What Happened

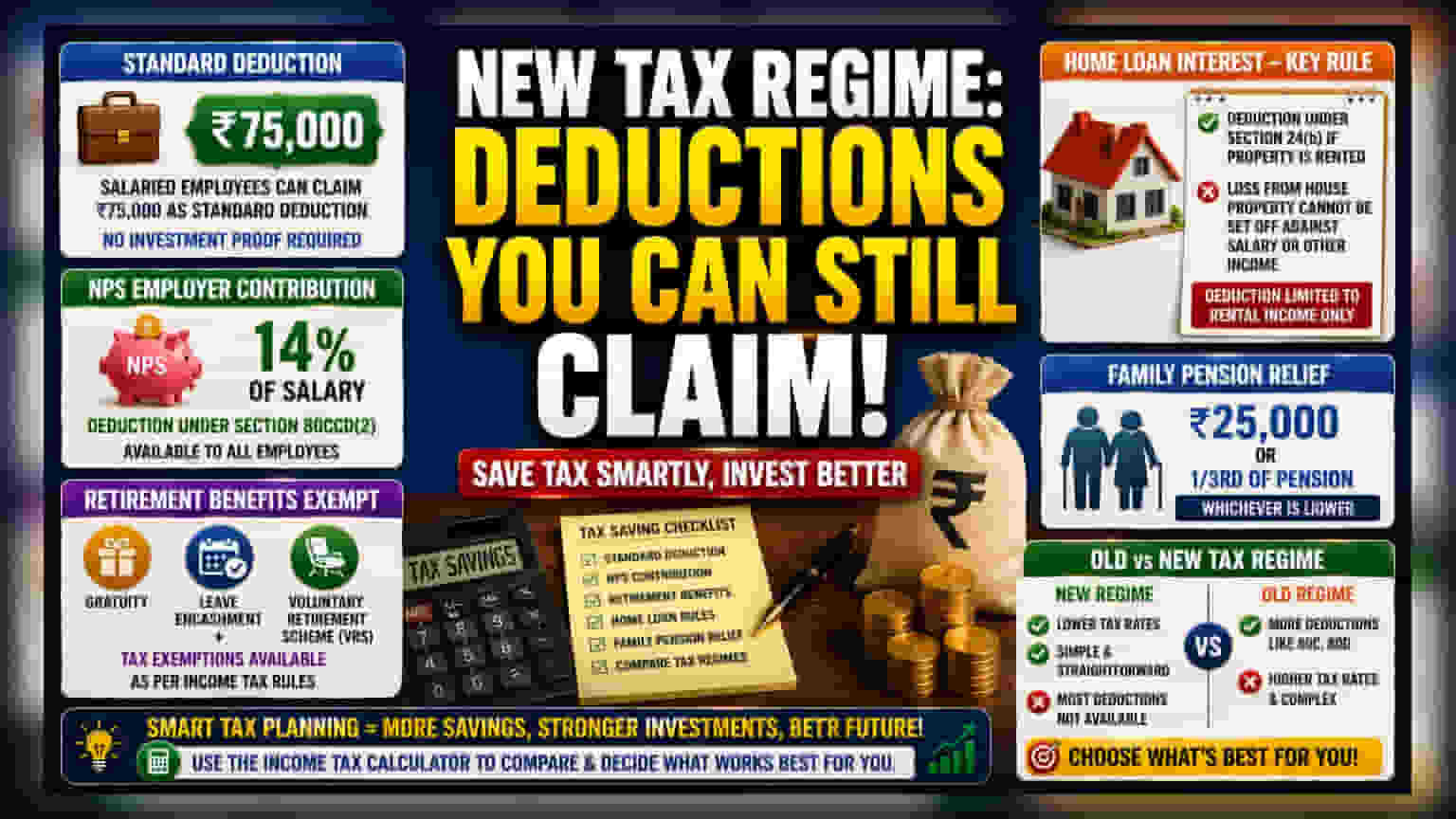

There is a common misunderstanding that the new tax regime in India does not allow for any tax deductions. While it is designed to be simpler and has removed many older tax-saving exemptions, several important deductions still exist. For salaried individuals, the most notable is the standard deduction. Under the current tax rules, salaried employees can claim a standard deduction of Rs 75,000, which is subtracted directly from their gross salary to arrive at the taxable income without requiring any specific investment proof.

Why This Matters For Investors

For an investor, taxes are a direct cost that reduces the money available for savings and monthly investments. Knowing exactly what you can claim helps you calculate your true take-home pay and plan your SIPs or other financial goals more accurately. Misunderstanding the tax rules can lead to poor financial planning, where you might overestimate or underestimate your tax liability, affecting your ability to commit to long-term investment plans.

Key Deductions Explained

Apart from the standard deduction, employer contributions to the National Pension System (NPS) remain a significant benefit. Under Section 80CCD(2), employees can claim a deduction for employer contributions up to 14% of their salary. This benefit is available to both government and private sector employees. Additionally, specific retirement benefits are preserved in the new regime. These include tax exemptions on gratuity, leave encashment, and compensation received under the Voluntary Retirement Scheme (VRS), provided they meet the conditions set by the tax department.

The Home Loan Interest Catch

It is important to understand the specific rules regarding home loans. While you can claim a deduction for interest paid on a home loan under Section 24(b) if the property is rented out, there is a specific restriction to keep in mind. You cannot use any loss from house property to reduce your tax liability against other sources of income, such as your salary. This means the deduction is only useful up to the extent of your rental income. Investors should be careful not to confuse this with the old tax regime, where home loan interest could be adjusted against other income sources.

Family Pension Relief

For individuals who receive a family pension, the tax rules provide a specific relief measure. Taxpayers are allowed to claim a deduction of Rs 25,000 or one-third of the pension amount, whichever is lower. This helps in lowering the overall taxable income for family pensioners.

What Investors Should Track

The primary decision for any taxpayer is choosing between the old and new tax regimes. The new regime is often preferred for its lower tax rates, but it excludes many popular deductions like 80C and 80D investments. Investors should regularly use the official income tax calculator provided by the government to compare their total tax outgo under both systems based on their specific income, investments, and expenses. This decision is not one-size-fits-all and depends entirely on your personal financial situation and goals.