Indian taxpayers are currently evaluating the choice between the old and new tax regimes. While the new regime offers lower tax rates with fewer deductions, the old regime retains benefits like HRA and insurance claims. With the new system acting as the default, understanding whether to switch depends on your specific income level and total available deductions. The new regime is often simpler for those earning up to Rs 12 lakh, but higher earners must calculate their potential savings carefully.

What Happened

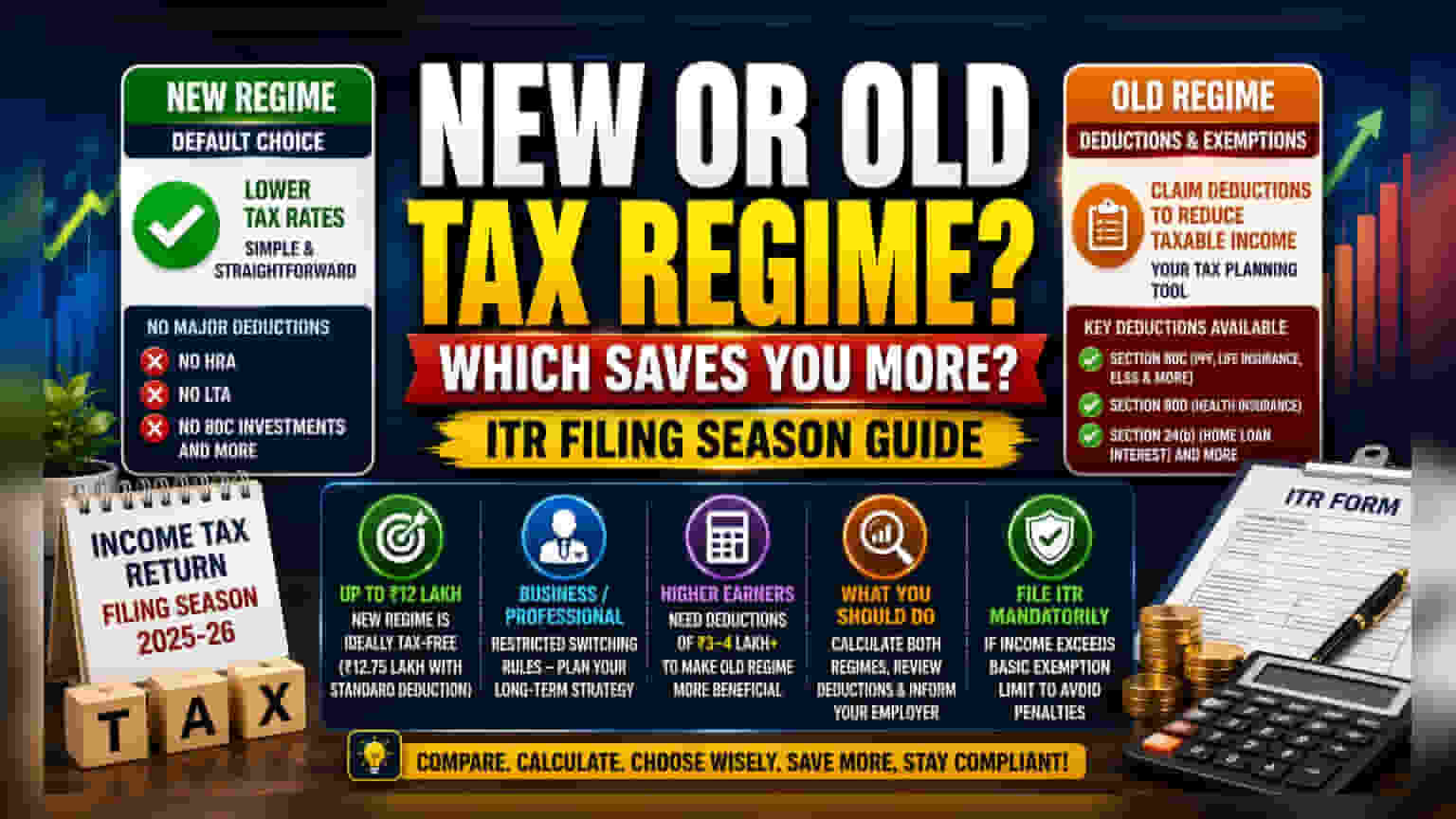

As the income tax return (ITR) filing season approaches, many taxpayers are assessing whether to stick with the new income tax regime or opt for the old one. The new tax regime is now the default system for taxpayers. This means that if you do not explicitly choose the old regime, your tax liability will be calculated based on the new, simplified structure. The key difference lies in the trade-off between lower tax rates and the ability to claim various exemptions and deductions.

The Core Difference: Rates vs. Deductions

The fundamental choice for a taxpayer is between simplicity and potential savings through deductions. The new regime simplifies the process by offering lower tax rates for most income brackets. However, to keep this structure simple, the government has removed most tax exemptions that were popular under the old regime. These removed benefits include House Rent Allowance (HRA), Leave Travel Allowance (LTA), and various investments under Section 80C, such as PPF, life insurance premiums, and ELSS.

In contrast, the old regime acts as a tool for tax planning. It allows taxpayers to reduce their taxable income by claiming deductions under sections like 80C, 80D (for health insurance), and 24(b) (for home loan interest). The challenge is that the old regime comes with higher tax rates. Consequently, for many, the lower rates of the new regime often offset the loss of these deductions, especially at lower-to-mid income levels.

The Income Threshold Explained

The government has made the new regime quite attractive for individuals with annual incomes up to Rs 12 lakh. Under this system, income up to this level is effectively tax-free. For salaried individuals, this limit reaches Rs 12.75 lakh when including the standard deduction. If your income falls within this bracket, the math is straightforward, and the new regime often results in a lower tax outgo without the need to track investments or receipts for deductions.

Business Income and Switching Restrictions

There is a crucial distinction between salaried individuals and those with business or professional income. While salaried taxpayers can usually choose their regime every year, those with business or professional income face stricter rules. If a business owner or professional opts out of the new regime, they may face limitations on how often they can switch back. This makes it essential for business owners to evaluate their long-term tax strategy rather than viewing the choice as a year-to-year adjustment.

Considerations for Higher Earners

For those earning above the Rs 12 lakh threshold, the decision requires more effort. The viability of the old regime depends on the total value of your eligible deductions. Financial experts often suggest that unless your total deductions amount to at least Rs 3 to 4 lakh, the tax liability under the old regime may remain higher than under the new one. Taxpayers should calculate their total deductions—including home loan interest, HRA, and section 80C investments—and compare the final tax payable under both regimes before making a final call.

What Taxpayers Should Monitor

To make an informed decision, taxpayers should first calculate their total tax liability under both systems. Review your salary structure or business income records to identify every available deduction. Remember that the new regime still allows for the standard deduction and certain NPS benefits if provided by an employer. Finally, ensure your tax choice is communicated to your employer during the financial year to avoid automatic enrollment in the default regime. Regardless of which system is chosen, filing an ITR remains mandatory for anyone with income exceeding the basic exemption limit to avoid potential penalties.