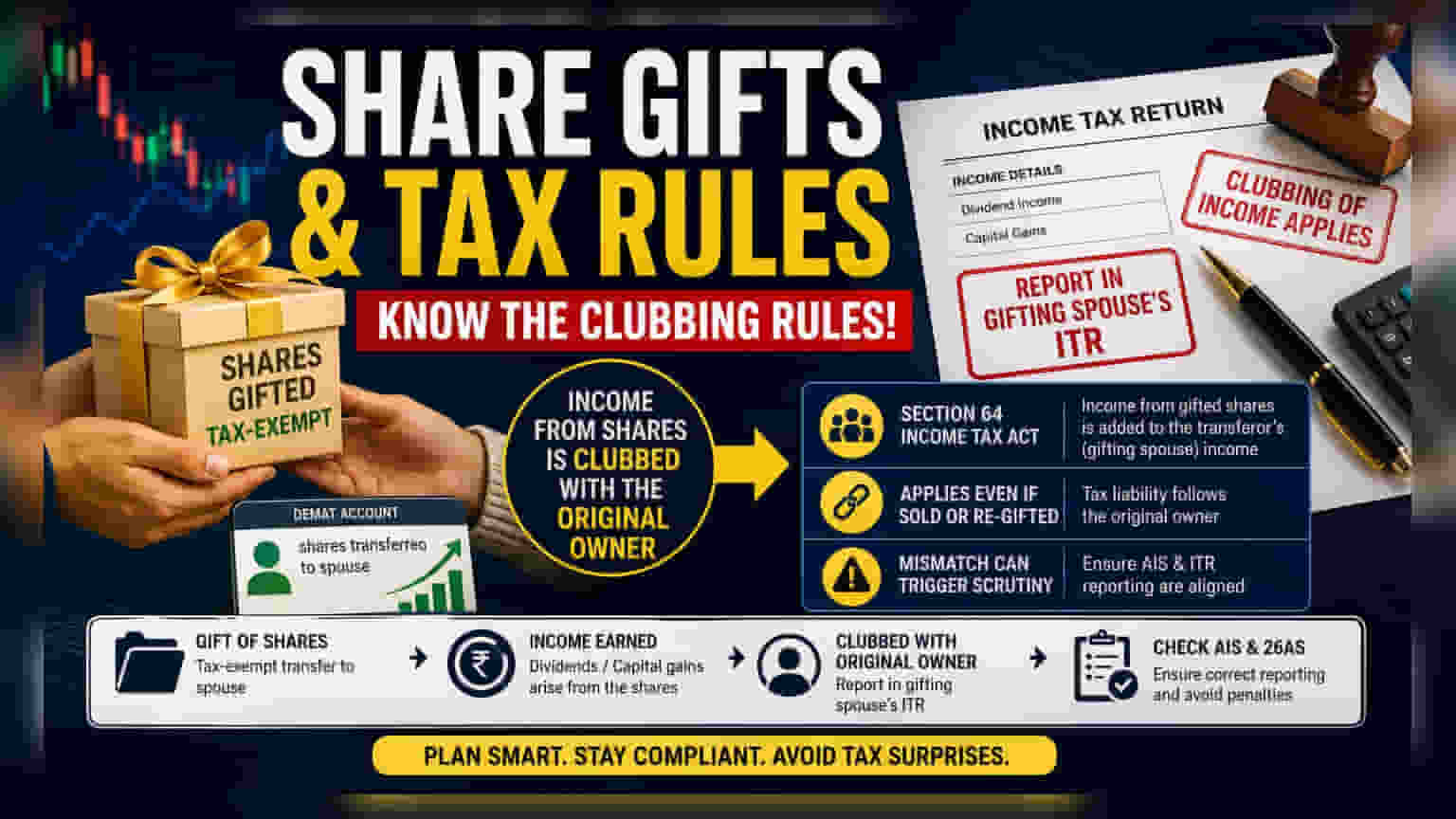

Gifting shares to a spouse is tax-exempt, but income earned from those shares is taxed as the original owner's income under the Income Tax Act's clubbing provisions. Failing to report this income in your tax return can lead to compliance issues and potential penalties during tax assessments.

What Happens With Share Gifts

Many investors transfer shares to their spouse for family planning or wealth distribution purposes. While the transfer of shares itself as a gift is tax-exempt under the Income Tax Act, the subsequent income generated from these assets creates a unique tax requirement. This process, often misunderstood, is governed by the 'clubbing of income' provisions. Even if the shares are officially transferred to the spouse’s demat account, the tax authority views the income generated—such as dividends or capital gains—as belonging to the original owner who gifted the shares.

Understanding the Clubbing Provision

Under Section 64 of the Income Tax Act, income arising from assets transferred to a spouse without adequate consideration is added, or 'clubbed,' to the income of the transferor. This means the original owner must report these earnings in their own Income Tax Return (ITR). This rule remains active even if the recipient spouse sells the shares and re-invests the money elsewhere. The tax responsibility remains with the original gifting spouse, and this applies regardless of whether the funds are kept separate or used for personal expenses.

Why This Matters for Tax Filing

Taxpayers often overlook the importance of matching their reported income with the information available in the Annual Information Statement (AIS). When shares are gifted, the transaction appears as an 'off-market transfer' in the records. If the recipient spouse reports the dividend or capital gains, it creates a mismatch because the tax department expects that income to appear in the gifting spouse's tax filing. Failing to align your income reporting with these rules can trigger scrutiny from tax authorities, potentially leading to demands for unpaid tax, interest, or penalties if the income is found to have been understated.

The Risk of Re-Gifting

An important aspect of these provisions is that they apply even to subsequent transfers. If a spouse receives shares as a gift and later decides to gift them to another person or back to the original owner, the tax department continues to view the income as tied to the original gifting spouse. This chain of ownership does not break the clubbing rule. Investors should be aware that the tax liability follows the asset’s origin, not just its current holder.

What Investors Should Track

Taxpayers who have executed inter-spousal share transfers should maintain clear documentation of the transaction date and value. It is essential to ensure that any dividend income or capital gains earned from these assets is accurately calculated and included in the tax filing of the gifting spouse. Before filing returns, investors should verify the data in their AIS and Form 26AS to ensure that income from gifted shares is correctly attributed. If the tax filing does not reflect these clubbing rules, taxpayers may face compliance hurdles during the assessment process.