Retirees often prioritize dividend stocks for regular income, but tax efficiency is a critical factor often overlooked. While dividends are fully taxable at the investor's slab rate, Systematic Withdrawal Plans (SWPs) may offer better post-tax outcomes by separating capital from gains. Understanding these differences, alongside alternatives like REITs and InvITs, helps in building a more reliable retirement corpus.

What Happened

For many Indian retirees, generating a steady stream of income is the primary goal of their investment portfolio. Traditionally, investors have gravitated toward dividend-paying stocks and Income Distribution cum Capital Withdrawal (IDCW) options in mutual funds. However, recent financial analysis suggests that focusing solely on headline yields can be misleading due to tax implications. Financial experts are now highlighting the need to look at post-tax returns, payout consistency, and tax efficiency to ensure long-term sustainability for a retirement income strategy.

The Tax Reality Of Dividends

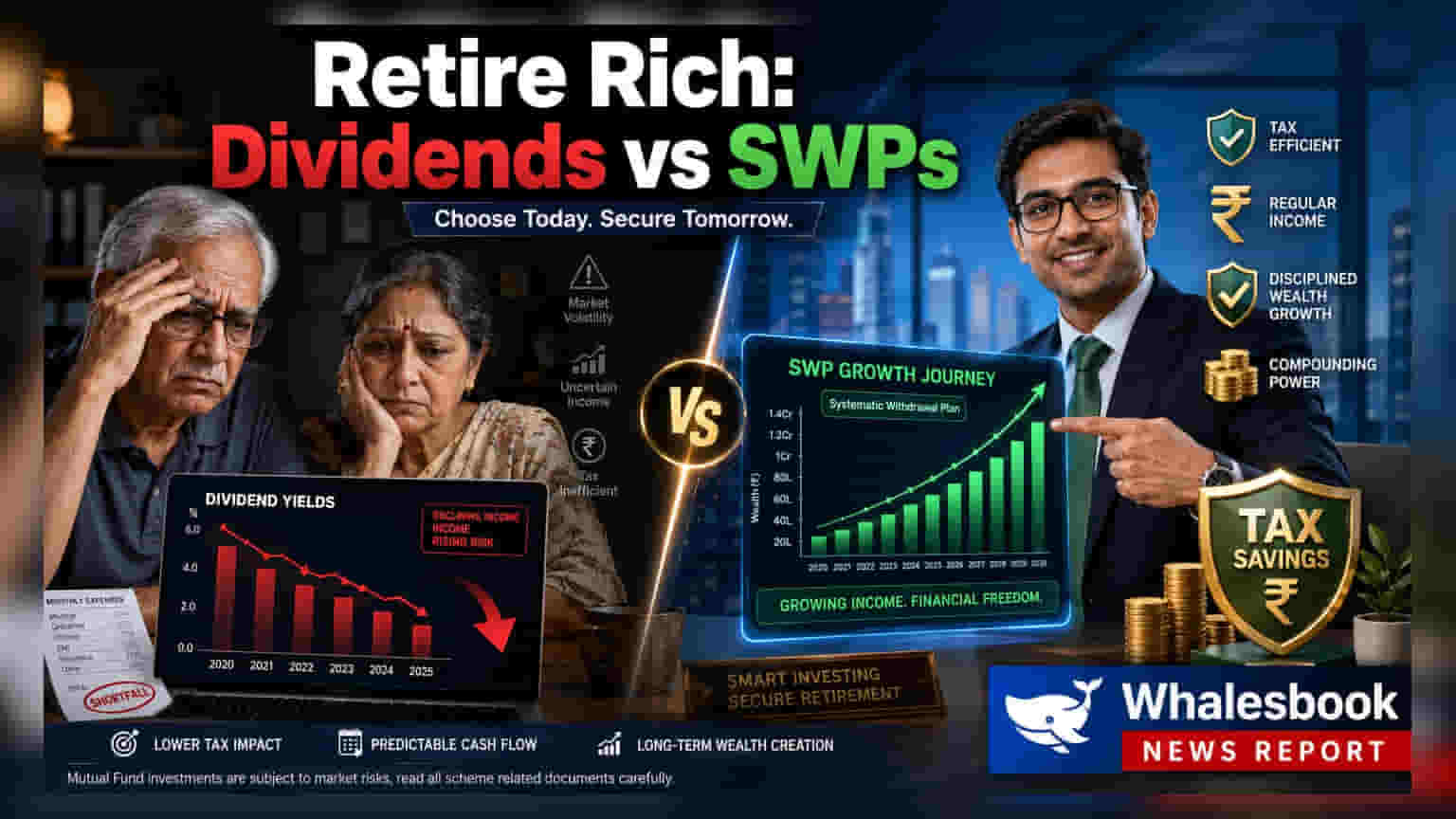

Dividend-paying stocks, particularly in sectors like IT, FMCG, and public sector undertakings, are often chosen for their history of regular payouts. While these companies may have strong cash flows, the income received by the investor is treated as 'income from other sources.' This means dividends are taxed entirely at the investor's applicable income tax slab rate. For retirees in higher tax brackets, this significantly reduces the actual money in hand. For instance, a headline yield of 6% could effectively drop to 4% after accounting for taxes, making it a less efficient source of retirement cash flow than it appears at first glance.

How SWPs Work For Income

Systematic Withdrawal Plans (SWPs) are gaining attention as a more tax-efficient alternative to traditional dividends. In an SWP, an investor chooses a set amount to withdraw from their mutual fund investment at regular intervals. The primary advantage lies in the tax treatment. When a withdrawal is made, only the capital gains portion—the profit component—is subject to tax, while the portion representing the original invested capital is returned tax-free. This mechanism can result in a lower overall tax liability compared to receiving direct dividend payouts, which are fully taxable. However, the taxation of capital gains can vary based on whether the mutual fund is equity-oriented or debt-oriented.

The Role Of REITs And InvITs

Real Estate Investment Trusts (REITs) and Infrastructure Investment Trusts (InvITs) have emerged as another avenue for income-seeking investors. These investment vehicles are regulated to distribute a significant portion of their cash flows—mandated at 90%—back to the unitholders. This structure is designed to provide relatively predictable and consistent income. Beyond the payout, these trusts also offer the potential for capital appreciation over time. They serve as an additional layer for those looking to diversify beyond traditional equity or debt instruments.

Building A Balanced Portfolio

No single investment product is universally suitable for every retiree. Relying heavily on any one asset class can expose the portfolio to market volatility or irregular payout schedules. Financial planners often emphasize that the ultimate strategy should balance income consistency with capital preservation. A well-diversified portfolio might combine different instruments, including traditional fixed deposits, government savings schemes, and quality bonds, to ensure that the total post-tax income meets personal requirements without jeopardizing the principal amount. Investors may focus on their specific tax slab and overall financial goals when choosing between these different income-generating mechanisms.