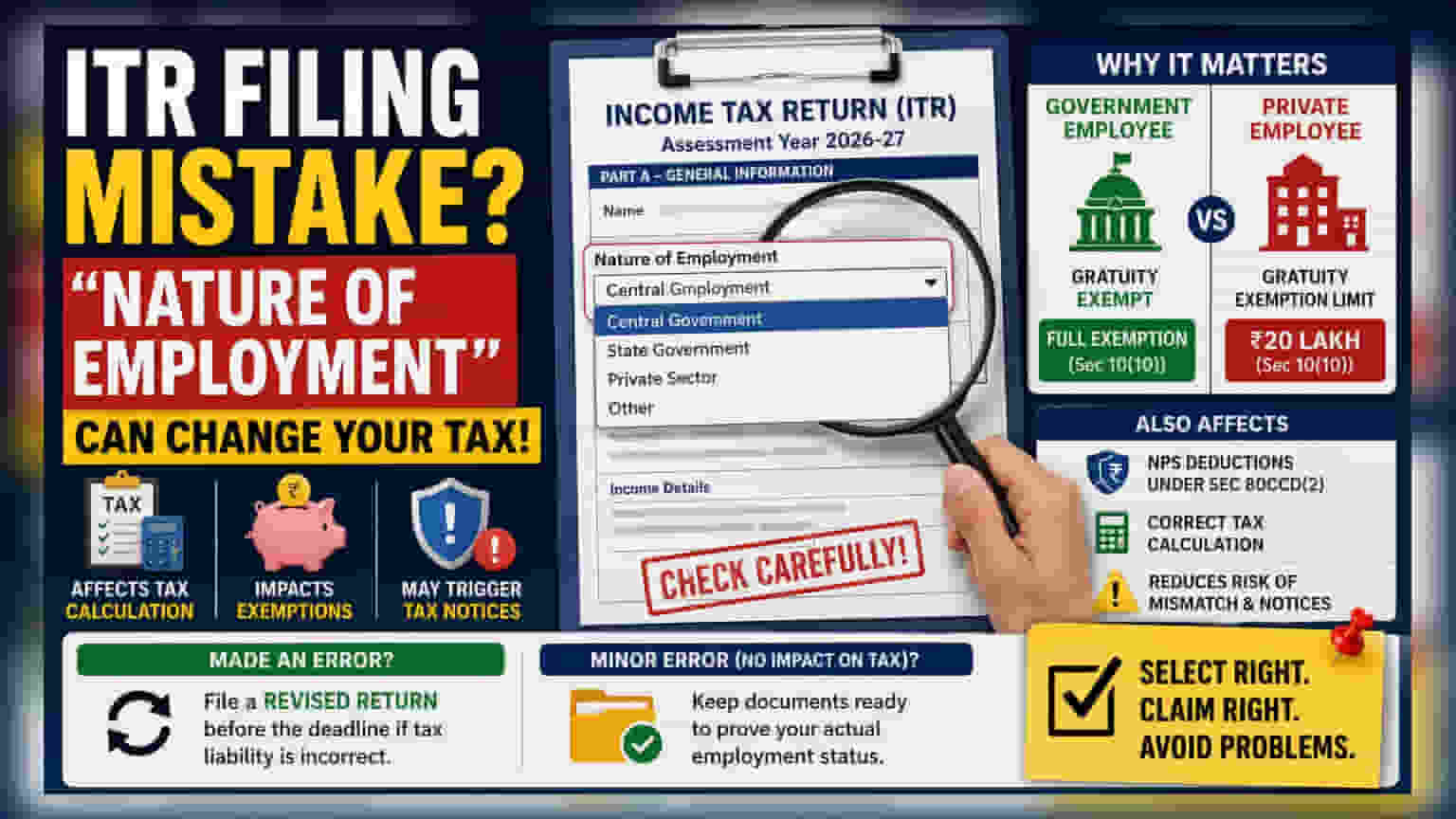

Selecting the incorrect 'Nature of Employment' in your ITR can lead to miscalculated taxes and potential notices from the Income Tax Department. This classification determines your eligibility for specific retirement exemptions like gratuity and leave encashment. If you find a mistake that alters your tax liability, filing a revised return is the standard path to correct the error.

Why 'Nature of Employment' Matters

When filing an Income Tax Return (ITR), the 'Nature of Employment' field is often treated as a simple administrative detail. However, this selection is critical for tax calculation. The Income Tax Department uses this data to automatically apply relevant rules regarding exemptions and deductions. If a taxpayer selects the wrong category—such as marking themselves as a private sector employee when they are a government employee—the tax computation software may apply incorrect exemption limits, leading to an inaccurate tax liability.

Impact on Retirement Benefits

The tax treatment of retirement benefits varies significantly between different employment categories. For instance, gratuity received by Central or State Government employees is generally fully exempt from tax under Section 10(10) of the Income-tax Act. Conversely, for employees of private companies or certain other entities, the exemption is subject to a specific monetary ceiling, currently set at ₹20 lakh. Misclassifying one’s employment status can cause a taxpayer to incorrectly claim full exemption or miss out on a legitimate deduction, both of which can invite scrutiny from tax authorities.

Deductions and NPS Rules

The classification also directly affects contributions to the National Pension System (NPS) under Section 80CCD(2). Rules for employer contributions differ based on whether the taxpayer works for the government or the private sector. By selecting an incorrect category, taxpayers risk either claiming an excessive deduction or failing to claim the amount they are entitled to. This creates a mismatch between the reported income and the tax liability, which is a common trigger for automated tax notices.

How to Correct an ITR Error

If a taxpayer realizes that an incorrect employment category was selected while filing their ITR for the assessment year 2026-27, they should first determine if the error changed their tax calculation. If the wrong classification resulted in an incorrect tax amount, the primary solution is to file a revised return before the applicable deadline. This action allows the taxpayer to correct the mistake and pay the appropriate tax, reducing the risk of further disputes. For minor clerical errors that do not affect the final tax liability, taxpayers are typically advised to maintain clear documentation proving their actual employment status to present if required by the Income Tax Department.