Regulations strictly allow only one Public Provident Fund (PPF) account per person. Holding multiple accounts can trigger complications with tax-free interest and maturity claims. Investors must understand that the annual investment cap of ₹1.5 lakh is a collective limit. This article explains how to stay compliant, handle minor accounts, and why transferring is a better solution than opening new accounts.

What Happened

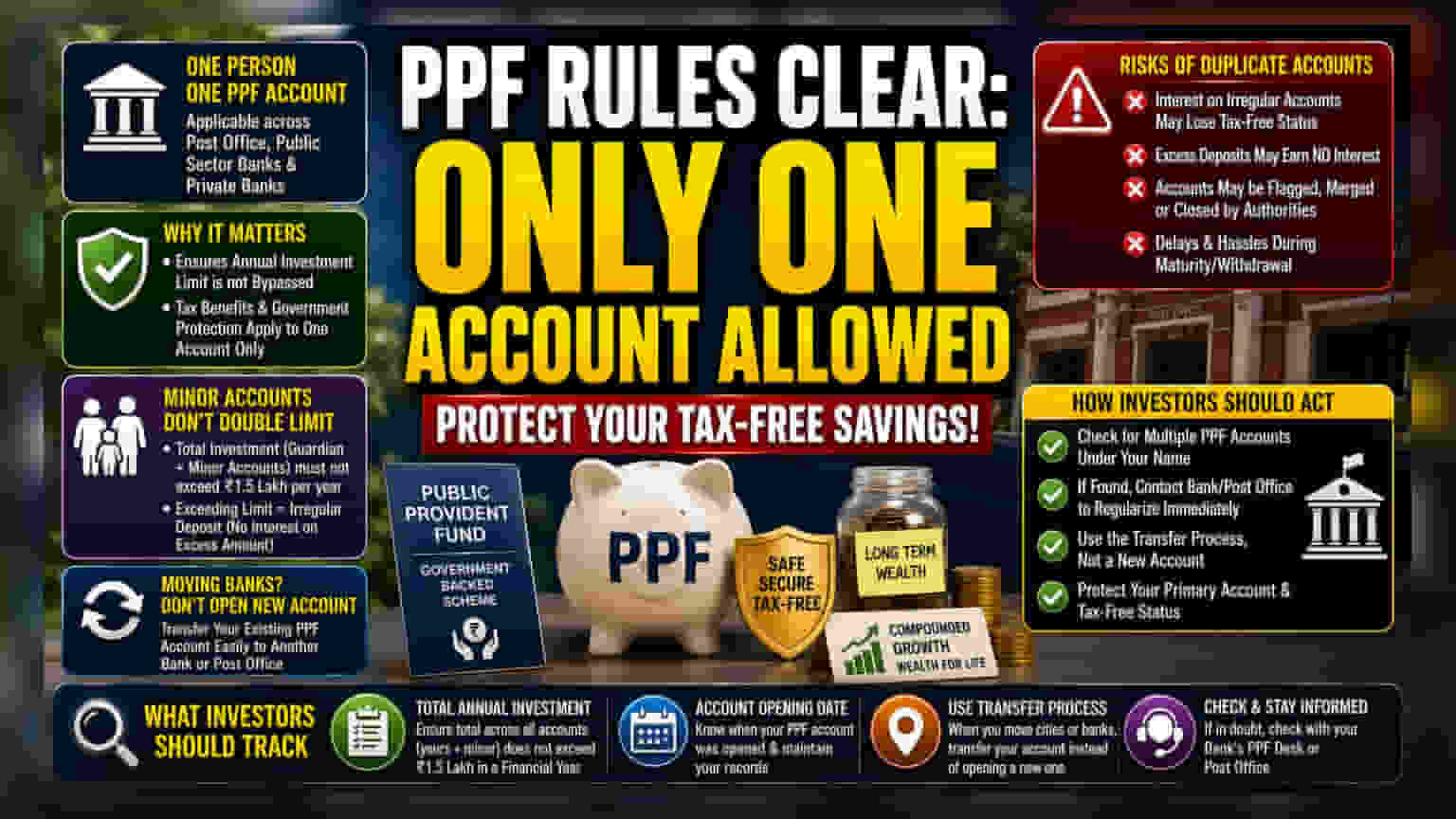

The government rules for the Public Provident Fund (PPF) are clear and strict: every individual is allowed to maintain only one account. This regulation applies regardless of whether the account is held in a post office, a public sector bank, or a private bank. The intent behind this rule is to ensure that the annual investment cap is not bypassed and to streamline the administration of the government-backed scheme.

Why The One-Account Rule Matters

For many Indian investors, the PPF is a core part of long-term savings because of its tax-free interest and government backing. However, this tax advantage comes with strict compliance requirements. If an investor holds more than one PPF account, it complicates the financial picture. Because the PPF is designed as a single-account product, the interest earned on any "irregular" or duplicate account may not enjoy the same tax-free status or regulatory protection as the primary account. Investors often fail to realize that their pan-India investment limit is linked to their identity, not their bank accounts.

The Minor Account Confusion

A frequent area of confusion involves accounts opened for minor children. While parents or legal guardians are permitted to open a PPF account for a minor, this does not double the investment limit. The total annual contribution across the guardian's own account and all minor accounts under their guardianship must not exceed the statutory limit of ₹1.5 lakh. Exceeding this limit leads to irregular deposits, which can result in the loss of interest on the excess amount and potential issues during the maturity phase.

Risks Of Duplicate Accounts

Maintaining multiple accounts can lead to several complications. The most significant risk is administrative: when it comes time to claim maturity proceeds or make withdrawals, the government or the bank may flag the accounts as irregular. This can trigger a process of account closure or mandatory merging, which can be time-consuming and frustrating. Furthermore, if an investor inadvertently deposits money into a second account, that excess amount may not earn interest, effectively wasting the investor's capital. In some cases, authorities may force the closure of the secondary account, which could impact the investor's long-term financial planning.

How Investors May Read This

If an investor finds they have multiple accounts, the goal should be to resolve the situation promptly rather than ignoring it. Often, this happens due to migration between cities or changing banks for better digital access. Instead of opening a new account, the recommended approach is to transfer an existing PPF account from one bank or post office to another. Most banks now provide online tools to manage PPF, which makes transferring a straightforward process. If multiple accounts already exist, investors should consult their bank or post office immediately to understand the regularization process, which typically involves merging or closing the secondary account to protect the status of the primary one.

What Investors Should Track

The most important monitorable for any PPF investor is the total annual investment across all held accounts. Investors should keep a record of when their PPF account was opened and ensure that they are not using multiple accounts simultaneously. If they are moving between cities, they should use the formal transfer process instead of initiating a new account. Finally, if there is any doubt about the status of an existing account, checking with the respective bank's PPF desk or the post office is essential to avoid surprises at the time of maturity.