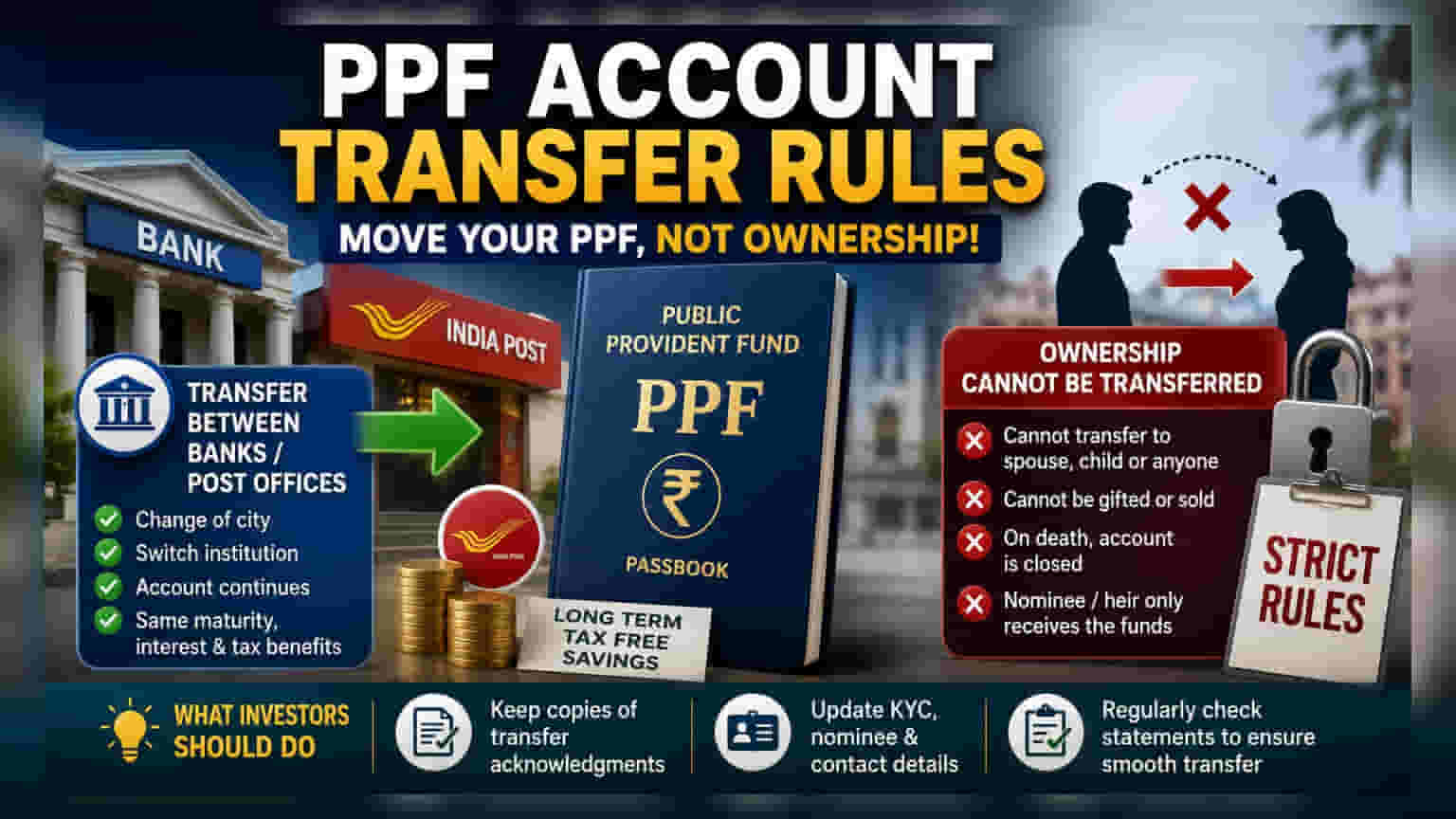

Investors can transfer their Public Provident Fund (PPF) accounts between authorized banks and post offices without losing maturity or tax benefits. However, ownership cannot be transferred to another individual, including family members. Maintaining updated KYC and nominee details is essential to ensure a smooth transition and future claims.

What Happened

Public Provident Fund (PPF) accounts are a staple for long-term, tax-efficient savings in India. For investors who relocate or wish to consolidate their finances under one banking service provider, the government allows the transfer of these accounts between authorized banks and post offices. While this administrative flexibility exists, the rules regarding account ownership remain strict, and understanding these distinctions is important for effective long-term financial planning.

Moving Your Account Between Institutions

Investors who change their city of residence or switch their preferred financial institution can move their PPF account. This process is treated as a continuation, meaning the account’s original maturity date, accumulated interest, and tax benefits remain fully protected. The transfer does not result in the account being closed and reopened; it simply shifts the administration from one branch or institution to another, preserving the account's history.

The process typically requires submitting a transfer request at the current bank or post office. The institution then forwards the necessary account documents to the new branch or bank chosen by the investor. It is often necessary to complete a fresh Know Your Customer (KYC) update at the new institution to finalize the transfer process.

The Restriction on Account Ownership

A common question is whether a PPF account can be transferred to another person, such as a spouse or child, to continue the investment. This is not permitted. PPF accounts are strictly linked to the original account holder’s identity. The ownership cannot be gifted, sold, or transferred to any other individual, regardless of their family relationship.

In the unfortunate event of the account holder's death, the account cannot continue to be operated by a nominee or legal heir. Instead, the account must be closed, and the remaining funds are disbursed to the designated nominee or legal successor according to official procedures. Nominees are only entitled to claim the funds after the death of the account holder and do not gain control of the account while the holder is alive.

What Investors Should Monitor

To ensure the smooth transfer of an account, investors should keep copies of all transfer acknowledgments provided by the bank or post office. Always verify that nominee details, address, and contact information are updated in the records of the new institution immediately after the transfer. Regularly checking account statements is a good practice, as it helps confirm that the transfer has been processed correctly and that all historical data is reflected accurately at the new location.