestic manufacturers capable of producing next-generation train sets. Failure to secure these sites by the end of the next fiscal year would likely lead to renewed institutional caution, potentially stalling further infrastructure momentum in the Eastern corridor.