Home loans are long-term commitments where early EMIs primarily pay off interest rather than the loan amount. Borrowers facing floating interest rates should monitor how rate changes affect their loan tenure. Strategically using bonuses or surplus funds to reduce the principal can save lakhs in total interest costs and significantly shorten the repayment duration.

What Happened

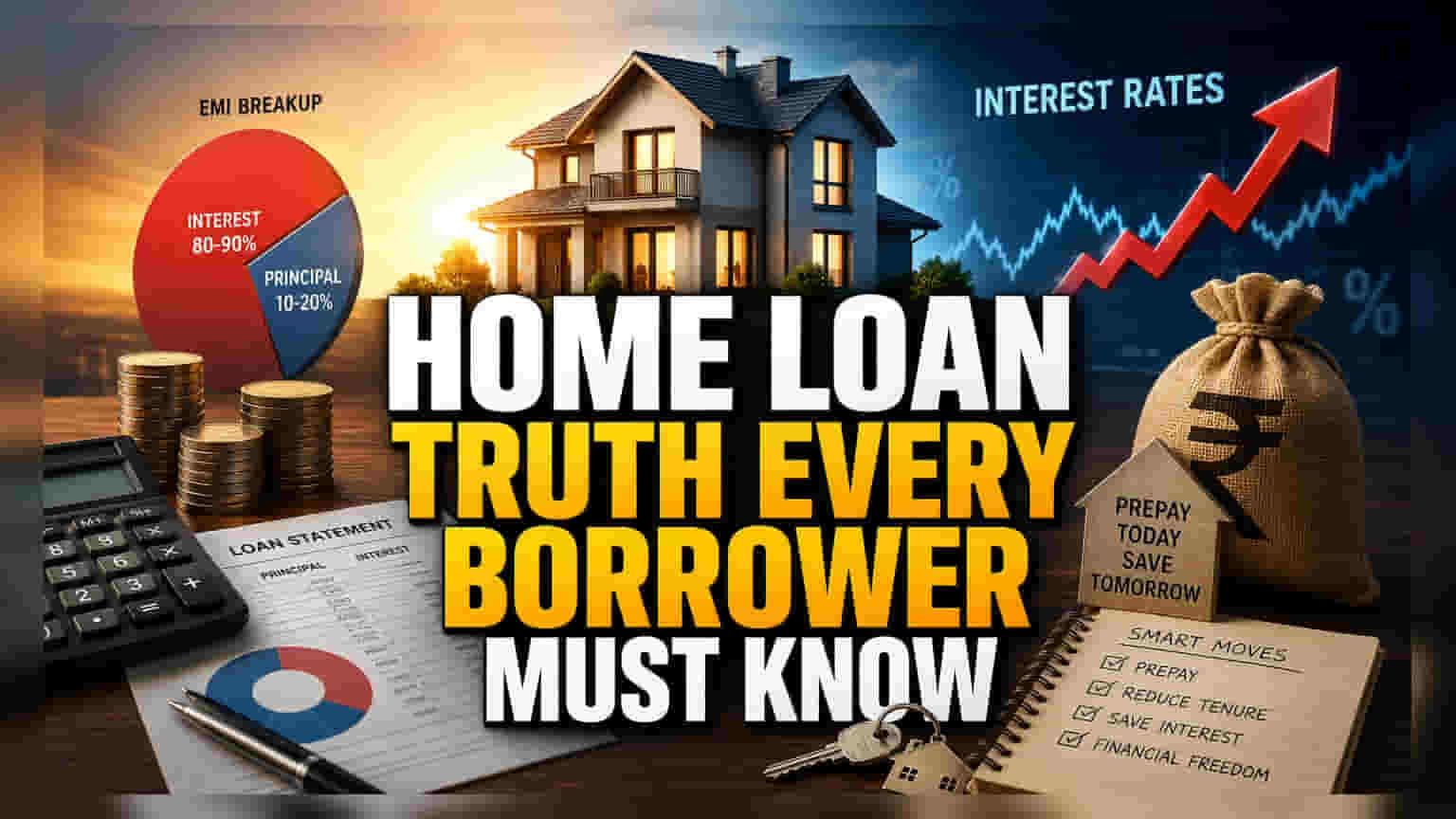

For many Indian families, a home loan is the largest financial liability they will ever undertake. While the Equated Monthly Installment (EMI) is often the focus of monthly budgeting, the underlying structure of home loan repayment is frequently misunderstood. In the initial years of a long-term loan, the majority of the EMI goes toward interest payments, with only a small portion reducing the actual loan amount. This creates a situation where the outstanding balance of the loan decreases much slower than many borrowers anticipate.

The Mechanics Of Home Loan Repayment

Most home loans follow a structured repayment schedule designed to balance the bank's interest income with the borrower's cash flow. When a borrower starts their loan journey, the interest is calculated on the entire outstanding amount. As the loan progresses and the principal amount is paid down, the interest component decreases, and the principal component of the EMI rises. This is why a quick check of the loan account after two or three years can be surprising; despite paying regular EMIs, the principal may appear largely untouched. This is not a mistake by the bank but a standard feature of how long-term lending works.

The Impact Of Floating Rates

Most home loans in India are linked to floating interest rates, meaning the rate can change based on the repo rate set by the Reserve Bank of India or the bank's own internal benchmarks. When interest rates rise, the bank typically extends the loan tenure rather than immediately increasing the EMI, unless the borrower requests otherwise. This can lead to a silent escalation in the total cost of the loan. Over a 20-year period, even a small increase in the interest rate can add significant amounts to the total repayment figure, effectively turning a medium-sized loan into a much more expensive liability.

The Math Behind Prepayments

One of the most effective ways to manage this liability is through prepayments. When a borrower makes an extra payment toward the principal—using a bonus, investment maturity, or other surplus funds—the effect is immediate. Because interest is calculated on the remaining principal, reducing that balance early cuts the interest accrued on that amount for all future months. Small, consistent prepayments can reduce the total repayment period by years and save a substantial amount of money in interest costs.

The Opportunity Cost Debate

While prepaying a home loan saves interest, borrowers often face a choice between debt repayment and other investments. If the home loan interest rate is lower than the potential post-tax return from equity markets or other high-growth assets, some investors prefer to invest their surplus cash instead of prepaying the loan. However, prepaying the loan provides a guaranteed return equal to the home loan interest rate, which is a risk-free saving. The best approach depends on an individual’s risk appetite, current tax bracket, and the specific interest rate on their loan.

What Investors Should Track

Borrowers should regularly check their loan statement to see the split between principal and interest. If the interest rate environment is rising, it is essential to ask the lender how the changes are affecting the loan tenure. Furthermore, setting a goal to make at least one extra EMI payment per year can significantly alter the trajectory of the loan, turning a 20-year debt into a shorter, more manageable commitment.