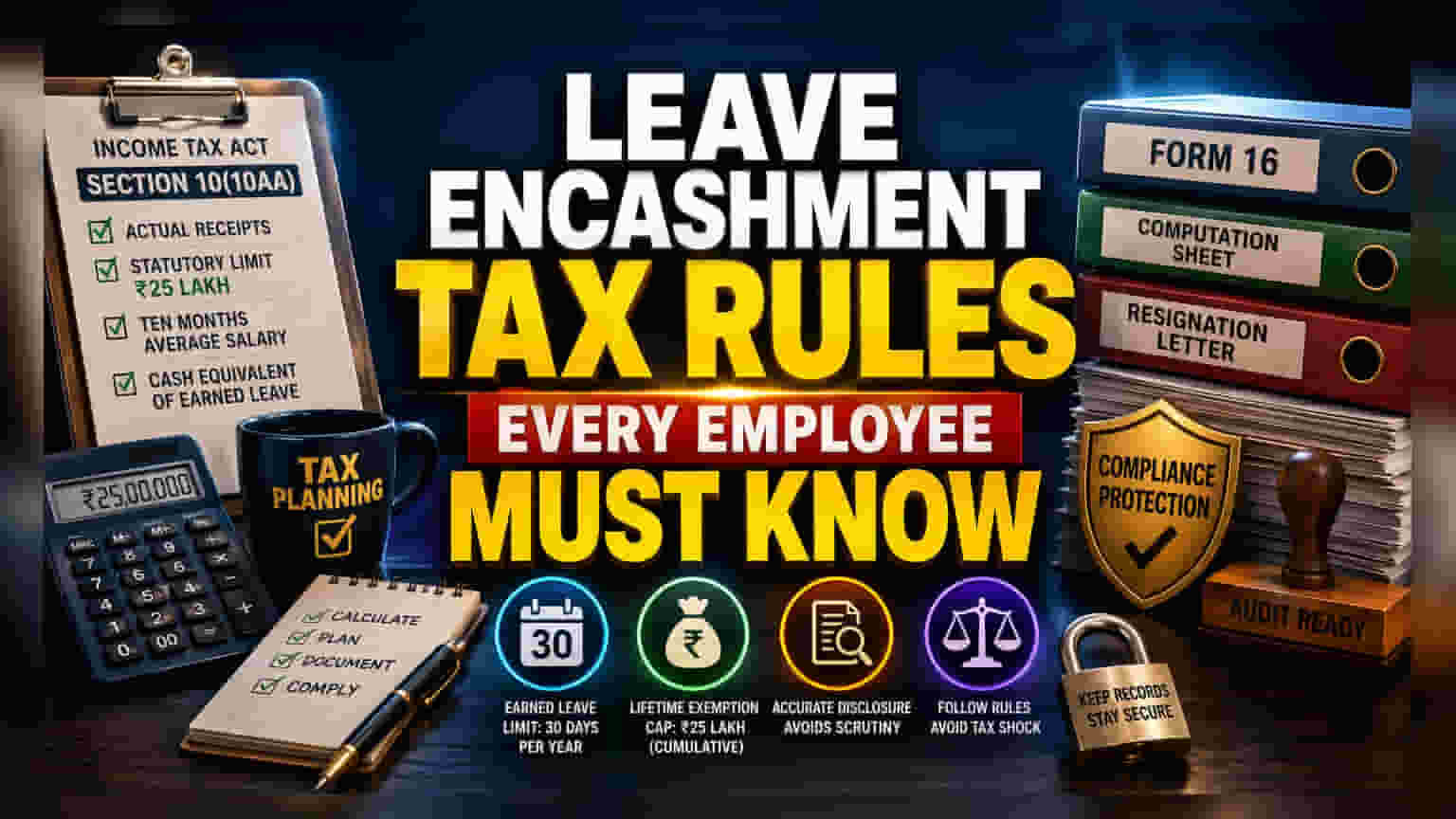

The Mechanics of Section 10(10AA)

The fiscal framework governing leave encashment for Assessment Year 2026-27 remains anchored in Section 10(10AA) of the Income-tax Act. While the headline Rs 25 lakh cap often dominates the narrative, the actual tax liability is frequently determined by the interaction between average salary calculations and specific accrual limits. For private sector employees, the exemption is not a flat threshold but a restrictive ceiling derived from the minimum of four distinct variables: actual receipts, the statutory limit, ten months of average salary, or the cash equivalent of earned leave.

Complexity in Salary Averaging

A critical oversight for many taxpayers involves the interpretation of the 'ten-month average salary.' This figure is calculated based on the ten months immediately preceding retirement or resignation, including basic salary, dearness allowance, and commission tied to fixed percentages of turnover. Discrepancies often arise when employers apply different methodologies for calculating 'earned leave,' particularly if internal company policies exceed the standard 30-day accumulation cap per year of service. Tax authorities strictly disregard any leave exceeding this 30-day regulatory mandate, often leading to unexpected taxable amounts for high-earning individuals who have accrued significant leave balances over long tenures.

The Forensic Audit Trail

The lifetime nature of the Rs 25 lakh exemption necessitates a rigorous approach to historical record-keeping. Because the limit applies cumulatively across an individual's career, failure to disclose previous exemptions claimed during earlier job changes can trigger automated scrutiny from the Income Tax Department. Taxpayers are advised to maintain a permanent digital or physical file containing Form 16, comprehensive employer-provided computation sheets, and formal resignation correspondence. These documents serve as the primary defense against potential reassessment notices, especially when inconsistencies appear between declared salary income and the exempt allowance portion reported under Schedule S.

Structural Risks and Compliance Hazards

The primary danger for employees lies in the misclassification of encashment received during active employment versus at the point of separation. Encashment received while still in service is fully taxable, regardless of the Rs 25 lakh limit, which only applies upon retirement, resignation, or superannuation. Furthermore, shifting between the old and new tax regimes does not negate the statutory requirements of Section 10(10AA); however, failing to accurately reflect these claims in the specific 'Allowances to the extent exempt' column can lead to the outright rejection of the deduction during automated processing, necessitating lengthy rectification procedures.