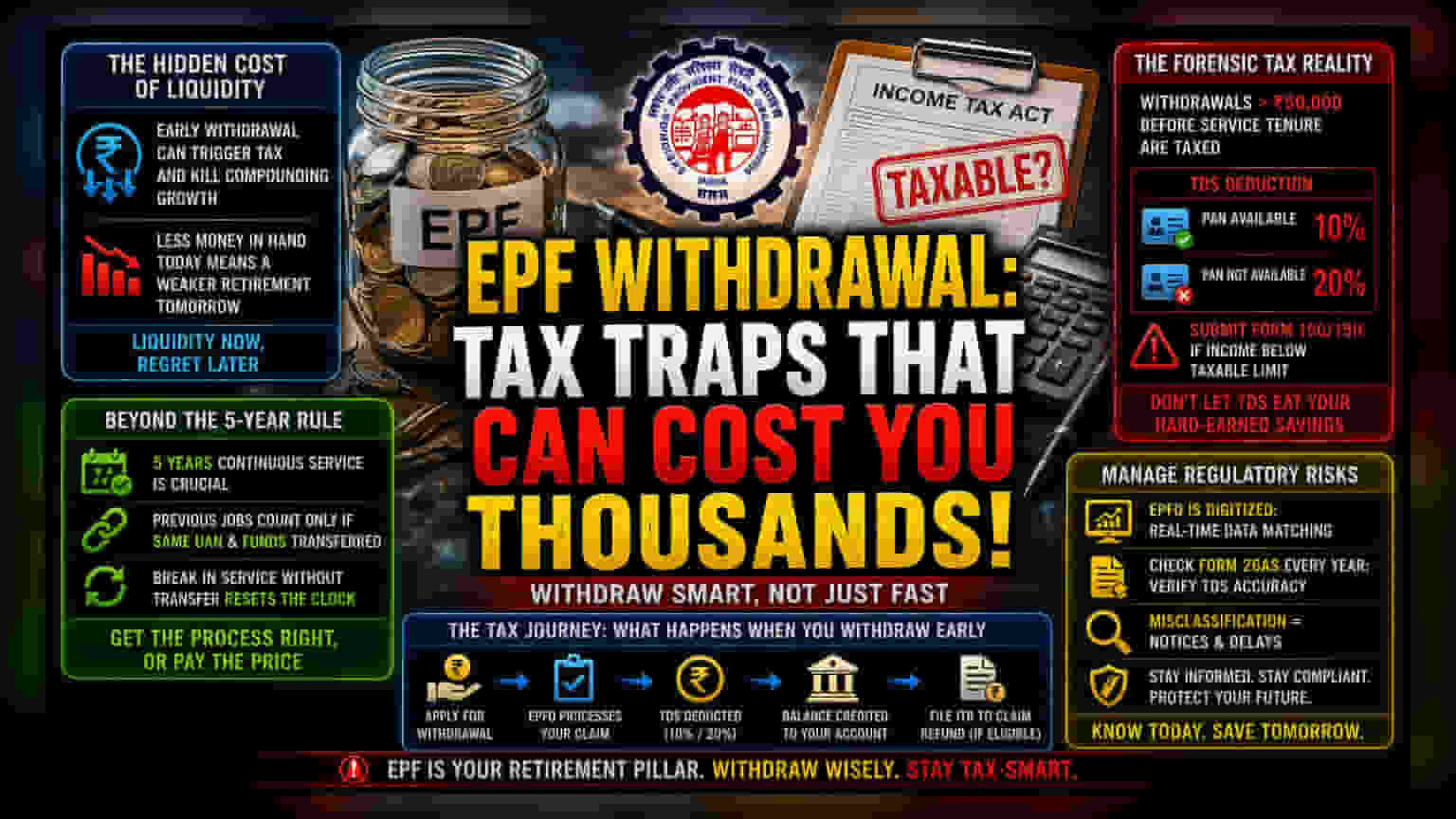

The Hidden Cost of Liquidity

While the Employees' Provident Fund serves as a bedrock for Indian retirement planning, the fiscal consequences of accessing these funds prematurely are often misunderstood. The primary danger lies not just in the loss of compounding interest, but in the immediate tax liability triggered by failing to navigate the nuances of the Income Tax Act. When an individual taps into their corpus, the distinction between capital and income becomes the primary variable in determining the final tax burden.

Beyond the Five-Year Threshold

The obsession with the five-year continuous service rule often blinds participants to deeper complexities. Even if an employee meets this tenure requirement, specific components of the accumulated balance—namely the employer’s contributions and the interest accrued thereon—remain taxable under the head of salary. Furthermore, if service is interrupted and accounts are not merged properly, the clock resets. Many individuals fail to recognize that previous employment periods only count toward the five-year mandate if the UAN remains consistent and the funds were formally transferred. Without this administrative bridge, the tax authorities view the withdrawal as premature, regardless of total years worked across different firms.

The Forensic Tax Reality

For those who withdraw more than ₹50,000 before meeting the service tenure, the tax authorities impose Tax Deducted at Source (TDS) with surgical precision. If a PAN is on record, a 10% deduction applies. If the PAN is missing, that rate doubles to 20%. The critical oversight for many employees is failing to submit Form 15G or 15H when their total income falls below the taxable threshold. These forms are not merely optional paperwork; they are the primary mechanism for preventing the unnecessary erosion of capital. When TDS is erroneously deducted, recovering those funds through the annual tax filing process creates a liquidity gap that can disrupt short-term financial planning.

Managing Regulatory Risks

Retirement planning in India now requires an active management approach rather than a passive 'set and forget' strategy. Given the digitisation of the EPFO portal, the integration of Aadhaar and UAN data provides tax authorities with real-time visibility into withdrawal patterns. This increased transparency means that manual errors in tax classification are easily flagged. Employees should treat their annual Form 26AS as a critical audit document, cross-referencing it against their withdrawal records to ensure that the TDS status matches their actual tax liability. Relying on outdated assumptions about the tax-exempt status of EPF will likely lead to unpleasant surprises during the assessment year.