What Happened

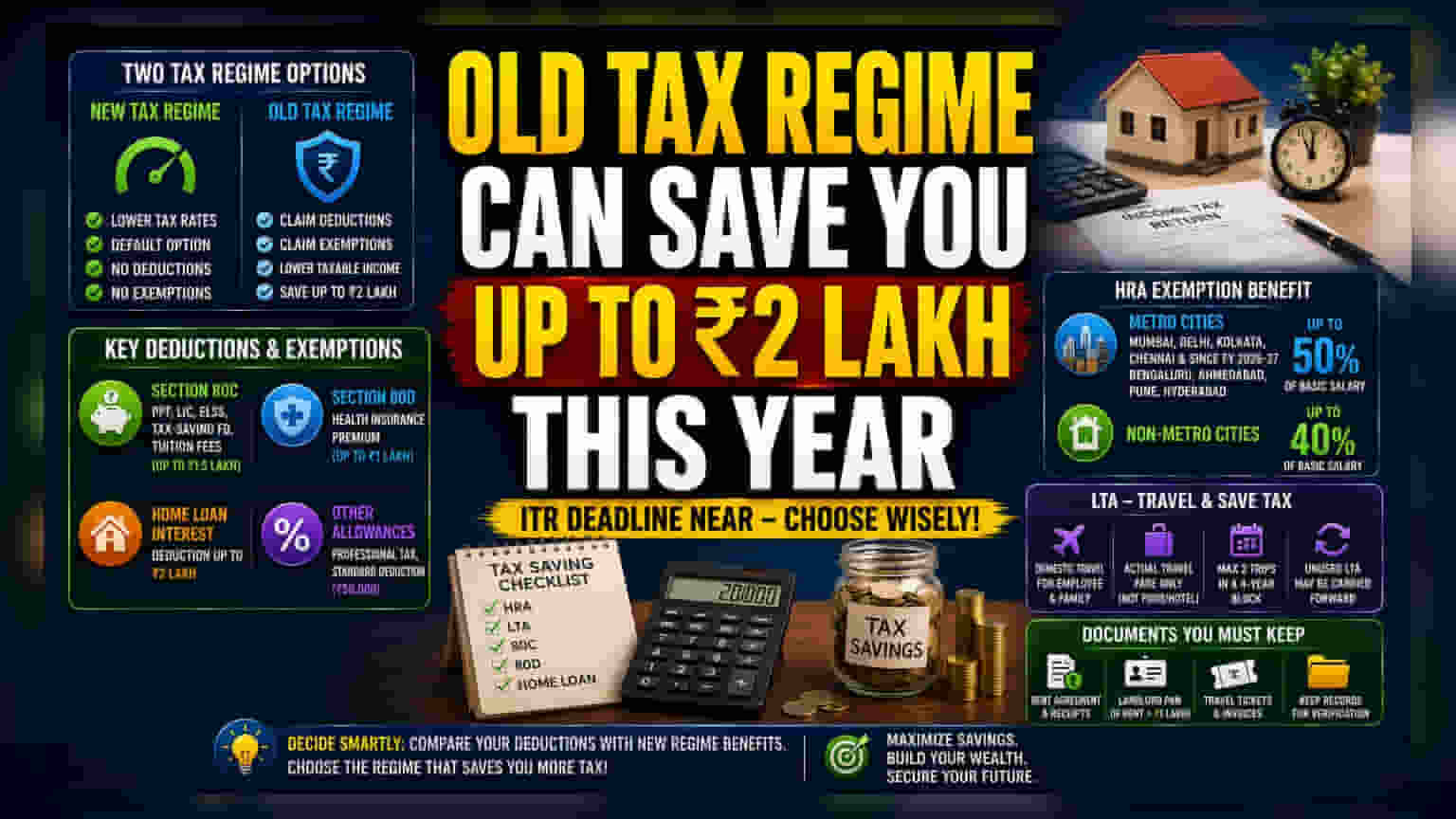

As the deadline for filing Income Tax Returns (ITR) approaches, salaried employees are evaluating their tax options for the financial year. The current tax system features two options: the new tax regime, which is the default, and the old tax regime. While the new regime offers lower tax rates, it does not allow for most deductions and exemptions. In contrast, the old tax regime permits individuals to reduce their taxable income through various investments and allowances. Employees who have significant expenses, such as rent or home loans, often find that the old regime allows them to lower their total tax liability significantly, potentially by as much as Rs 2 lakh per year, depending on their salary structure and living expenses.

The Role of Deductions and Exemptions

The ability to lower taxes under the old regime relies on specific components within a salary structure. Exemptions like House Rent Allowance (HRA) and Leave Travel Allowance (LTA) are key. Additionally, tax deductions are available under sections like 80C and 80D, and for interest paid on housing loans. Section 80C covers investments like Public Provident Fund, Life Insurance premiums, and certain mutual funds, while Section 80D focuses on health insurance premiums. These combined benefits allow taxpayers to exclude a portion of their income from taxation, which is not possible under the default new tax regime.

Understanding HRA and LTA

For those living in rented housing, HRA is a common tax-saving tool. The amount that can be exempted depends on the rent paid, the location of the residence, and the basic salary. Specifically, employees in metro cities like Mumbai, Delhi, Kolkata, and Chennai, and since fiscal year 2026-27, cities including Bengaluru, Ahmedabad, Pune, and Hyderabad, can claim a higher percentage of their salary as an HRA exemption compared to those in other locations. The exemption is calculated based on the rent paid minus ten percent of the basic salary plus dearness allowance.

LTA is another allowance that supports tax savings for domestic travel. This benefit covers the actual travel costs for the employee and eligible family members. It is not designed to cover costs like food or hotel stays. The allowance is available for a maximum of two trips within a four-year block. If these trips are not taken, the allowance can sometimes be carried forward to the next period, depending on company policy.

Importance of Documentation

Claiming these benefits requires accurate record-keeping. The Income Tax Department may ask for proof of expenses. For HRA, this includes the rent agreement and receipts. If the annual rent paid exceeds Rs 1 lakh, it is necessary to provide the landlord's Permanent Account Number (PAN). Similarly, LTA claims require submission of travel documents like tickets and invoices. Maintaining these documents ensures that the claims are verifiable if the tax department requests documentation during the verification process.

What Investors and Employees May Monitor

When deciding between the two regimes, employees often look at their total deductible expenses against the potential tax savings from the lower rates of the new regime. The decision depends on how much an individual spends on rent, loan interest, and specific insurance or investment products. For those with a salary structure that lacks these specific components, the default new regime might remain the simpler choice. The key factor for employees is calculating which regime results in a lower total tax payment based on their personal financial situation, income level, and ability to document their expenses.