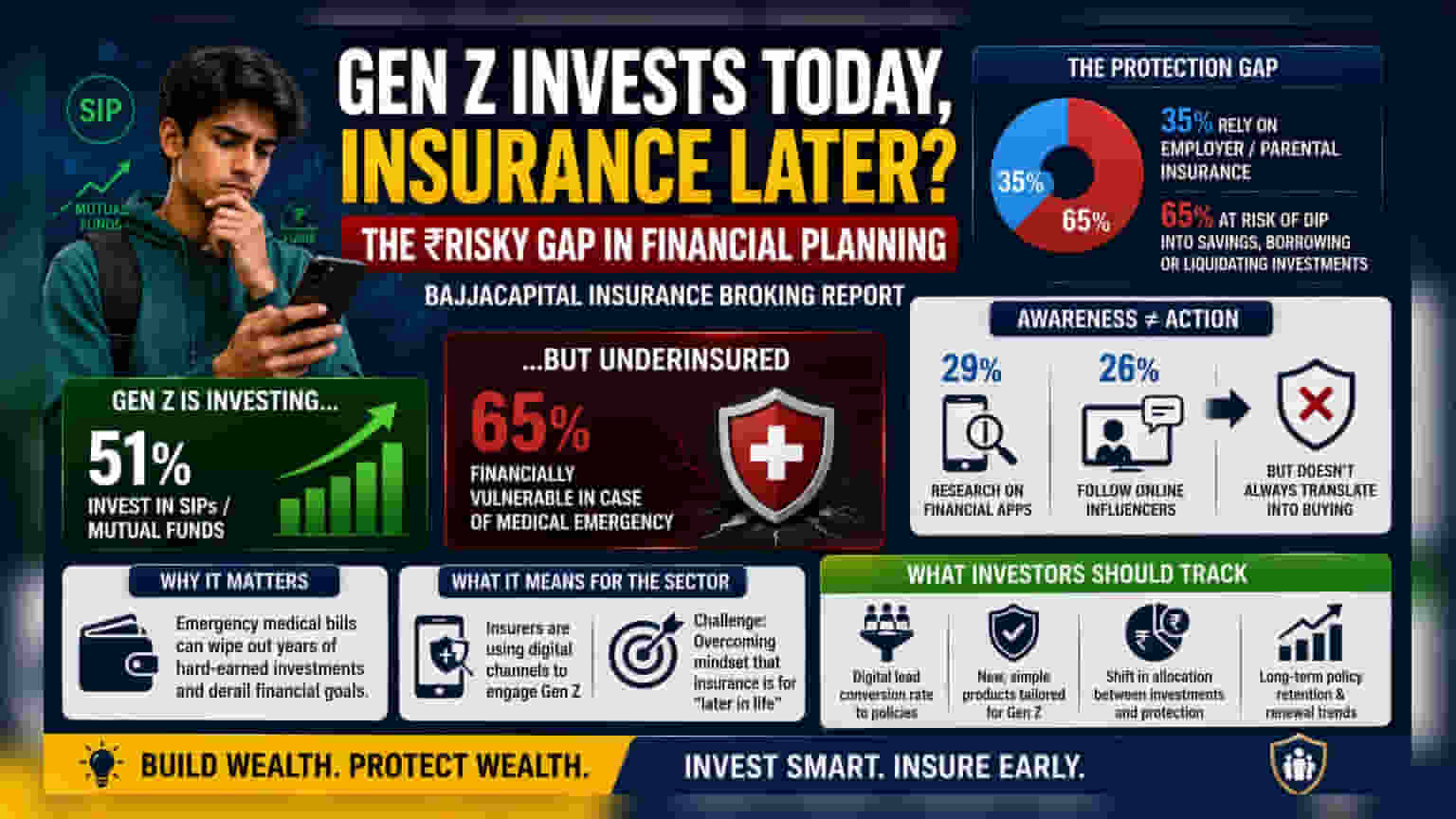

A report by BajajCapital Insurance Broking finds that while 51% of Gen Z invest in mutual funds and SIPs, many are delaying health insurance. This creates a financial risk, as 65% remain vulnerable to high medical costs. Despite high digital awareness, this gap between research and purchasing behavior remains a challenge.

What Happened

A new report by BajajCapital Insurance Broking has highlighted a distinct trend in the financial behavior of India’s Gen Z. The data shows that while this generation is actively building wealth through Systematic Investment Plans (SIPs) and mutual funds—with 51% participation—there is a significant lag in purchasing personal health insurance. Many young adults are viewing insurance as a product to be bought only after reaching their 30s or reaching major life milestones, rather than a necessary financial safety net.

The Financial Protection Gap

For investors and young adults, this trend creates a potential long-term issue. The report indicates that 65% of Gen Z individuals are financially vulnerable if they face a serious medical emergency. While 35% of the demographic rely on employer or parental insurance cover, the majority are at risk of having to dip into their savings, borrow money, or liquidate their investments to cover healthcare costs. This effectively works against their wealth creation goals, as emergency medical bills can wipe out years of disciplined investment in SIPs.

Digital Awareness vs. Buying Behavior

The research points to a clear disconnect between digital engagement and actual financial action. While 29% of Gen Z individuals use financial apps to research options and 26% consult online influencers, this awareness does not always translate into buying a policy. This "activation problem" suggests that while information is easily available, the step from being aware of insurance to actually purchasing it is where the process often stalls.

What This Means for the Sector

This behavior is a crucial monitorable for the Indian insurance sector. Insurance companies are increasingly using digital platforms to target younger buyers, hoping to bridge the gap between financial awareness and policy adoption. The challenge for these companies is not just reaching the customer, but overcoming the mindset that insurance is a product for later in life. Investors in the sector may track whether new, simplified digital-first products can successfully convert this high-interest, low-action demographic into long-term policyholders.

What Investors Should Track

For those observing the insurance and financial services sector, the key areas to watch include the conversion rate of digital leads into policies and how companies adapt their product design to appeal to the Gen Z mindset. Additionally, any shift in how young earners balance their allocation between wealth-building assets (like mutual funds) and risk-mitigation assets (like insurance) will be a critical indicator of long-term financial health for this demographic.