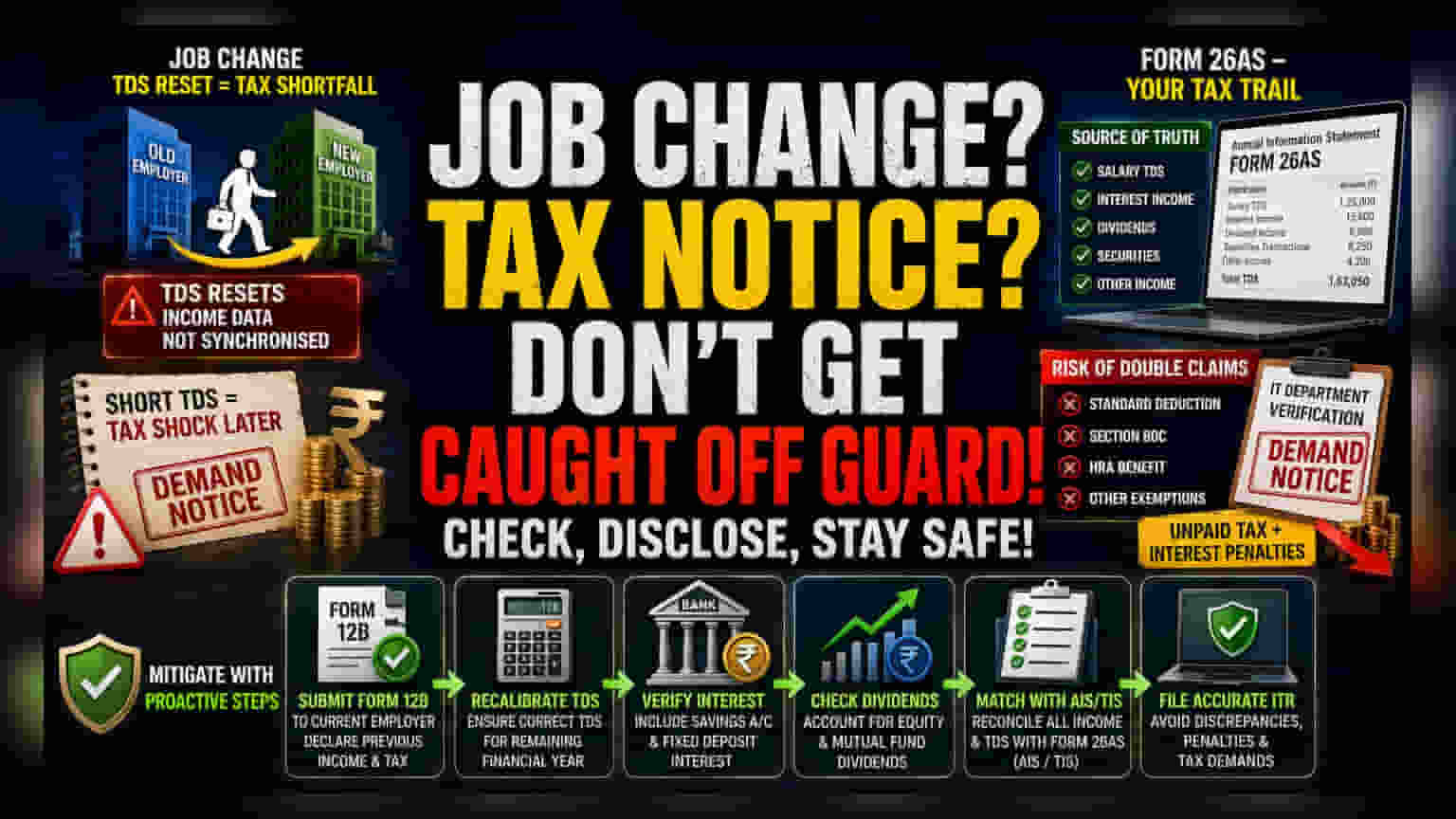

The Synchronization Deficit

The primary driver of tax-related friction for mobile talent is the failure to reconcile bifurcated income streams. When an individual transitions between employers, the tax-deduction calculation often resets, leading to a shortfall in the total Tax Deducted at Source (TDS). This oversight is not merely a documentation error but a structural failure in how income is reported to the tax authorities. Because each employer operates in a silo regarding your fiscal history, the responsibility to bridge this gap falls entirely on the taxpayer.

The Data Trail of Form 26AS

Modern tax compliance relies on the precision of the Annual Information Statement and Form 26AS. These digital repositories act as the source of truth for the Income Tax Department, capturing everything from interest income to securities trades. When a taxpayer submits an Income Tax Return that deviates from the figures populated in these statements, it immediately flags the return for verification. The most common discrepancy involves the failure to account for TDS credits from a previous employer, which, if not manually integrated, leads to an inflated tax liability and potential double-taxation on the same income slice.

Structural Risks of Double Claims

A critical, often overlooked vulnerability during job transitions is the duplicate claim of standard deductions or Section 80C exemptions. Because many payroll systems automate these deductions, an employee moving mid-year might unintentionally benefit from these thresholds twice. When the Income Tax Department performs a cross-verification against your Permanent Account Number, these irregularities stand out. This often results in a formal demand notice for the unpaid tax amount, plus interest penalties that accrue from the end of the assessment year.

Mitigation Through Proactive Disclosure

Taxpayers can mitigate these risks by proactively submitting Form 12B to their current employer. This document serves as a formal declaration of previous earnings and tax payments, allowing the payroll department to recalibrate the TDS for the remainder of the year. Beyond salary, individuals must ensure that interest from high-yield savings accounts and dividends from equity portfolios are manually verified against the Taxpayer Information Summary. Relying solely on employer-provided documents is a strategy destined for failure in an era of automated, data-driven tax assessment.