Traditional retirement savings methods are becoming insufficient due to longer life expectancy, rising medical inflation, and changing career patterns. Investors now require a dynamic approach that focuses on regular portfolio reviews and growth-oriented assets rather than fixed savings targets.

What Happened

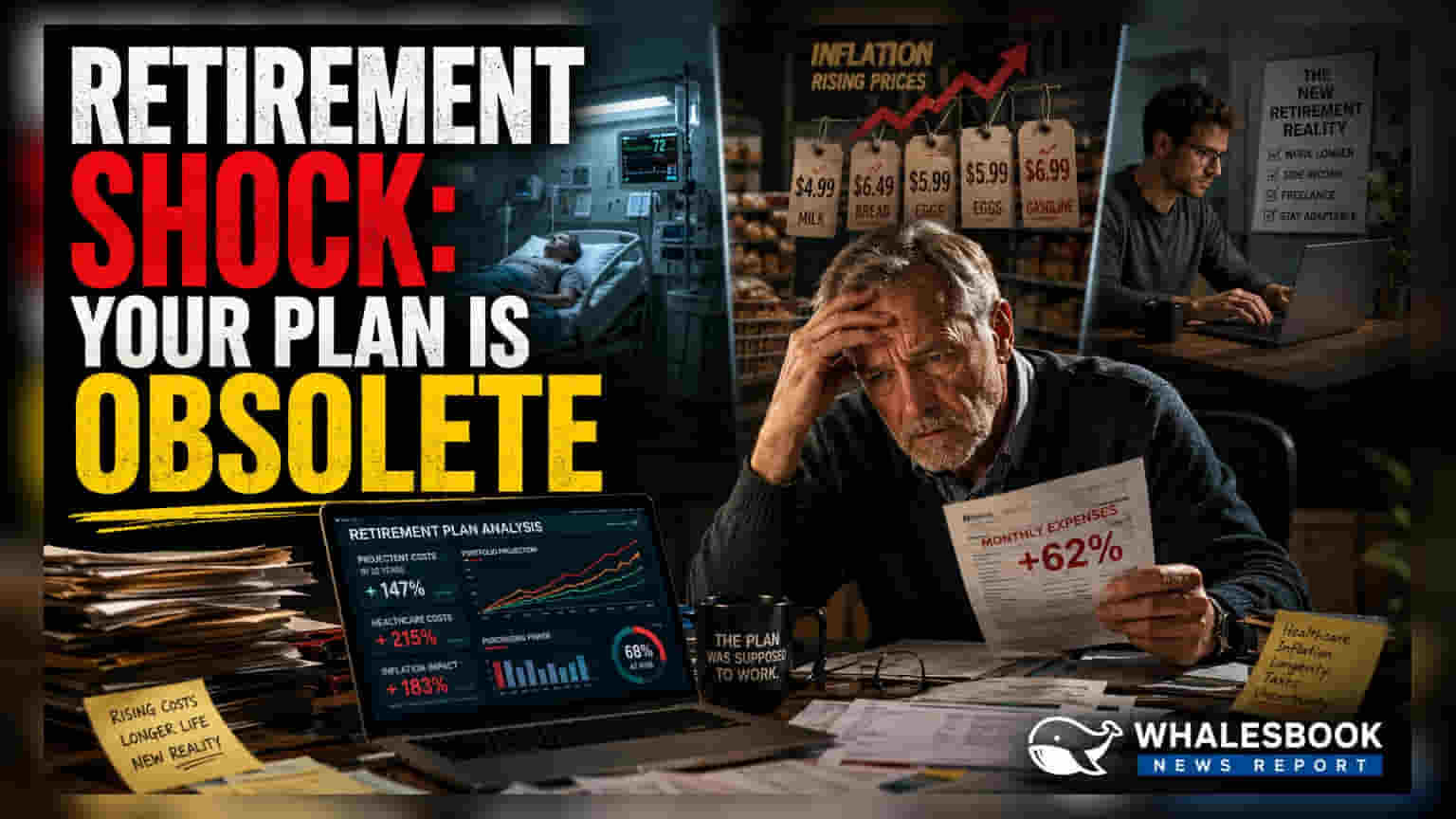

Retirement planning strategies that rely on fixed, static savings targets are increasingly viewed as outdated in the current financial environment. As of July 2026, financial planners are emphasizing that factors such as persistent inflation, longer life spans, and modern, flexible career paths require a more adaptive approach to long-term wealth management. Instead of a one-time setup, retirement planning is becoming an ongoing process that must evolve alongside an individual's changing life circumstances and the broader economic landscape.

The Shift In Retirement Lifestyles

The nature of retirement itself has changed. Many individuals no longer stop working entirely at age 60; instead, they transition into consulting, part-time roles, or freelance work. This flexibility significantly changes how much money one needs to accumulate. A person with an active, post-career income stream requires a different financial cushion compared to someone exiting the workforce completely. Financial planning today is increasingly focused on aligning investments with these specific, evolving lifestyle choices rather than rigid age-based milestones.

Why Healthcare And Inflation Matter

Rising healthcare costs and the steady erosion of purchasing power due to inflation are the two biggest risks to a retirement corpus. Medical expenses often grow faster than general inflation, meaning that retirees who do not account for these costs separately risk depleting their savings far sooner than expected. Similarly, money saved today will lose value over time. To combat this, modern strategies prioritize growth-oriented assets, such as equities for younger investors, to ensure the portfolio beats inflation over the long run.

The Importance Of Portfolio Rebalancing

Most financial experts suggest a transition in asset allocation as an investor nears retirement age. While a younger investor can afford the volatility associated with growth assets to build wealth, an older investor typically shifts toward safer debt instruments to preserve capital. However, this shift is no longer viewed as a static event. It now requires periodic reviews to ensure that the balance between growth and safety remains appropriate for current market conditions and individual risk tolerance.

What Investors Should Track Next

For those managing their own retirement planning, the focus should shift from a 'set and forget' mentality to active management. Investors may track whether their contributions are increasing in line with their income growth and if their health insurance coverage is sufficient to handle future medical inflation. The most important monitorable is the regular review process: adjusting goals when life events occur, such as a career change or a major increase in living expenses, is more effective than sticking to an outdated financial plan.