The Silent Wealth Drain

Mutual fund investors diligently saving via Systematic Investment Plans (SIPs) can face significant wealth erosion, not due to market crashes, but from an often-overlooked cost: the expense ratio. Two investors making identical Rs 20,000 monthly SIPs into the same fund for 20 years could see one end up with Rs 20 lakh less than the other, purely due to this cost.

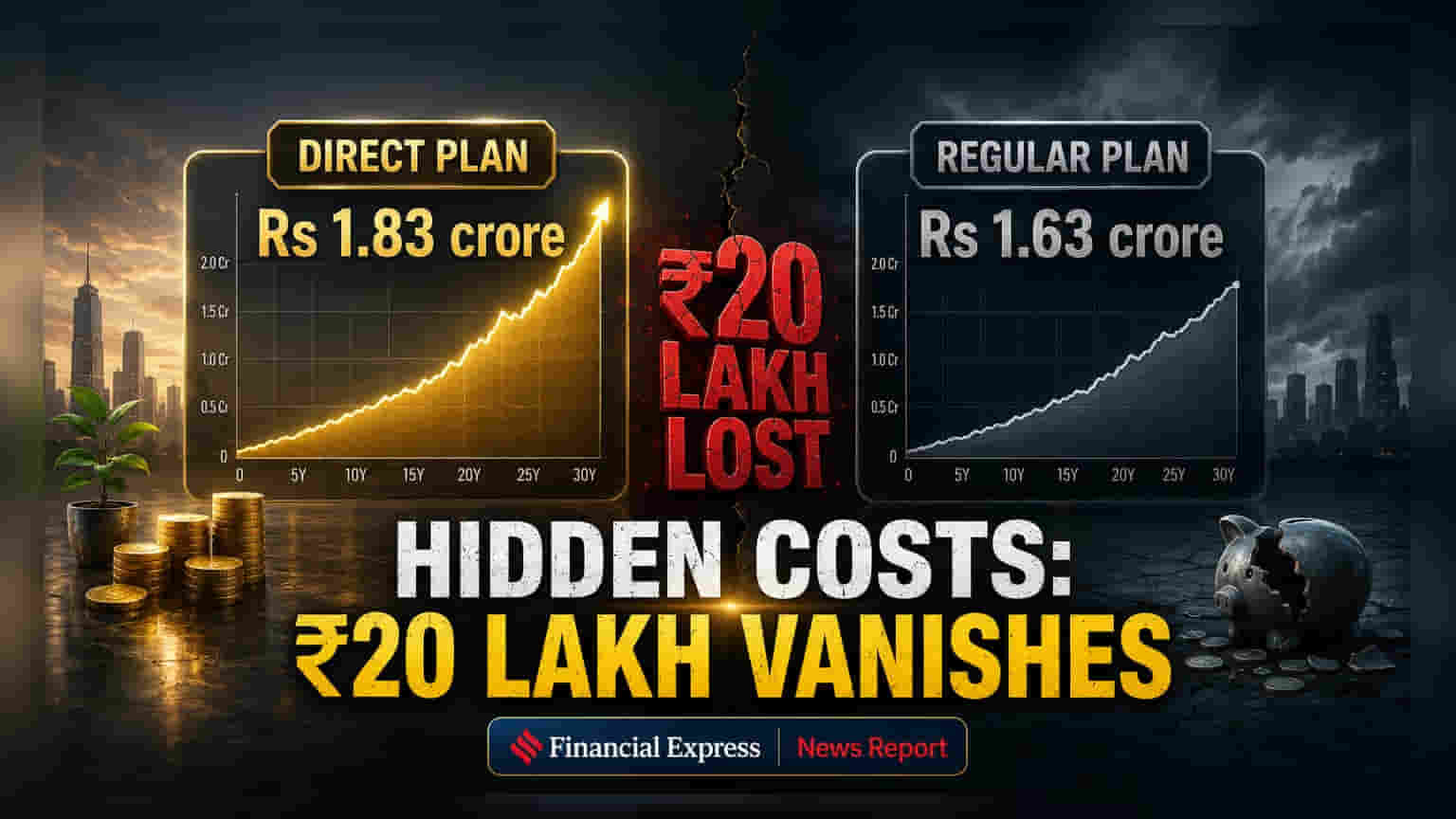

Direct vs. Regular Plans

The critical distinction lies between 'Regular' and 'Direct' mutual fund plans. Regular Plans include a commission for distributors or brokers, typically adding 0.5% to 1.2% annually to the expense ratio. This fee is deducted before the Net Asset Value (NAV) is calculated, making it invisible to the investor. Direct Plans, invested in without intermediaries, carry a lower expense ratio by the same margin.

Compounding Costs Over Time

While a 1% annual difference might seem negligible, its impact compounds significantly over two decades. An analysis suggests this can create a Rs 20 lakh gap, with one investor accumulating Rs 1.63 crore and the other Rs 1.83 crore, assuming 11% and 12% annual returns, respectively. This demonstrates how seemingly small percentages can lead to substantial wealth discrepancies in long-term investing.

Real-World Expense Ratios

Actual expense ratios illustrate this point starkly. For instance, the Edelweiss Mid Cap Fund shows a direct expense ratio of 0.60% compared to 1.80% for its regular plan, a difference of 1.20%. Similarly, the Invesco India Mid Cap Fund has a 1.04% direct expense ratio against a 2.17% regular plan, a 1.13% disparity. These figures highlight the material impact on investor returns over time.

The Advisor Dilemma

While a good financial advisor providing personalized advice and portfolio management can justify the higher cost of a Regular Plan, the issue arises when investors pay these commissions without receiving ongoing, valuable guidance. Many investors remain in Regular Plans sold years ago, with no active advisor reviewing their portfolio, yet the commission continues to be deducted annually.

Making Informed Decisions

Investors contemplating a switch from Regular to Direct Plans must consider exit loads and potential capital gains tax implications. A thorough assessment of personal needs is crucial: if an investor can independently research, track their portfolio, and avoid emotional trading, a Direct Plan is likely more beneficial. However, for those relying on professional financial advice, the cost of a Regular Plan might be justifiable if genuine value is provided.