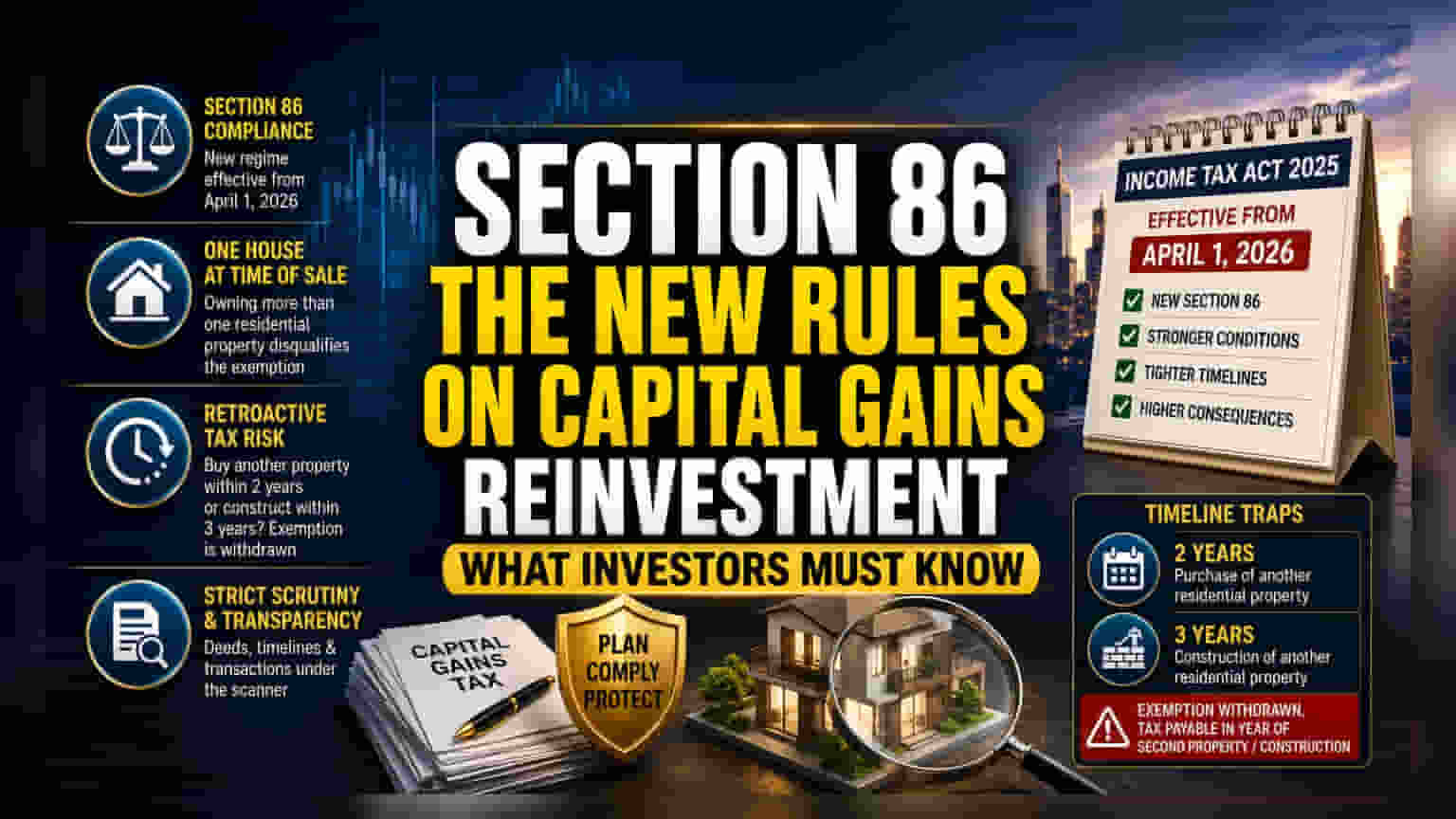

The Shift to Section 86 Compliance

With the implementation of the Income Tax Act 2025 effective April 1, 2026, the regulatory framework governing capital gains reinvestment has undergone a structural pivot. What was previously recognized under the legacy Section 54F umbrella is now codified under Section 86. This change is not merely cosmetic; it signals a stricter enforcement of tax neutrality regarding residential real estate accumulation. Investors utilizing these provisions to mitigate tax burdens on long-term share sales must now account for more rigorous scrutiny of their property portfolios at the precise moment of asset liquidation.

Eligibility and Property Ownership Constraints

The fundamental premise of the new provision rests on the limitation of residential footprint. At the exact date of the capital asset sale, the taxpayer’s ownership profile is audited. Any holding exceeding a single residential unit renders the capital gains ineligible for the reinvestment exemption. This serves as a legislative deterrent against serial property speculation disguised as primary home acquisition. By tying the exemption to the taxpayer’s status on the date of sale, the tax authorities have effectively eliminated loopholes previously exploited by those maintaining secondary rental portfolios while claiming primary residence benefits.

The Mechanics of Retroactive Taxation

Risk management under Section 86 requires precise adherence to post-investment timelines. The statute imposes a clawback mechanism that triggers if an investor acquires an additional residential property within two years of the share sale or initiates construction of a secondary unit within three years. Should either of these conditions be met, the previously granted exemption is neutralized. The tax liability does not merely reappear; it becomes exigible in the financial year the second property is acquired, often catching investors off guard during subsequent tax filing cycles. This temporal trap necessitates that investors prioritize long-term residential holdings over rapid expansion strategies to avoid sudden cash flow disruptions from retroactive tax assessments.

Strategic Portfolio Oversight

For high-net-worth individuals, the serial application of these benefits is not outright prohibited but is subject to independent transaction-based evaluation. If a taxpayer successfully divests from a secondary property to return to single-house status, the eligibility window for Section 86 may theoretically reset for future asset sales. However, the administrative burden of proving property divestment and timing makes this a high-risk maneuver. Institutional observers note that current regulatory trends favor transparency, meaning taxpayers attempting to cycle properties while leveraging capital gains exemptions should anticipate deeper scrutiny of property deeds and transaction timestamps to ensure compliance with the 2025 legislative intent.