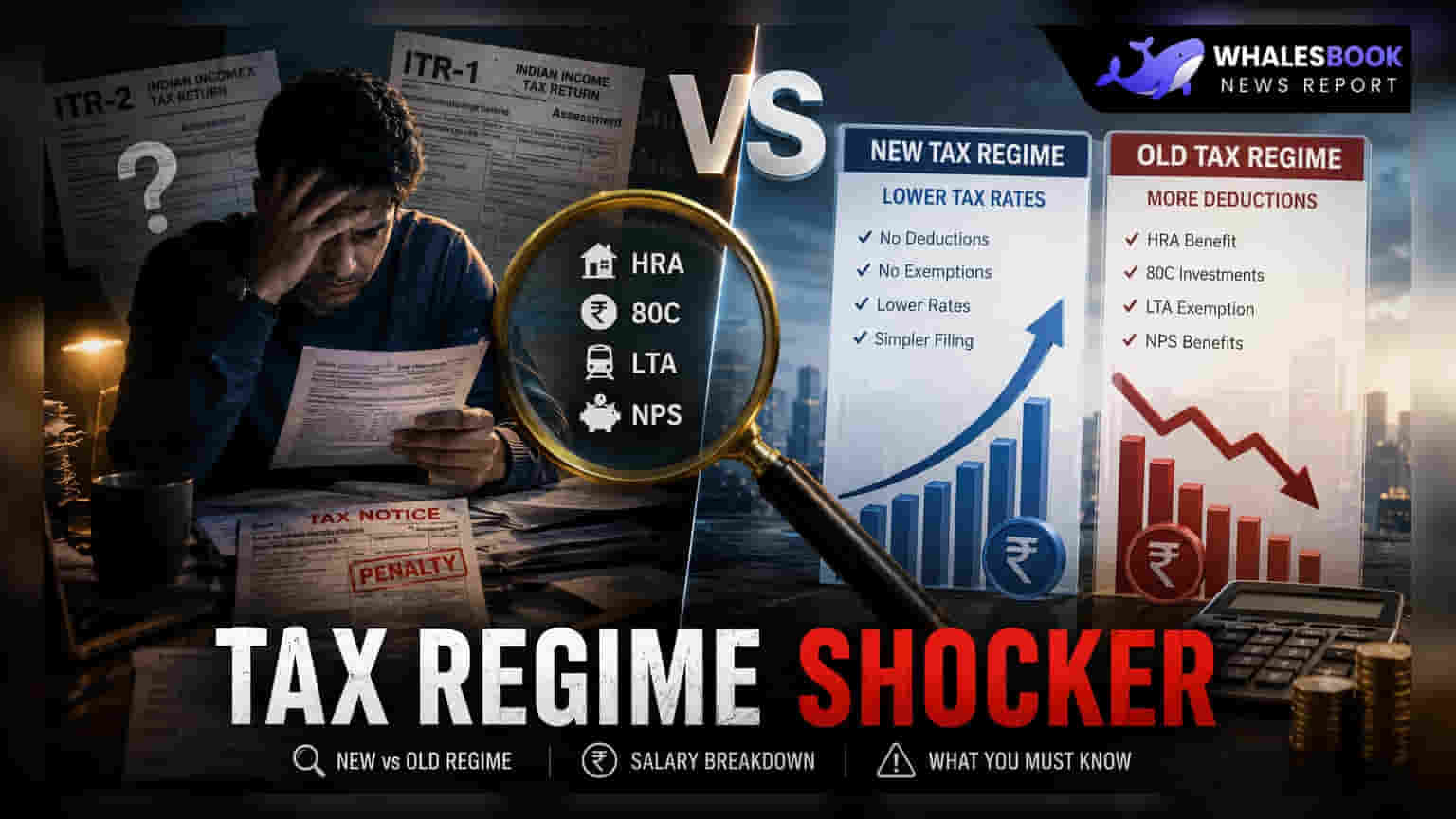

Choosing between India's old and new tax regimes requires a detailed look at your salary components like HRA, LTA, and Section 80C investments. While the new regime offers lower tax rates, losing common deductions can lead to a higher total tax burden for many employees. A careful calculation of your specific exemptions is essential before submitting your tax declaration to your employer.

As employers begin the process of collecting tax regime declarations, many salaried individuals are facing the complex choice between the traditional old tax regime and the newer, simplified structure. While the new regime is often marketed for its lower tax slab rates, the decision is not as simple as comparing percentages. The actual tax outflow depends heavily on how much an individual can claim through various exemptions and deductions.

The HRA and Home Loan Trade-off

One of the most significant factors for many taxpayers is the House Rent Allowance (HRA). Under the old tax regime, HRA is a crucial tax-saving tool for those living in rented accommodation. This benefit is generally not available in the new regime. Similarly, homeowners who rely on deductions for home loan interest under Section 24(b) and principal repayment under Section 80C often find that the tax savings under the old system outweigh the benefits of the lower rates in the new system. For individuals with large mortgage payments, the shift to the new regime can lead to a noticeable increase in their annual tax liability.

Evaluating 80C and Other Allowances

Many popular tax-saving investments fall under Section 80C, including Employee Provident Fund (EPF), Public Provident Fund (PPF), Equity Linked Savings Schemes (ELSS), and life insurance premiums. These are excluded in the new regime, meaning that if you are a disciplined investor who regularly utilizes the 80C limit, the new regime may feel less attractive. Additionally, common benefits such as Leave Travel Allowance (LTA), children's education allowance, and professional tax deductions are also structured primarily for the old regime. Employees who frequently use these allowances should calculate their total tax-exempt income to see if the new tax rates are enough to compensate for these losses.

Strategic Benefits in the New System

Despite the loss of many deductions, the new regime does retain some efficiency for specific salary components. Employer contributions to the National Pension System (NPS), recognized provident funds, and superannuation funds remain tax-efficient up to their respective limits. This can be particularly beneficial for high-earners or senior management whose compensation packages include significant retirement benefits. Furthermore, individuals with simpler salary structures—those who do not have large rent payments, home loans, or a high volume of tax-saving investments—often find the new regime easier to manage because it requires less documentation and compliance.

Making an Informed Decision

Because there is no single best choice for everyone, the decision must be personalized based on your annual income and expense profile. Before finalizing your declaration, it is advisable to create a side-by-side comparison. List your current HRA, LTA, 80C investments, and interest payments to determine your total taxable income under both regimes. For the upcoming tax year, consider how your projected travel, housing costs, and investment plans might change. If your salary structure is complex, this calculation will reveal which option truly minimizes your tax outflow for the year.