Many investors overlook the loan facility against their Public Provident Fund (PPF) account, which offers significantly lower interest rates than personal loans. However, strict rules regarding eligibility, the loan amount, and repayment penalties apply. Understanding these constraints is essential before choosing this route for emergency funding.

What Happened

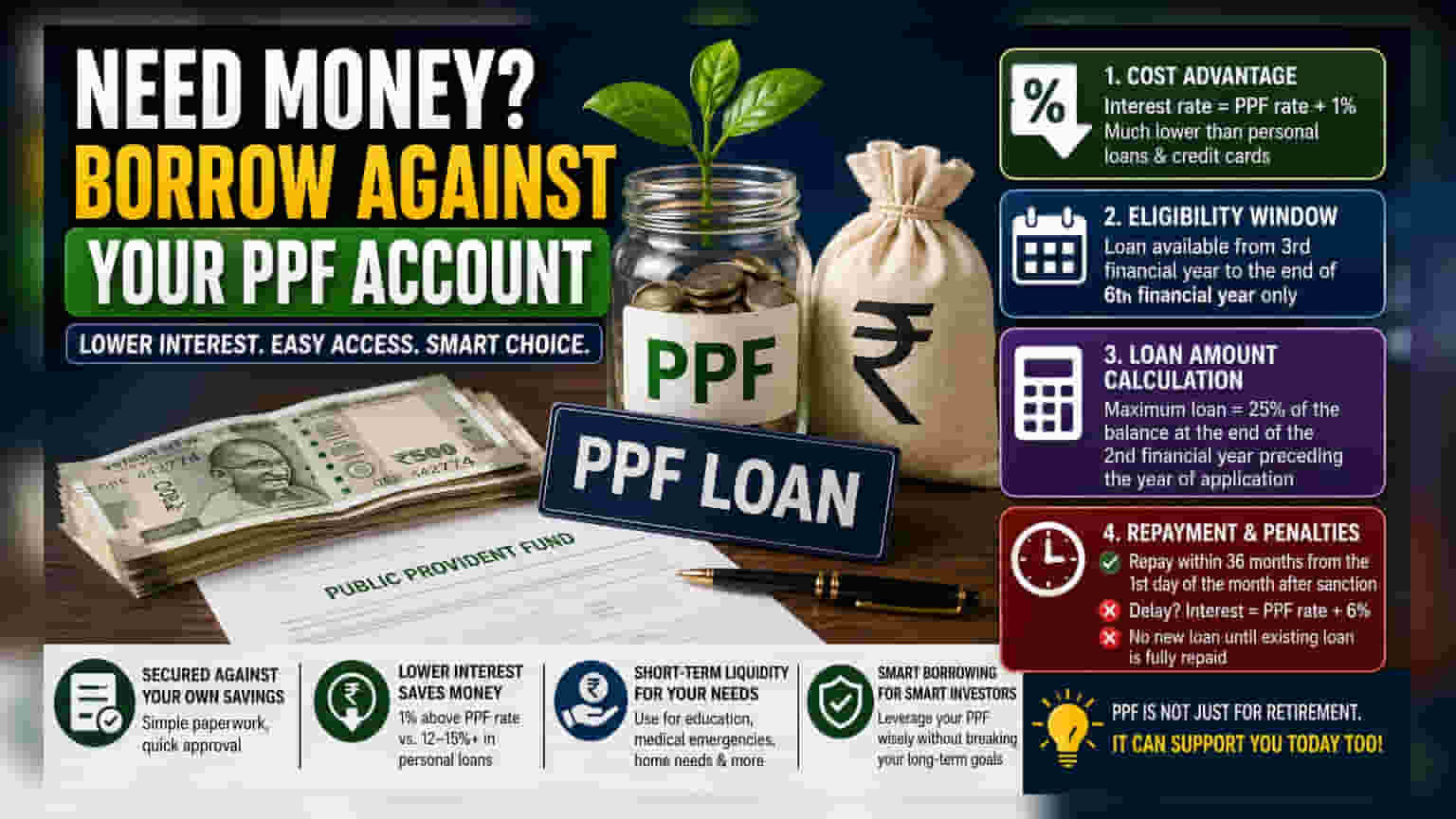

For many Indian investors, the Public Provident Fund (PPF) is primarily seen as a long-term retirement tool. However, the scheme also includes a facility that allows account holders to borrow money against their savings. This option is often more economical than taking a personal loan or using a credit card, especially for those who need temporary liquidity and have an active PPF account.

The Cost Advantage

The primary benefit of borrowing against a PPF account is the interest rate. While personal loans and credit cards can carry high annual interest rates often exceeding 12% to 15%, a PPF loan is priced much lower. The interest charged is typically just 1% above the prevailing PPF interest rate. Because it is a secured loan—backed by the investor's own savings—the paperwork is generally simpler and faster than seeking an unsecured loan from a bank.

The Eligibility Window

Investors often make the mistake of assuming this loan facility is available throughout the entire 15-year tenure of the PPF account. In reality, the access is time-bound. A loan can only be taken starting from the third financial year after the account was opened, and it must be applied for before the end of the sixth financial year. Once this specific period passes, the loan facility is no longer available, and account holders may only rely on partial withdrawal options as per the scheme rules.

How The Loan Amount Is Calculated

It is important to note that the loan amount is not based on the balance currently sitting in the account. Instead, the maximum loan limit is capped at 25% of the balance that existed at the end of the second financial year preceding the year of application. For instance, if an investor applies for a loan in the current financial year, the limit is based on the balance from two years prior. This means the actual cash available through this route might be lower than what an investor expects based on their current statement.

Repayment And Penalties

These loans are intended for short-term needs and must be repaid within 36 months from the first day of the month following the loan sanction. If an investor fails to repay the principal amount within this 36-month window, the interest rate significantly increases. The penalty rate climbs to 6% above the prevailing PPF interest rate, making it a much more expensive form of borrowing than the original loan. Investors must also settle any accrued interest after the principal is cleared. Furthermore, a new loan cannot be sanctioned until the existing one is fully repaid.