With education costs for tuition and foreign studies surging, families are increasingly prioritizing long-term investments. Effective financial planning now requires balancing these costs against retirement and healthcare goals to avoid compromising long-term stability.

Why Education Costs Are Rising

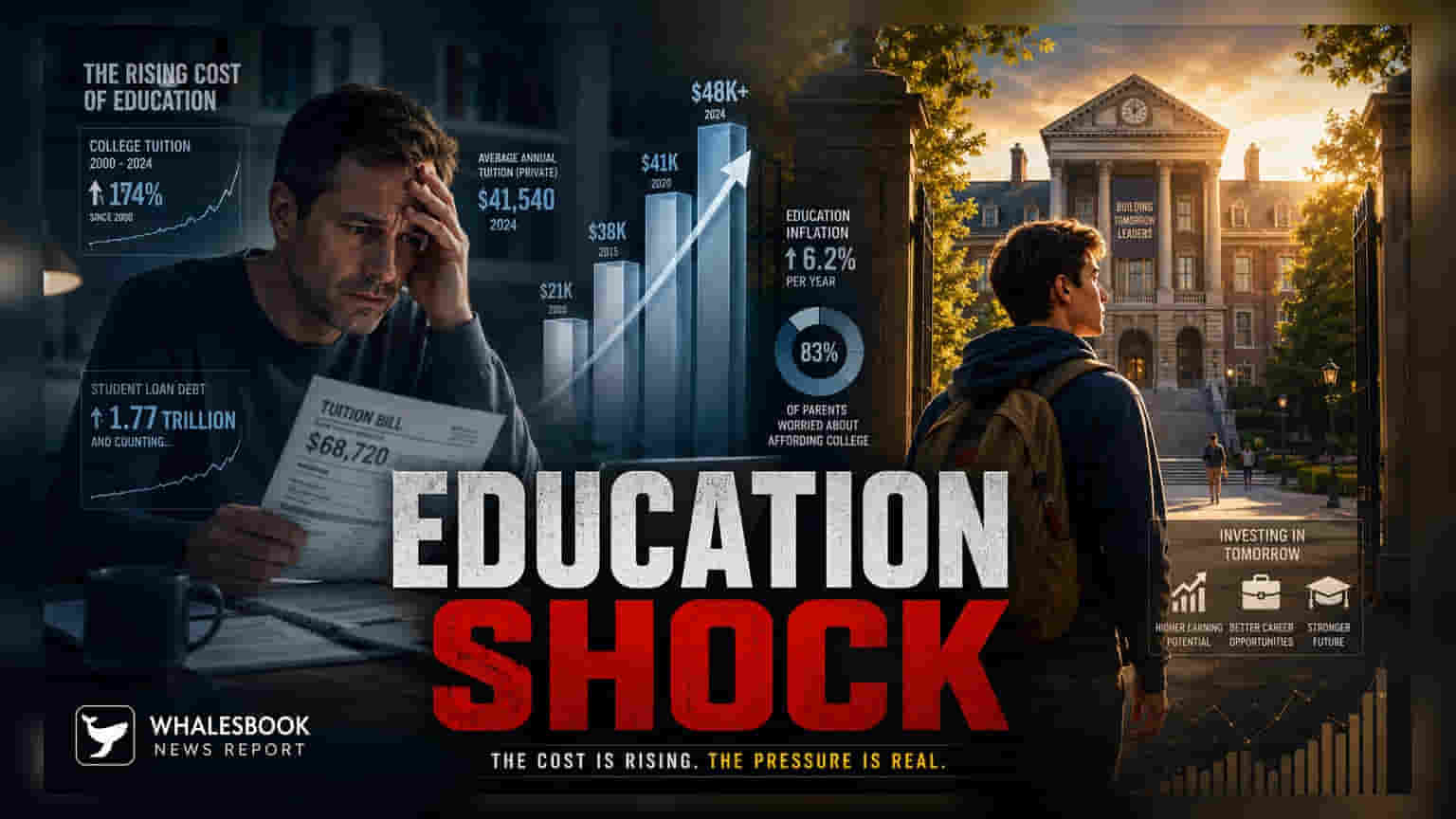

Families are experiencing significant increases in the cost of higher education, driven by rising tuition fees, living expenses, and the growing costs associated with pursuing studies abroad. Inflation in the education sector often outpaces general consumer price inflation, meaning that income growth alone may not be enough to cover future requirements. Because these costs are predictable in timing but volatile in price, they have become a major driver of household financial stress.

The Importance of Starting Early

Financial planning for education now requires a much longer time horizon than in the past. By starting investments years before a child reaches college age, families can utilize the power of compounding to build necessary funds. This approach shifts the reliance away from taking on large amounts of debt near the time of admission. Investors often look at systematic investment plans or long-term debt-equity balanced portfolios to align with these specific target dates.

Managing Investment Shifts

As the target year for education expenses approaches, many financial strategies shift their focus. The objective often moves from aggressive capital appreciation to capital preservation. This is a critical step because market volatility in the final years before the expense can significantly reduce the available corpus. Protecting the accumulated amount from sharp market corrections is essential to ensure that funds are available when needed.

The Debt Consideration

While education loans provide an immediate solution, they represent a long-term financial commitment. For families, these loans carry repayment obligations that can extend well into the parent's later working years or the child's early career. Understanding the interest rates, repayment periods, and potential impact on a family’s debt-to-income ratio is a crucial part of the planning process.

Balancing Multiple Financial Goals

Education funding rarely happens in isolation. Families must weigh this goal against other important objectives such as retirement savings, health insurance coverage, and emergency funds. The risk of over-allocating to one goal is that it may leave other areas, such as retirement security, underfunded. A balanced strategy requires prioritizing these goals simultaneously to maintain overall financial health.

What To Track Next

For families, the primary monitorables include the annual increase in education costs, changes in interest rates for education loans, and the performance of long-term investment vehicles. Reviewing financial plans every year allows for adjustments based on inflation or changes in career goals, ensuring the overall strategy remains sustainable.