Paying only the minimum due on credit cards keeps accounts in good standing but triggers high interest charges on the remaining balance. This practice traps borrowers in a cycle of debt, significantly increasing the total cost of credit. Understanding how interest compounds on unpaid balances is essential for managing personal financial health.

What Happened

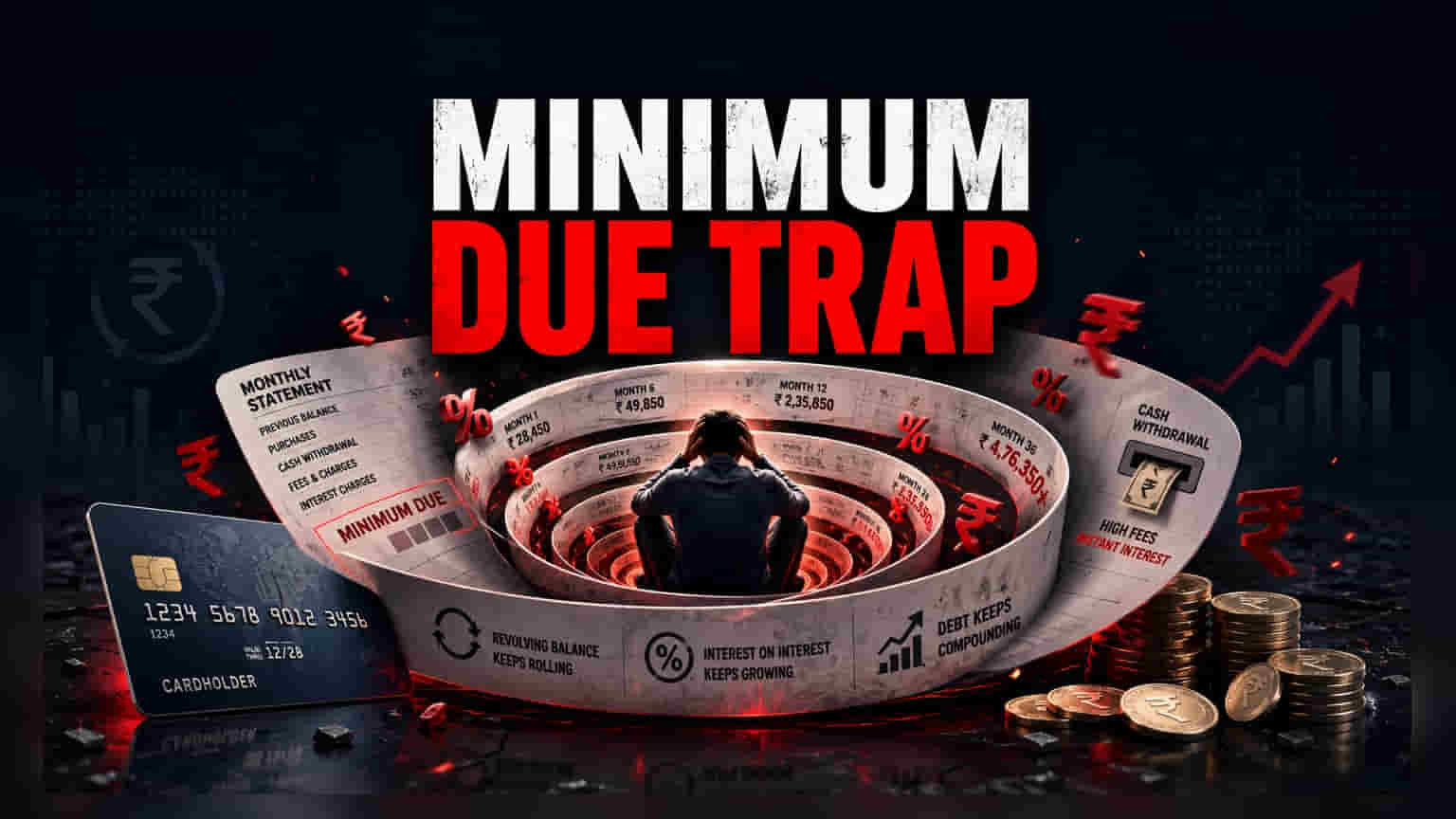

When credit card users pay only the minimum amount requested on their monthly statement, they are essentially choosing to carry over the remaining debt to the next billing cycle. While this prevents late payment fees and keeps the card account in good standing, it activates the interest calculation mechanism on the outstanding balance. The minimum payment, often set between 5% and 10% of the total, covers only a fraction of the debt, leaving the bulk of the principal amount to accrue high-interest charges.

The Business Model Behind the Debt

For credit card issuers and banks, the interest generated from "revolving credit"—debt that is not paid off in full—is a significant revenue stream. This is why credit cards are marketed with features like rewards and cashback, which can sometimes distract users from the underlying cost of carrying a balance. From a banking perspective, a customer who pays only the minimum is considered a "revolver" rather than a "transactor" (someone who pays the full balance every month to avoid interest). Revolvers pay substantial interest, which forms a core part of the return on assets for many card-issuing financial institutions.

How Interest Compounds

Once a user misses paying the full statement balance, the "grace period" on new purchases often disappears. This means that interest begins to accrue on both the old unpaid balance and any new purchases made during the cycle. Because credit card interest rates in India are often quite high, this compounding effect can lead to a situation where the borrower is paying mostly interest rather than reducing the principal debt. This prolongs the repayment period for months or even years, often costing the borrower significantly more than the original value of the purchases made.

The Cash Withdrawal Danger

It is vital to distinguish between standard purchases and cash withdrawals. Credit card issuers typically apply interest on cash withdrawals from the very first day, often with additional transaction fees. Unlike standard retail purchases, which may have an interest-free period, cash advances do not. Using a credit card to withdraw cash when one is already struggling with minimum payments exacerbates the debt burden immediately, as the interest clock starts ticking instantly and usually at a higher rate.

Financial Monitorables for Borrowers

To avoid falling into a revolving credit trap, borrowers should prioritize paying the full statement balance by the due date. If that is not possible due to financial constraints, paying significantly more than the minimum amount is the most effective way to reduce the principal and lower the total interest paid. Investors and individuals should monitor their credit utilization ratio—the percentage of total credit limit used—as high utilization combined with partial payments can also negatively impact credit scores, making it harder to access credit or loans in the future.