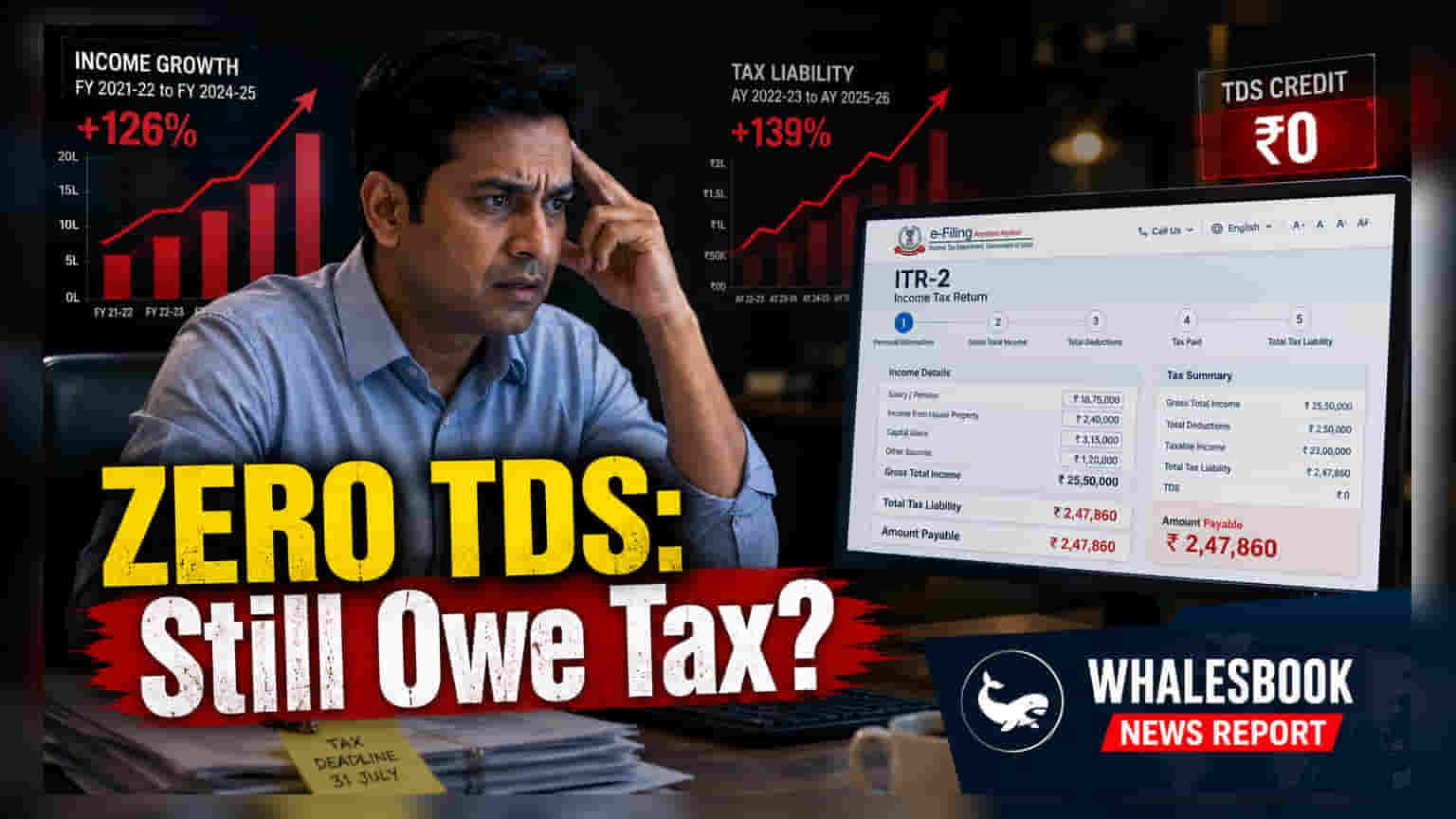

Employees with salaries up to ₹12.75 lakh may see zero TDS, but this does not guarantee a zero tax liability. Filing an Income Tax Return often reveals that secondary income, such as bank interest, pushes total earnings above the rebate threshold.

What Happened

Many salaried taxpayers with annual incomes up to ₹12.75 lakh are finding that their employers are not deducting any Tax Deducted at Source (TDS). This is due to the enhanced rebate limit introduced under the new tax regime in the 2025 budget. While this may look like an tax-free income on the monthly pay slip, it creates a potential misunderstanding regarding total tax obligations. The rebate applies to the total taxable income, not just the base salary processed by the payroll department.

Why Salary TDS Is Not The Full Picture

Employers only calculate TDS based on the salary income they pay out. They apply the standard deduction to arrive at a taxable salary figure. If this resulting amount stays within the threshold for the Section 87A rebate, the employer stops deducting tax. However, the tax department views an individual's financial situation as a whole. When an individual files their Income Tax Return (ITR), they must include all income sources. Any income earned outside of the primary salary—such as interest from savings accounts, fixed deposits, or rental income—is added to the total.

The Impact Of Additional Income Sources

Once secondary income is added, the total taxable income may cross the ₹12 lakh threshold. This can result in an unexpected tax demand during the filing process, even if the employer deducted zero tax throughout the year. It is important to remember that the rebate under the new regime is strictly for total income. Furthermore, income taxed at special rates, such as long-term or short-term capital gains from stock market investments, remains separate and is not covered by the salary rebate mechanism.

Understanding Marginal Relief

When total income marginally exceeds the threshold, the tax system provides a mechanism known as marginal relief. For example, if a gross salary after standard deduction is ₹12.35 lakh, it exceeds the ₹12 lakh limit. While the standard slab calculation might suggest a significant tax payment, marginal relief limits the liability to the amount by which the income exceeds the threshold. Despite this relief, the taxpayer will still owe tax to the government. Relying solely on the absence of TDS from an employer can lead to cash flow issues if a taxpayer is unprepared for this end-of-year payment.

What To Watch Next

For taxpayers, the most important step is to maintain a clear record of all interest certificates from banks and other miscellaneous income throughout the financial year. Before filing, one should estimate their total taxable income, including all non-salary sources, to determine if they qualify for the full rebate. If the total income exceeds the threshold, setting aside funds specifically for the potential tax liability is a prudent practice to avoid financial strain when the ITR deadline approaches.