Navigating tax rules for the FY 2025-26 filing season requires clarity on Section 87A. Learn how the new and old tax regimes offer different rebate limits, how marginal relief protects taxpayers slightly above the threshold, and what the transition to Section 156 means for the coming financial year.

What Happened

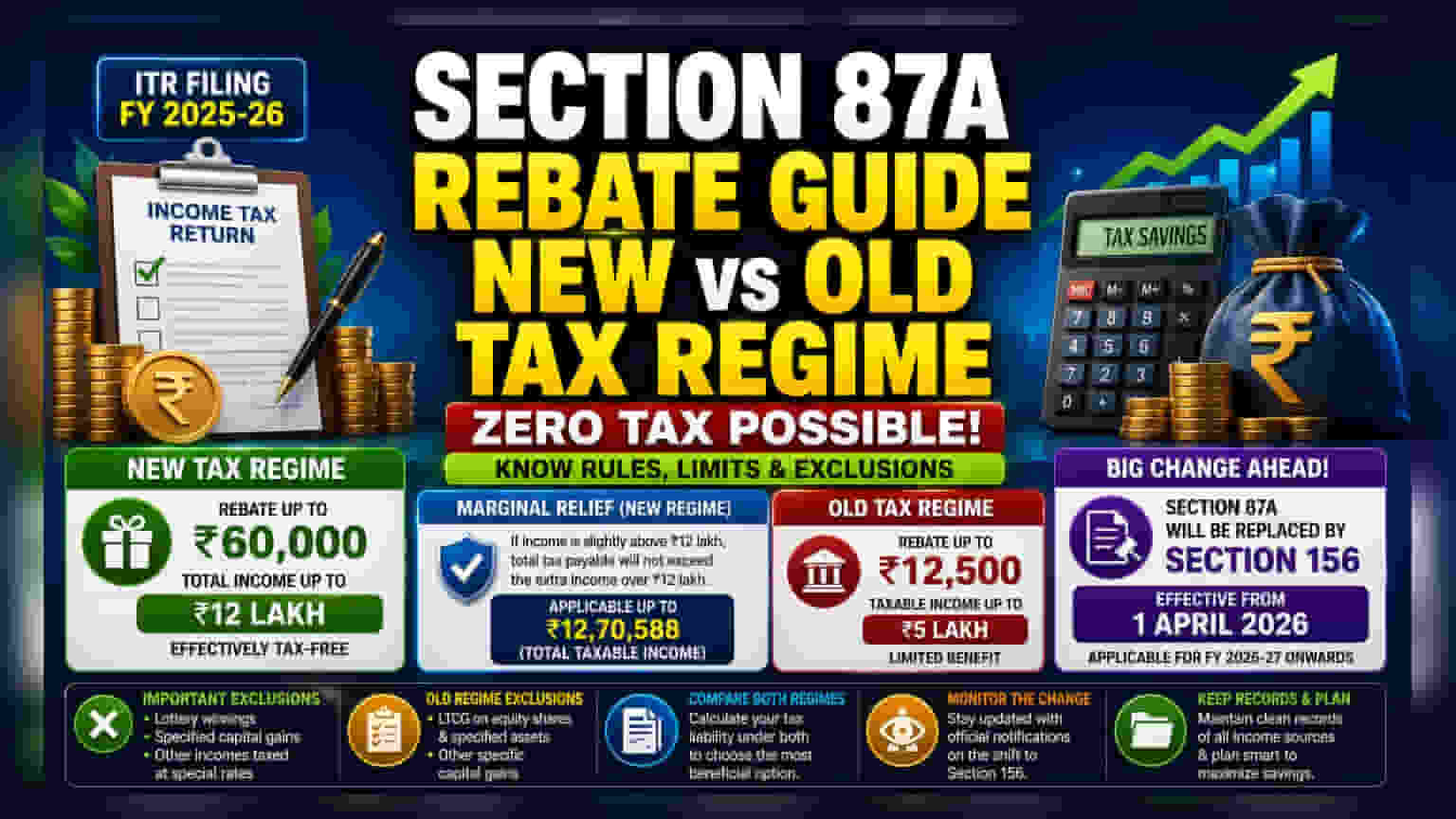

As taxpayers begin the process of filing their Income Tax Returns (ITR) for the financial year 2025-26, understanding the Section 87A rebate is essential. This provision allows resident individuals to lower their total tax liability, in some cases bringing it down to zero. The specific rules and limits for this rebate differ significantly depending on whether a taxpayer chooses the new tax regime or the old tax regime. This distinction is vital for accurate tax planning and compliance during the current filing season.

Comparing New and Old Tax Regimes

The newer tax regime provides a more generous rebate structure compared to the traditional old regime. Under the new regime, taxpayers can claim a rebate under Section 87A if their total income is up to Rs 12 lakh. This effectively makes that income tax-free, as the rebate can be as high as Rs 60,000, covering the tax liability for that income bracket.

Conversely, the old tax regime maintains a more restricted benefit. Individuals opting for this system can claim a rebate of up to Rs 12,500, provided their taxable income does not exceed Rs 5 lakh. Taxpayers should carefully calculate their potential liability under both regimes to see which best fits their specific income and investment profile before finalising their ITR.

How Marginal Relief Works

Taxpayers whose income slightly exceeds the Rs 12 lakh limit in the new regime are not automatically disqualified from all benefits. A provision for marginal relief exists to protect those earning slightly more than the threshold. This rule ensures that the total tax payable does not exceed the extra amount of income earned over Rs 12 lakh. However, this relief is only applicable if the total taxable income remains below Rs 12,70,588. This acts as a safeguard against a sudden, disproportionate tax burden for those just above the rebate cutoff.

Important Exclusions to Remember

The Section 87A rebate is not a blanket waiver for all types of income. Certain earnings are taxed at special rates and are excluded from this benefit. For instance, in the new regime, income from sources like lottery winnings or specific capital gains does not qualify for the rebate. Similarly, under the old tax regime, long-term capital gains from equity shares and other specific assets are often excluded from the rebate calculation. Taxpayers should ensure they account for these exclusions to avoid errors in their tax computations.

The Shift to Section 156

A critical update for taxpayers is the scheduled change in tax law. The provisions currently governed by Section 87A are set to be replaced by Section 156 of the Income Tax Act. This transition takes effect from April 1, 2026, meaning it will impact tax planning and filings for the financial year 2026-27 onwards. Taxpayers should be aware of this shift as they plan their financial strategy for the next year, as the rules governing rebates will evolve under the new section.

What Taxpayers Should Monitor

The most important monitorable for individuals is the upcoming change in tax law for the next financial year. While filing for FY 2025-26, it is useful to track official government notifications and updates regarding how the transition to Section 156 will work in practice. Maintaining clean records of all income sources and understanding the specific exclusions under the current regime can help in accurate filing. Those planning their finances should keep an eye on how these legal changes might influence their take-home pay in the coming year.