As Senior Citizens' Savings Scheme (SCSS) deposits reach maturity in 2026, retirees face a key decision on whether to renew or diversify. While the scheme offers a stable 8.2% return, investors should compare it against bank FDs and Post Office schemes, focusing on liquidity, tax implications, and the impact of inflation on long-term capital.

What Happened

Many retirees who invested in the Senior Citizens' Savings Scheme (SCSS) a few years ago are approaching the maturity date of their deposits in 2026. This period is a critical time for financial planning, as it requires retirees to decide whether to reinvest in the same scheme or shift their capital to other financial instruments. The SCSS has long been a preferred choice for Indian retirees due to its government backing, fixed return, and safety features.

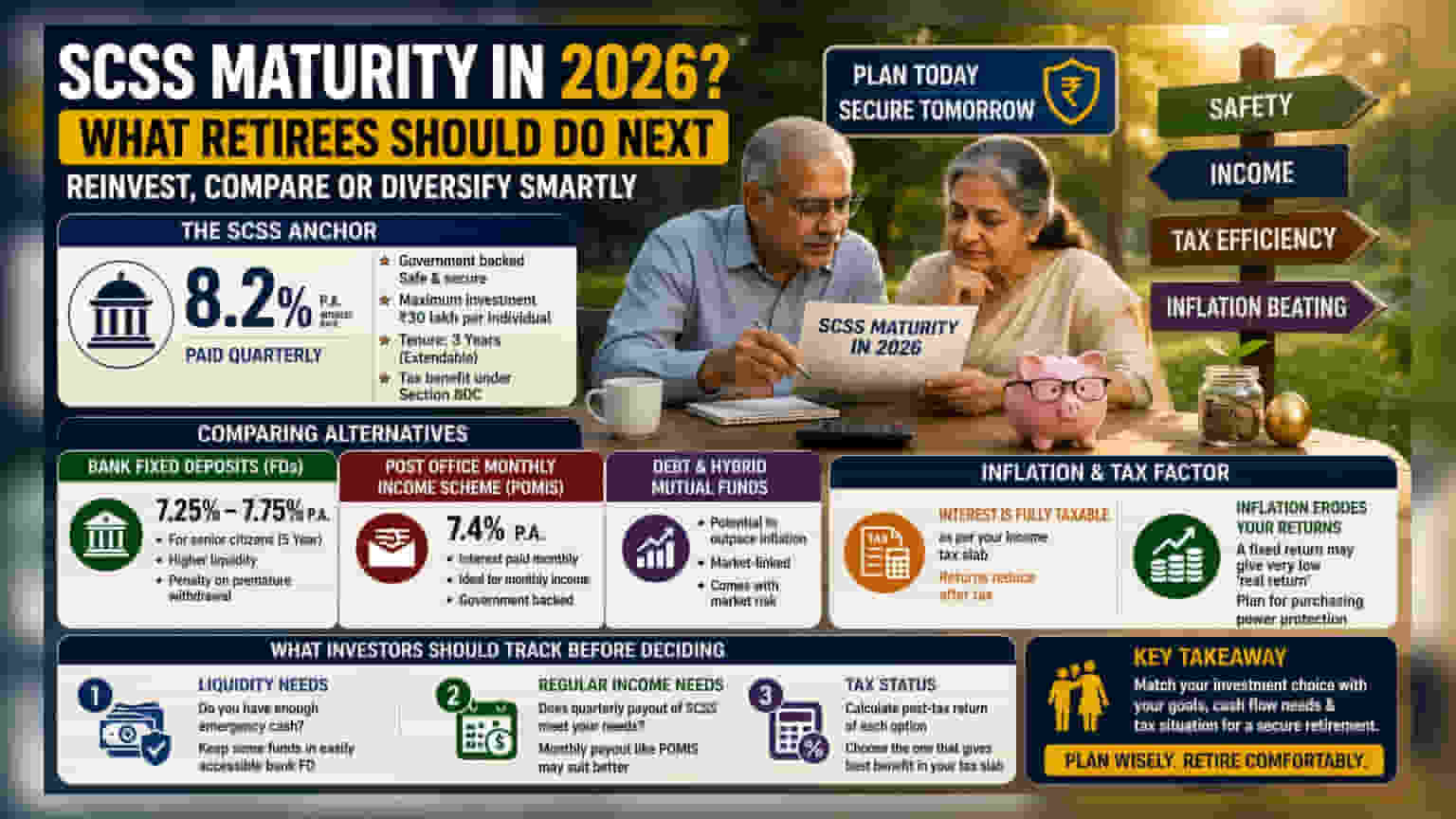

The SCSS Anchor

The current interest rate for SCSS is 8.2% per annum, paid quarterly. This rate is fixed for the duration of the deposit, providing predictable income, which is a primary requirement for most retirees. The scheme allows a maximum investment of Rs 30 lakh per individual and offers tax benefits under Section 80C of the Income Tax Act. For investors who prioritize safety above all else, the government-backed status of the SCSS remains a strong reason to consider a renewal for another three-year cycle.

Comparing Alternatives

While the SCSS is a strong income generator, it may not be the only tool needed for a retirement portfolio. Investors often look at other options to balance different financial needs.

Bank Fixed Deposits (FDs) are a common alternative. While current yields for seniors generally range between 7.25% and 7.75% for five-year terms, they offer higher liquidity compared to the SCSS. If a retiree anticipates the need for sudden cash, such as for medical expenses, the penalty-based withdrawal options in FDs can be more practical than locking funds in the SCSS.

Another option is the Post Office Monthly Income Scheme (POMIS), which currently offers a 7.4% annual return. The key difference here is the payment frequency—interest is credited monthly rather than quarterly. This can be more useful for retirees who manage their monthly household budget based on a fixed inflow.

The Inflation and Tax Factor

Retirees must look beyond the headline interest rate. First, interest earned from SCSS, bank FDs, and POMIS is fully taxable according to the individual's income tax slab. This means the actual return in the investor's hand could be significantly lower than the quoted rate, depending on their total taxable income.

Second, inflation acts as a hidden risk to retirement funds. If inflation stays at a certain level, a fixed return of 7.5% or 8% might only provide a very small 'real return'—the actual increase in purchasing power. To combat this, some financial planners suggest that retirees might consider allocating a portion of their corpus to debt mutual funds or conservative hybrid funds. These investments are market-linked and may offer the potential to outpace inflation better than traditional fixed-income schemes, though they come with market risk.

What Investors Should Track

When deciding where to move funds upon maturity, investors may focus on three main factors:

- Liquidity needs: Do you have enough emergency cash, or should you keep some funds in an easily accessible bank FD?

- Regular income needs: Does the quarterly payout of SCSS meet your needs, or would a monthly payout like POMIS be better?

- Tax status: Calculate the post-tax return of each option to see which one provides the best benefit based on your current tax bracket.