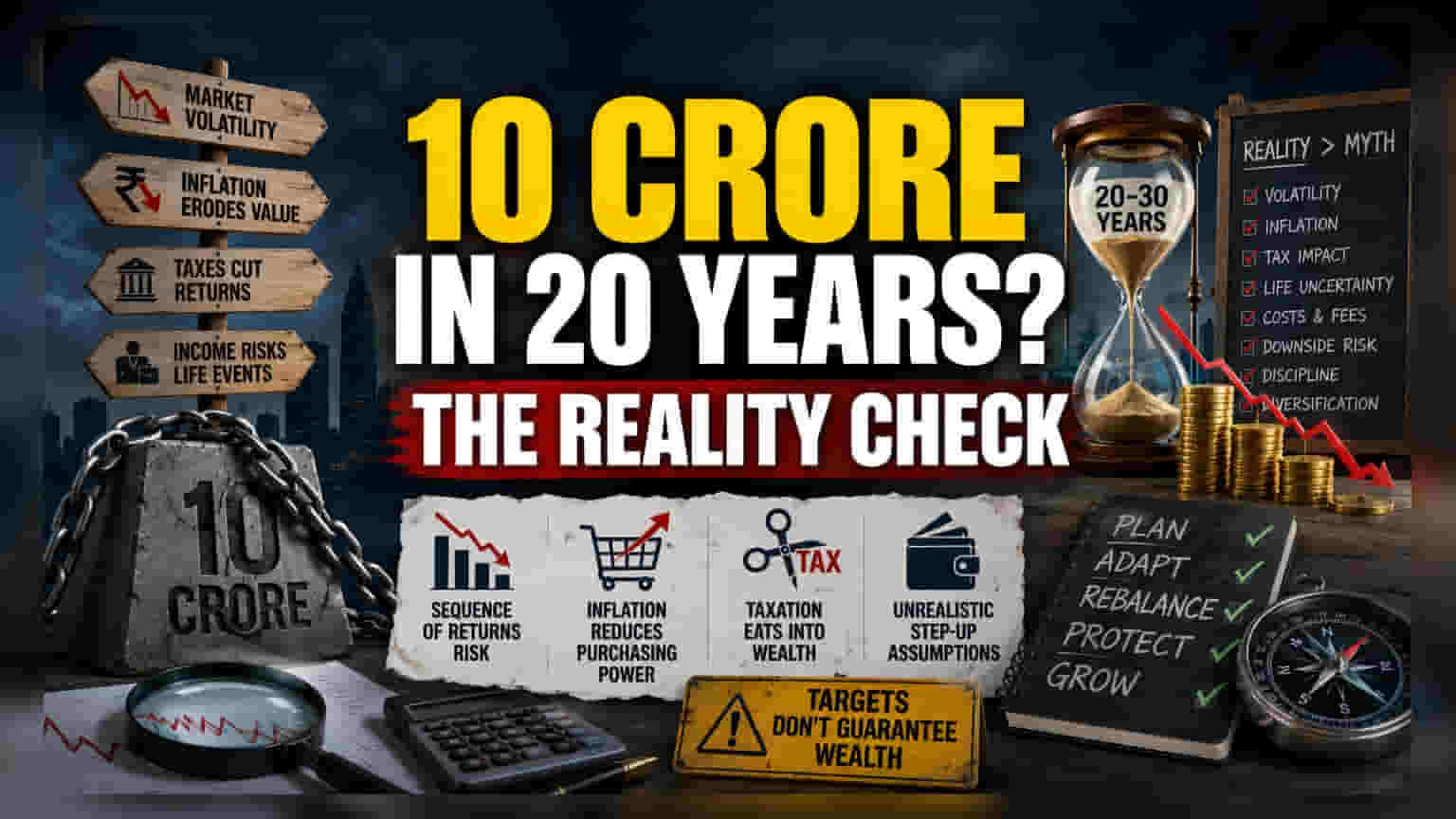

The Illusion of Static Yields

Financial planning narratives frequently lean on the convenience of a flat 12% annual return to illustrate the ease of building a 10-crore portfolio. However, this benchmark fails to account for the real-world variance of equity markets. Over a two-decade horizon, investors rarely experience a linear progression of returns. Instead, portfolios are subjected to volatility clusters where significant drawdowns can occur precisely when the corpus is at its largest. Relying on average annual percentage gains ignores the sequence of returns risk, which posits that a market crash in the final years of an investment journey has a disproportionately devastating impact on the final valuation compared to the initial years.

The Inflation and Tax Headwind

Beyond market volatility, the purchasing power of a 10-crore target in 20 or 30 years will look drastically different than it does today. If one assumes a conservative 6% long-term inflation rate, the actual value of a 10-crore corpus after two decades shrinks significantly in real terms. Furthermore, the math often overlooks the friction of taxation. Capital gains tax on equity mutual funds continues to evolve, and assuming gross returns without considering the impact of long-term capital gains tax—or potential future hikes in wealth or inheritance taxes—creates a dangerous optimism bias. Investors often underestimate how these silent killers erode net wealth over long horizons.

Structural Weaknesses in the 'Step-Up' Model

The strategy of a 10% annual step-up assumes that an investor’s income growth will reliably outpace their cost of living for thirty consecutive years. This ignores the reality of career volatility, medical emergencies, or periods of economic stagnation where an individual might be forced to halt or reduce contributions. Unlike the idealized calculations presented in typical advisory columns, real-world accumulation is non-linear. Individuals often face higher liquidity needs in their middle years, such as housing costs or education funding, which frequently conflict with the requirement to increase investment amounts during the exact phases where compounding should be working the hardest.

The Management of Risk

Modern financial health is better measured by risk-adjusted performance rather than raw target-based speculation. Professional fund managers frequently underperform broad market indices over extended periods, meaning that the costs associated with active management can further drag down the net corpus. Investors chasing a specific target figure often neglect to diversify into non-correlated assets, leaving them vulnerable to a sector-specific downturn that could stall progress for years. Focusing solely on the end goal encourages a passive approach, whereas institutional success relies on active rebalancing and constant recalibration against changing macro-economic realities.