Retirees in India often compare the Post Office Monthly Income Scheme (POMIS) and the Senior Citizens Savings Scheme (SCSS) for reliable, fixed income. While SCSS generally provides higher interest rates and tax benefits, POMIS offers broader eligibility. This overview breaks down the deposit limits, tax rules, and withdrawal penalties to help retirees understand how these government-backed options function.

What Happened

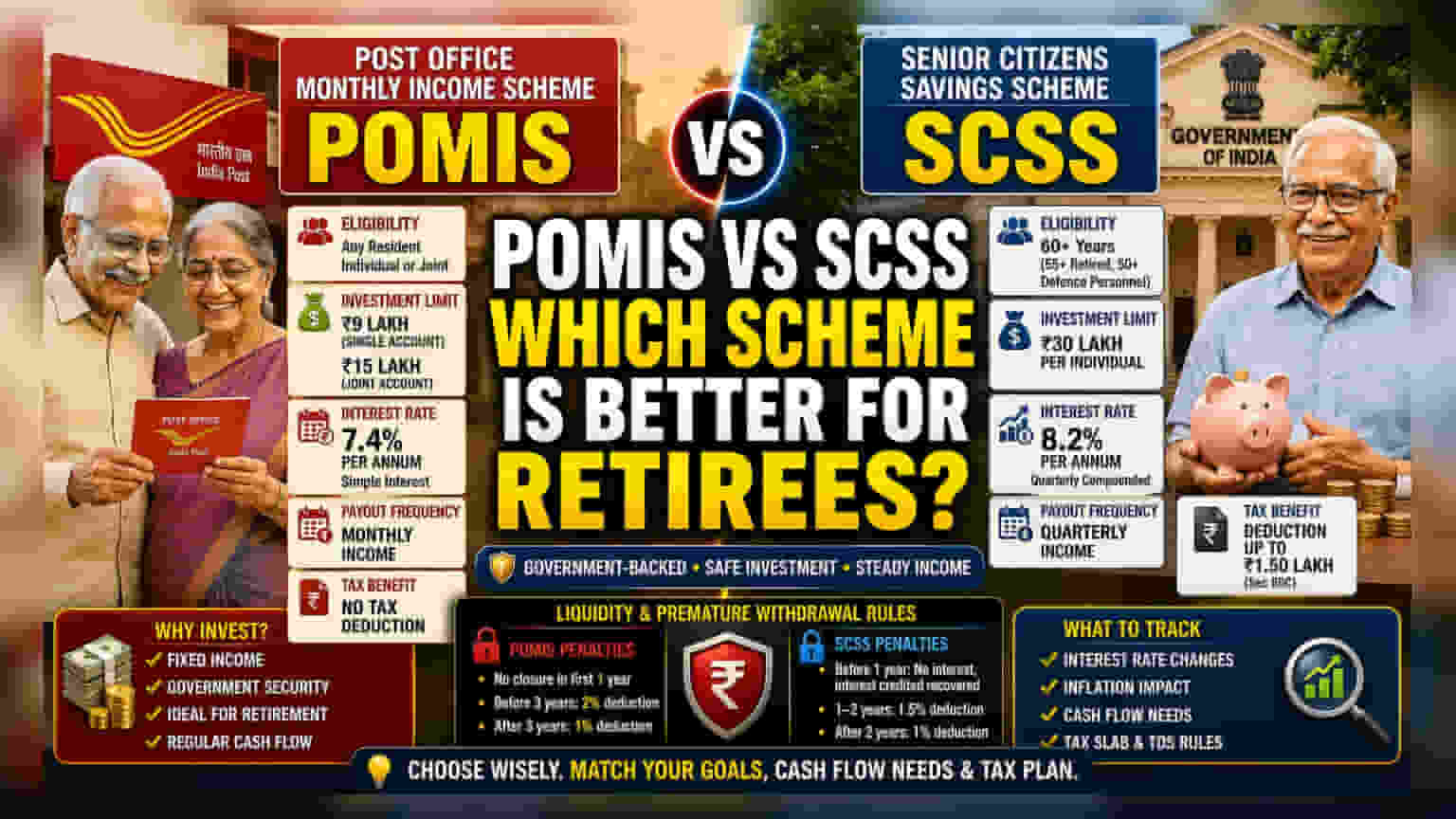

Retirees looking for government-backed, fixed-income investments often evaluate the Post Office Monthly Income Scheme (POMIS) and the Senior Citizens Savings Scheme (SCSS). Both options are popular for their safety, as they are backed by the Indian government. However, they serve different purposes based on eligibility, income requirements, and tax status. Understanding the specific differences between these schemes is important for those managing their retirement corpus.

Eligibility and Investment Limits

The two schemes differ primarily in who can open them and how much capital can be invested. The Senior Citizens Savings Scheme (SCSS) is strictly for individuals aged 60 and above. There is a relaxation for those between 55 and 60 years old who have retired, and special provisions exist for retired defence personnel aged 50 and above. The maximum investment allowed per individual in SCSS is ₹30 lakh.

In contrast, the Post Office Monthly Income Scheme (POMIS) is open to any resident of India. The maximum deposit limit is ₹9 lakh for a single account and ₹15 lakh for a joint account. Investors can hold multiple accounts, provided their total share in all accounts does not exceed these specific thresholds.

Income Generation and Interest Rates

The primary driver for many investors is the interest rate. SCSS currently offers an interest rate of 8.2% per annum, which is compounded quarterly. This helps in generating a higher effective yield compared to POMIS, which offers a 7.4% annual interest rate paid out on a simple interest basis.

Because SCSS interest is paid quarterly and POMIS interest is paid monthly, the cash flow patterns differ. Investors needing regular monthly income to cover specific expenses might prefer the structure of POMIS, while those focused on maximizing the absolute interest earned often look toward the higher rate offered by SCSS.

Tax Implications and Benefits

Tax planning is a critical part of retirement strategy. Investments in SCSS qualify for a tax deduction of up to ₹1.50 lakh under the Income Tax Act. This can lower the overall tax burden for the year in which the investment is made. POMIS, however, does not provide this specific tax deduction benefit.

It is important to note that interest earned from both schemes is fully taxable. While the interest from POMIS does not attract Tax Deducted at Source (TDS), SCSS interest is subject to TDS if the annual interest income exceeds ₹1 lakh. Investors may need to submit Form 15G or 15H to manage TDS if their total income is below the taxable threshold.

Liquidity and Premature Withdrawal

Accessing money in an emergency is a key consideration for retirees. Both schemes have penalties for closing the account before the 5-year maturity period. For POMIS, there is no option to close the account within the first year. Exiting before three years leads to a 2% deduction on the deposit, while exiting after three years results in a 1% penalty.

SCSS has stricter liquidity rules. If an account is closed before one year, no interest is paid, and any interest already credited is recovered. Closures between one and two years attract a 1.5% deduction, and closures after two years incur a 1% deduction. Investors should ensure they do not require these funds in the short term to avoid these penalties.

What Investors Should Track

Investors should monitor the quarterly announcements of interest rates by the government, as these rates are reviewed periodically and can change. Additionally, those planning their finances should consider the impact of inflation on fixed-income returns over the 5-year tenure. Comparing the payout frequency—monthly for POMIS versus quarterly for SCSS—against specific cash flow requirements remains a standard practice for retirement planning.