Taxpayers filing returns face higher scrutiny on HRA claims as the Income Tax Department uses data analytics to spot discrepancies. To avoid notices, ensure your rent agreements, receipts, and landlord PAN details are consistent with your Annual Information Statement (AIS). Most importantly, verify if you are eligible, as HRA exemptions do not apply under the New Tax Regime.

What Happened

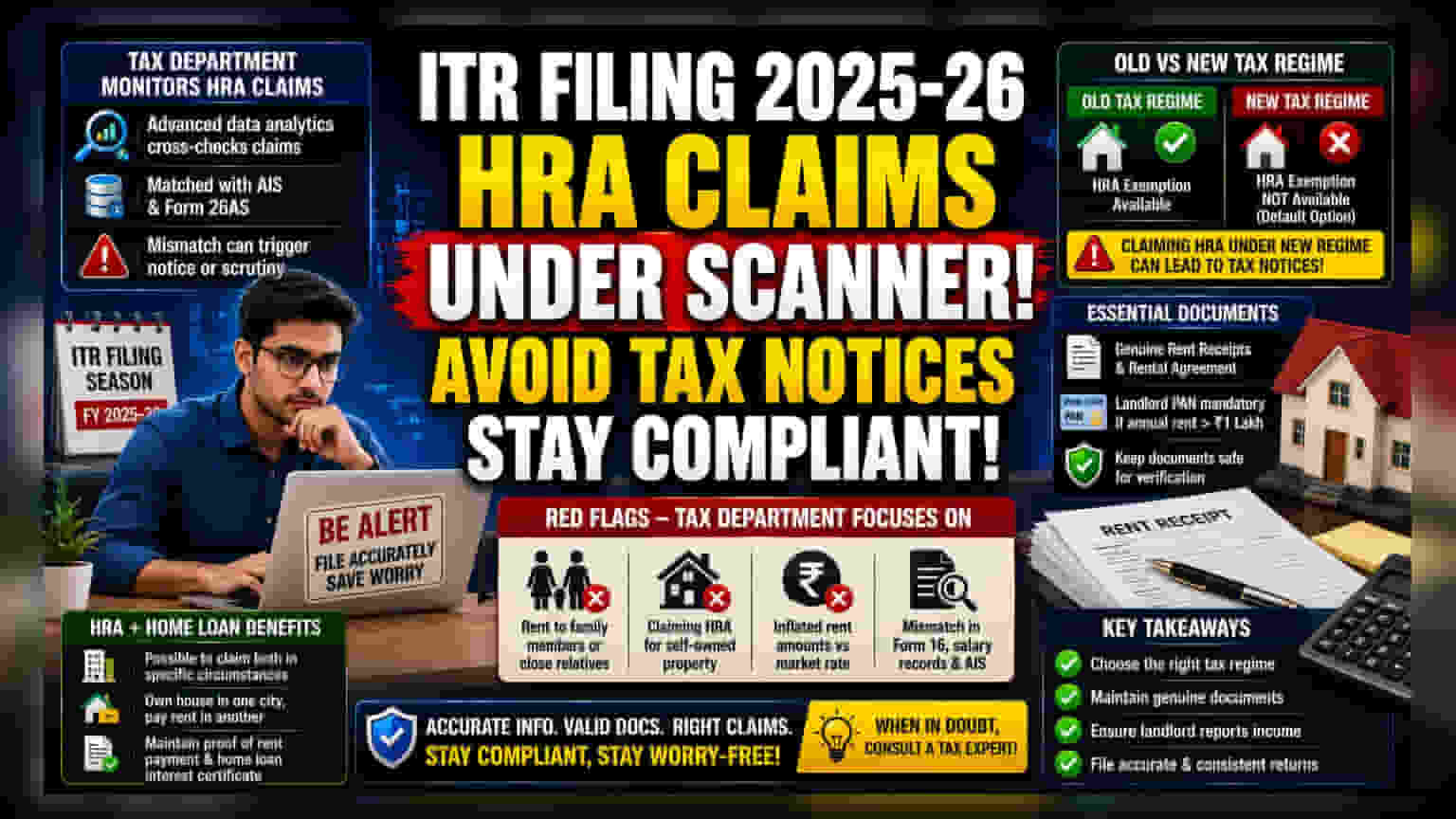

As the Income Tax Return (ITR) filing season for the financial year 2025-26 progresses, the Income Tax Department is significantly increasing its monitoring of House Rent Allowance (HRA) claims. Tax authorities are now using advanced data analytics to cross-check the claims made by salaried individuals against the financial information disclosed in their Annual Information Statement (AIS) and Form 26AS. This means that if the rent details reported by an employee do not match the income disclosures made by the landlord or the actual financial records, it is likely to trigger an automated notification or scrutiny notice.

The New Regime Distinction

A critical point of confusion for many taxpayers is the difference between the Old and New Tax Regimes. Under the New Tax Regime, which is the default option for most taxpayers, the HRA exemption is not available. Many taxpayers inadvertently claim HRA while opting for the New Tax Regime, which inevitably leads to tax department notices for tax underpayment. Before submitting the ITR, it is essential to confirm whether the tax regime selected actually allows for the HRA deduction.

Essential Documentation

For those eligible under the Old Tax Regime, documentation is the first line of defense against tax notices. Taxpayers must ensure they possess genuine rent receipts and a valid rental agreement. For any annual rent exceeding ₹1 lakh, furnishing the landlord's Permanent Account Number (PAN) is mandatory. The tax department matches the landlord’s PAN with their own income tax filings to ensure that the rental income is being reported correctly. Discrepancies here are a primary cause for scrutiny.

Common Pitfalls and Red Flags

Tax authorities are increasingly focused on identifying "sham" arrangements. Claims that are frequently flagged include paying rent to family members or close relatives while residing in the same house, or claiming HRA for a self-owned property without a genuine, documented reason. Data analytics systems are designed to detect if the "landlord" is a family member who has not declared the rental income, or if the rent amount is significantly inflated compared to the market rate for the area. Filing returns with consistent information across Form 16, salary records, and the AIS is vital to avoiding these red flags.

Combining HRA and Home Loan Benefits

It is possible to claim both HRA exemption and a home loan interest deduction simultaneously, but only under specific circumstances. For instance, if an individual owns a house in one city but is employed and paying rent in another, they may claim both. However, simply owning a property does not automatically disqualify one from HRA if the conditions are met. Conversely, claiming HRA for a property owned by the taxpayer in the same city is generally not permitted unless there is a valid, logical reason for living elsewhere. Taxpayers should ensure that they have proof of both rent payment and the home loan interest certificate to support these dual claims if they are ever reviewed by the tax department.