For FY 2026-27, understanding National Pension System (NPS) tax benefits is essential for tax planning. While the old regime offers wider deductions including the extra Rs 50,000 limit, the new regime focuses primarily on tax-exempt employer contributions. Knowing these differences can help you structure your income and avoid reporting errors during ITR filing.

What Happened

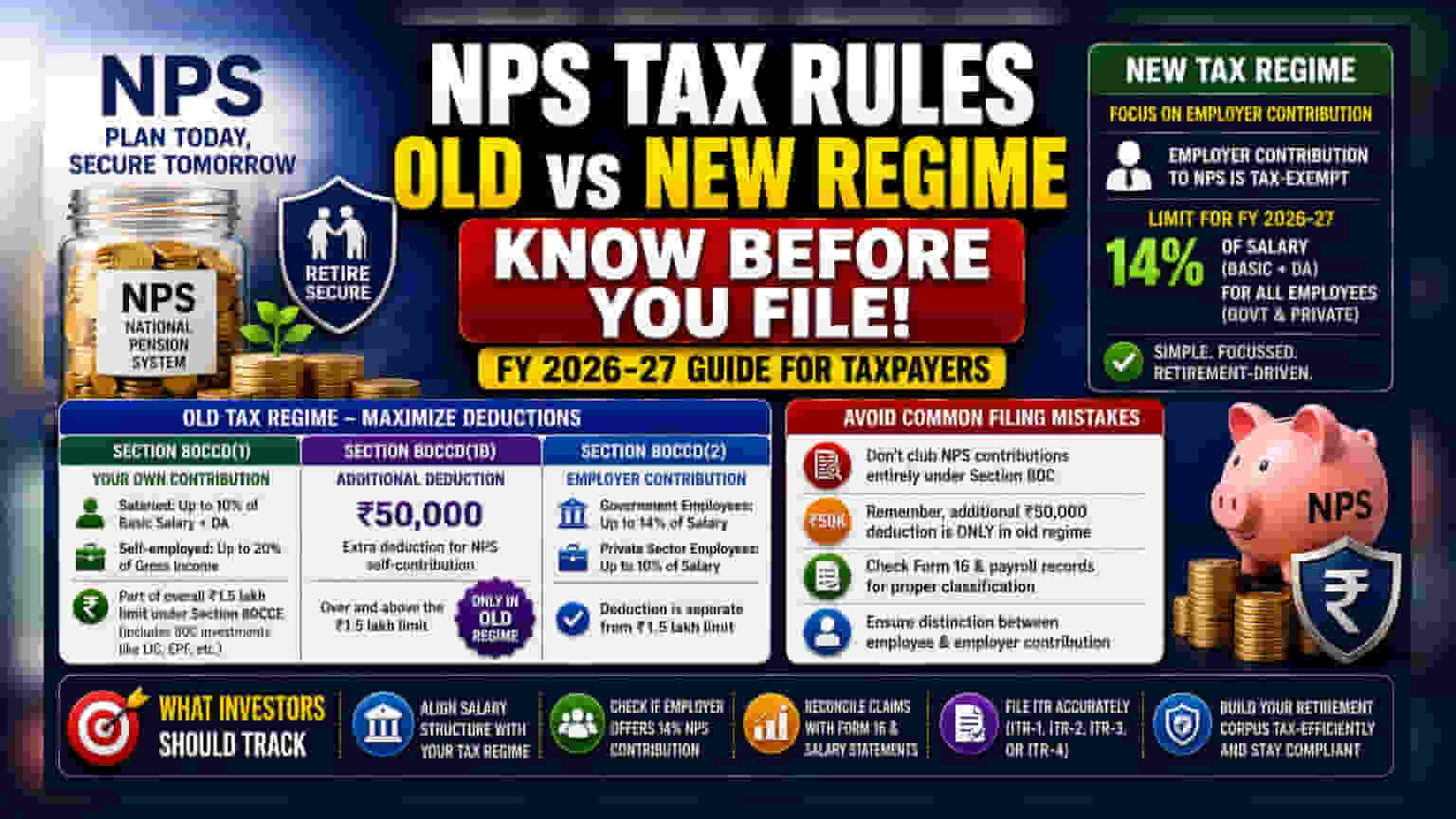

For the financial year 2026-27, the National Pension System (NPS) continues to be a key tool for retirement planning, but its tax treatment changes significantly depending on whether you choose the old or the new tax regime. Taxpayers need to be aware of how different sections of the Income Tax Act apply to their contributions to ensure they do not lose out on potential savings or file their returns incorrectly.

Deductions Under the Old Regime

The old tax regime is more flexible for those who want to maximize deductions. Under this regime, you can claim benefits through three main channels:

- Section 80CCD(1): This covers your own contributions to NPS. Salaried employees can claim up to 10% of their basic salary plus dearness allowance, while self-employed individuals can claim up to 20% of their gross income. Crucially, this deduction is part of the overall Rs 1.5 lakh limit under Section 80CCE, which also includes common investments like life insurance and EPF.

- Section 80CCD(1B): This is a powerful feature of the old regime. It allows an additional deduction of Rs 50,000 specifically for NPS self-contributions, over and above the standard Rs 1.5 lakh limit. This helps taxpayers lower their taxable income further.

- Section 80CCD(2): This relates to employer contributions. Government employees can claim up to 14% of their salary, while private sector employees can claim up to 10%. This deduction is separate from the Rs 1.5 lakh limit.

Benefits Under the New Regime

The new tax regime simplifies things by removing many deductions but keeping the focus on employer-led retirement savings. In the new regime, the primary benefit is the tax-exempt status of the employer's contribution to your NPS account. For FY 2026-27, this employer contribution limit is set at 14% of your salary (basic plus dearness allowance) for both government and private sector employees. This is a notable point, as it allows private employees to benefit from the higher 14% limit typically reserved for the government sector.

Avoiding Common Filing Mistakes

A common issue during tax filing is the misclassification of NPS contributions. Many taxpayers accidentally group their entire contribution under Section 80C instead of separating it, or they forget that the additional Rs 50,000 deduction is exclusive to the old regime. To avoid issues with the Income Tax Department, it is important to:

- Review your Form 16 and payroll records carefully to see how your employer has categorized your NPS contribution.

- Check if you are eligible for the specific deduction under your chosen regime before filing your ITR.

- Ensure that contributions are clearly distinguished as either 'employee contribution' or 'employer contribution' in your records.

What Investors Should Track

For the current financial year, the most important step is to align your salary structure with your tax regime choice. If you are under the new regime, checking if your employer offers the 14% contribution can be a strategic way to build your retirement corpus in a tax-efficient manner. Always reconcile your tax saving claims with your final salary statements and Form 16 before submitting your ITR-1, ITR-2, ITR-3, or ITR-4 forms.