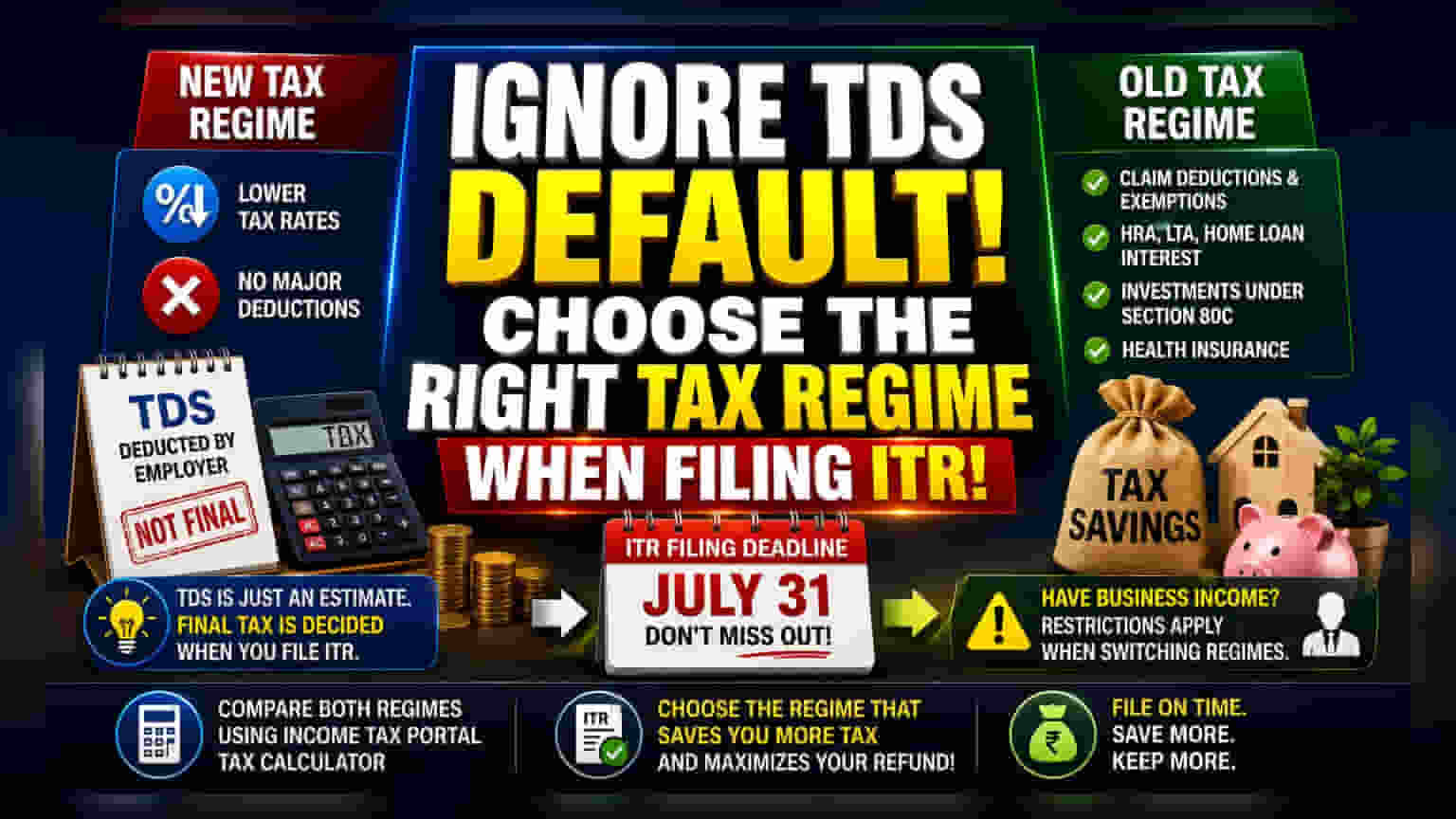

If your company deducted tax based on the new tax regime, you have not lost your chance to save tax. You can still opt for the old tax regime when filing your Income Tax Return (ITR) to claim deductions for HRA, LTA, and investments under Section 80C. Your final tax choice is made by you during the ITR filing process, not by your employer's initial tax deduction calculation.

What Happened

Many salaried employees have faced confusion this financial year because employers are defaulting to the new tax regime for calculating Tax Deducted at Source (TDS) on salaries. If an employee did not explicitly inform their employer about their preferred tax regime, the employer automatically calculates tax using the new tax regime. This has led many to worry that they have missed out on claiming common tax-saving deductions such as House Rent Allowance (HRA), Leave Travel Assistance (LTA), and investments under Section 80C or health insurance premiums.

The Difference Between TDS and ITR

It is important for taxpayers to understand that the tax calculation done by an employer for TDS purposes is not final. The actual tax liability for the year is determined only when you file your Income Tax Return (ITR). Your employer’s TDS deduction is simply an estimate of the tax you may owe. When you sit down to file your ITR, you have the freedom to select the tax regime that best suits your financial situation, regardless of which regime your employer used to deduct taxes from your salary during the year.

Why This Matters For Your Savings

The choice of tax regime directly impacts your total tax outgo. The new tax regime generally offers lower tax rates but does not allow for most deductions and exemptions. In contrast, the old tax regime allows you to reduce your taxable income by claiming deductions for expenses like rent, home loan interest, and specific investments like PPF, LIC, or ELSS. If you have significant investments or expenses that qualify for deductions, opting for the old regime at the time of filing your ITR could result in a lower total tax liability and a potential tax refund.

The Business Income Caveat

While salaried individuals without business income have the flexibility to switch between regimes every year, there is a restriction for those who have income classified as Profits and Gains of Business or Profession. If you have business income and choose to opt out of the new regime to use the old one, you may face restrictions on how often you can switch back and forth. Always check your income sources carefully before finalizing your choice. For the vast majority of pure salaried employees, this restriction does not apply.

What You Should Monitor

The most important date to keep in mind is the ITR filing deadline, which is July 31st for most individual taxpayers. You must file your return by this date to exercise your choice of tax regime. If you fail to file by the deadline, you will lose the chance to choose the old regime for that financial year, and your tax will be assessed under the default new tax regime. Before filing, compare your total tax liability under both the new and old regimes using the income tax portal's tax calculator to see which option saves you more money.