Missing an EMI is more than just a late payment; it is a critical signal for both borrowers and investors. While delinquency refers to an overdue payment, default is a severe financial breach usually marked after 90 days. For borrowers, this distinction is the difference between a minor credit blip and a long-term mark on their record. For investors, monitoring these stages is essential to assess the health of banking and finance stocks, as they directly influence a lender's asset quality and profit margins.

What Happened

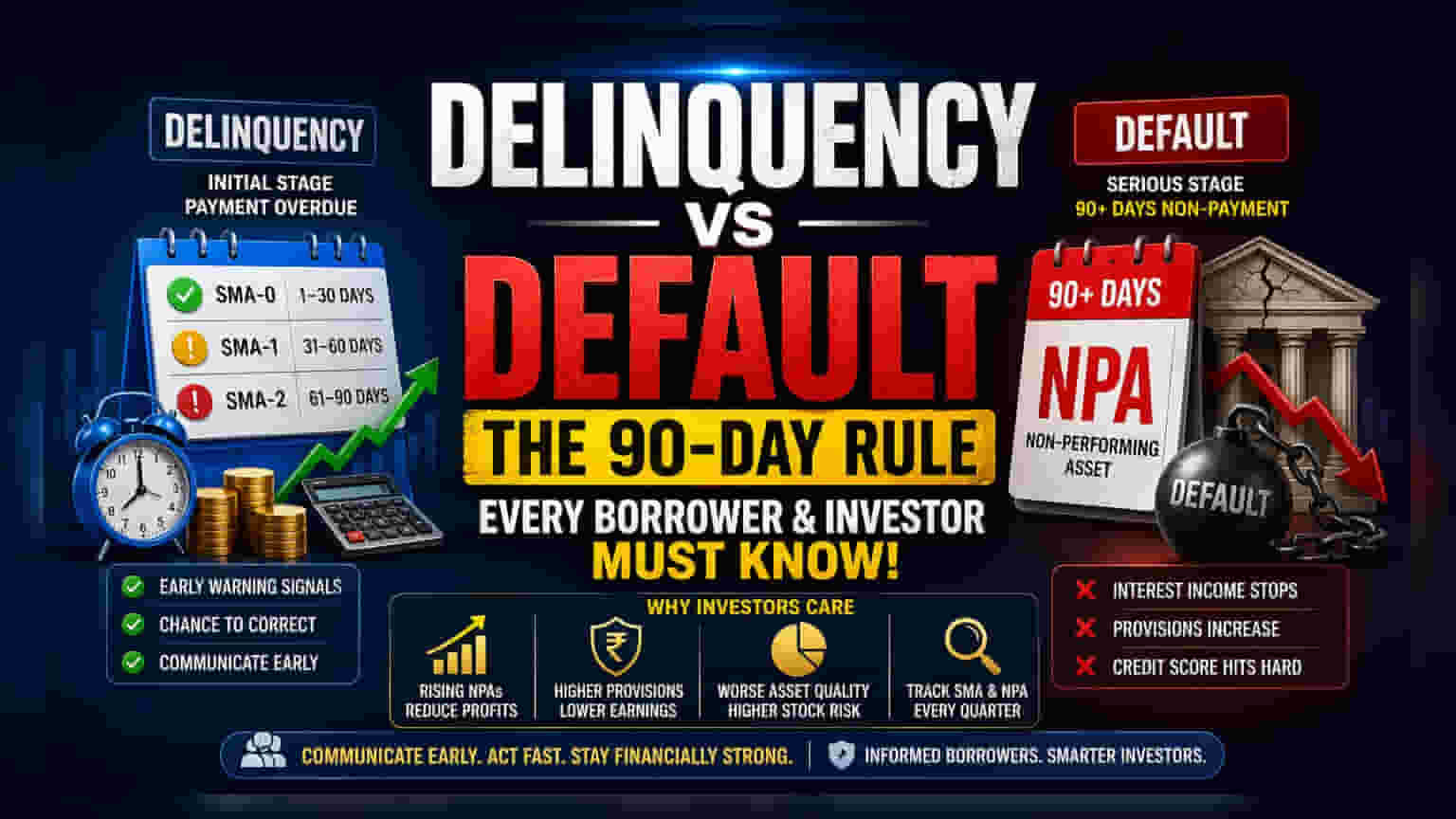

Borrowers often use the terms delinquency and default interchangeably, but in the financial world, they represent two very different stages of loan repayment. Delinquency is the initial stage where a payment becomes overdue. This happens when an EMI is missed or a cheque bounces. In contrast, default is a more serious state that usually occurs after a prolonged period of non-payment, typically exceeding 90 days. Understanding this timeline is essential for anyone managing personal debt or analyzing the performance of banking and non-banking finance company (NBFC) stocks.

The Crucial 90-Day Threshold

In the Indian banking system, the distinction between delinquency and default is formally recognized through regulatory guidelines. When a borrower misses a payment, the loan enters the Special Mention Account (SMA) category. Banks track these in buckets, such as SMA-0 for 1-30 days overdue, SMA-1 for 31-60 days, and SMA-2 for 61-90 days. These buckets serve as early warning signals for the lender. If the borrower does not clear the dues within 90 days, the loan is classified as a Non-Performing Asset (NPA). This 90-day mark is the technical definition of a default from a lender's perspective. Once an account becomes an NPA, the lender must stop counting the unpaid interest as income and is often required to set aside capital as a provision to cover potential losses.

Why This Matters for Investors

For stock market investors, the movement of loans from delinquency to default is a primary indicator of a lender's business health. When a bank or NBFC reports a rise in delinquency, it suggests that their customers are under financial stress, which may lead to higher defaults in the future. If a large portion of a bank’s loan book shifts from standard accounts to SMA buckets, the bank may eventually have to increase its provisions. Higher provisions directly reduce the net profit of the company. Investors often track 'asset quality' metrics, such as Gross NPA ratios and Net NPA ratios, to gauge how effectively a lender is managing its risk. A company with a rapidly growing NPA ratio is often viewed as carrying higher risk, which can weigh on its stock valuation.

Impact on Credit Health

For individual borrowers, the impact is equally significant. A single missed EMI, even if it is only a few days late, gets reported to credit bureaus. While this might not be classified as a default immediately, it shows up as a delinquency on the credit report. A history of repeated delinquencies can lower a credit score, making it harder to secure loans or credit cards in the future. By the time a loan reaches the default stage, the damage to the credit score is substantial. Recovering from a default is a long process that can limit an individual’s financial flexibility for years.

The Importance of Early Communication

Financial stress can happen due to unexpected life events such as job loss or medical emergencies. The most effective way to manage these situations is through early communication. Lenders often have mechanisms to restructure loans or offer temporary relief if a borrower approaches them before the loan hits the 90-day default threshold. Proactive communication helps borrowers avoid the severe consequences of default and helps lenders maintain a healthier loan book. Investors often look for management commentary in quarterly earnings reports to see if the company is effectively engaging with stressed borrowers to prevent defaults.

What Investors Should Track

Investors looking at the banking and finance sector should monitor quarterly updates on asset quality. Key monitorables include the movement in SMA buckets, changes in Gross and Net NPA ratios, and the company's provisioning coverage ratio. These figures provide insight into whether the lender is successfully containing delinquency or if there is an underlying risk of rising defaults. Management commentary on collection efficiency and the health of specific loan segments, such as retail or corporate, also provides critical context for the company's future earnings.