The Shift in Fiscal Strategy

The choice between the legacy tax structure and the modern framework for senior citizens has shifted from a matter of habit to a rigorous exercise in quantitative analysis. With the standard deduction now harmonized across regimes, the primary driver for selection remains the total volume of eligible outlays rather than just income bracket placement. Relying on default settings often leads to avoidable leakage, particularly for retirees whose fixed-income interest streams are supplemented by variable medical costs.

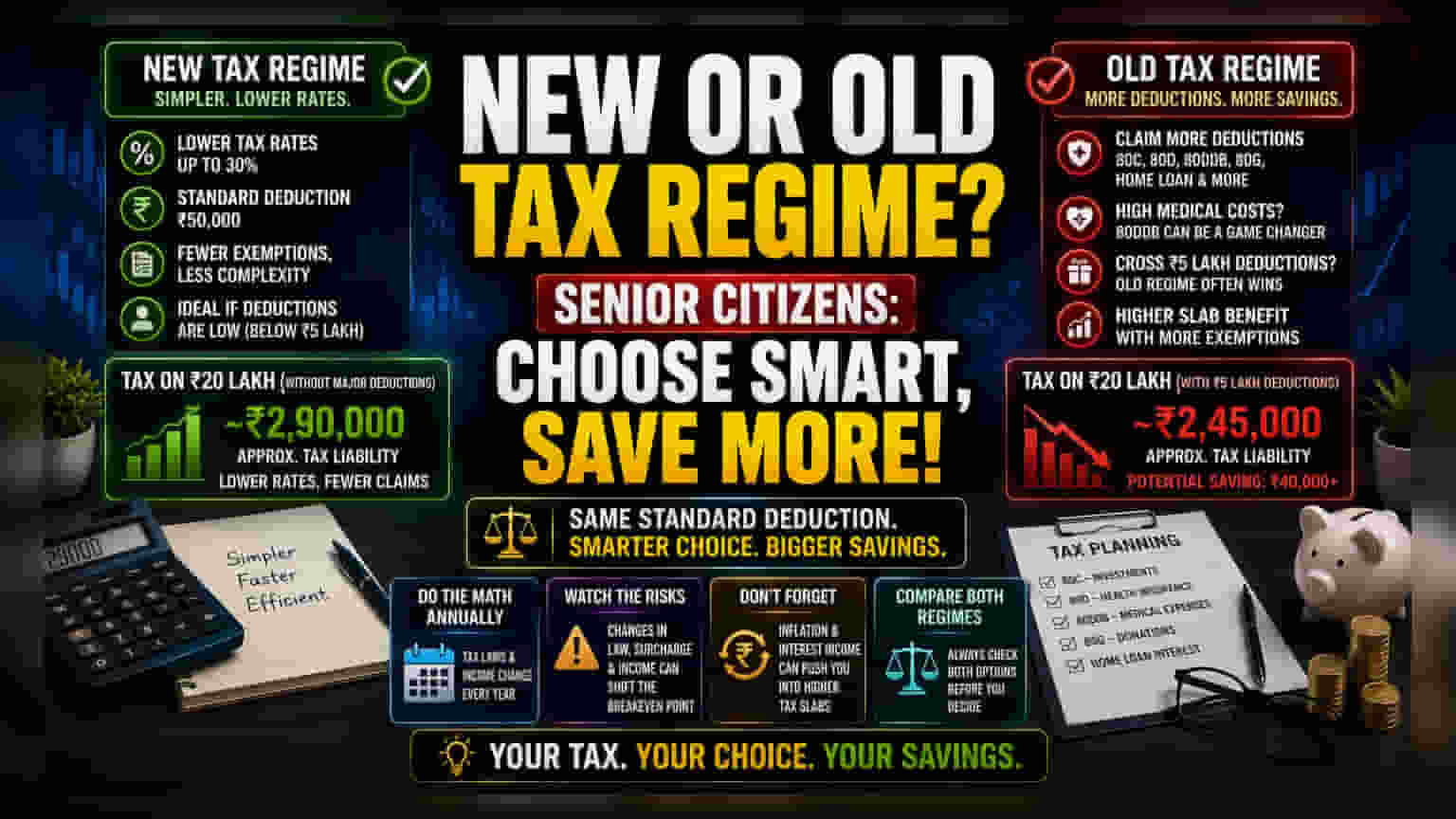

The Math Behind the Decision

For an annual income of Rs 20 lakh, the tax liability gap between the two regimes can exceed Rs 40,000 when excluding major exemptions. The new regime acts as a default efficiency engine for those with standard tax-saving habits, such as basic Section 80C and 80D utilization. However, the equilibrium shifts abruptly once total deductions cross the Rs 5 lakh mark. This is frequently achieved by taxpayers utilizing Section 80DDB for critical illness expenses or Section 80G for charitable contributions. When these specific line items are present, the benefit of the old regime’s higher bracket thresholds often offsets the lower rates offered by the simplified structure.

The Hidden Costs of Complexity

Transitioning to the new regime is often marketed as a reduction in compliance burden, but this comes with a potential opportunity cost. Taxpayers who elect the new regime effectively forfeit the ability to claim deductions for housing loans, educational expenses, and specific medical provisions. For retirees, this creates a structural disadvantage if their financial planning involves high-interest debt servicing or recurring healthcare costs. Those who opt for the simplified path must ensure that the lower tax rate provides a net benefit that exceeds the cash-flow value of those forfeited deductions.

Risk Factors and Future Proofing

Reliance on a single regime without annual reassessment is a significant fiscal hazard. Legislative adjustments to surcharge brackets or modifications to the definition of 'eligible expenses' under the old regime can alter the breakeven point overnight. Furthermore, the volatility of inflation-linked interest income for seniors can push them into higher slab rates, potentially rendering previous tax-planning decisions obsolete. Prudent management requires a side-by-side reconciliation of both potential outcomes annually, rather than assuming past years' status quo remains valid. Failing to account for changes in the composition of income—such as shifts from pension to annuity or capital gains—can result in an inefficient tax profile that neglects the interplay between the two systems.