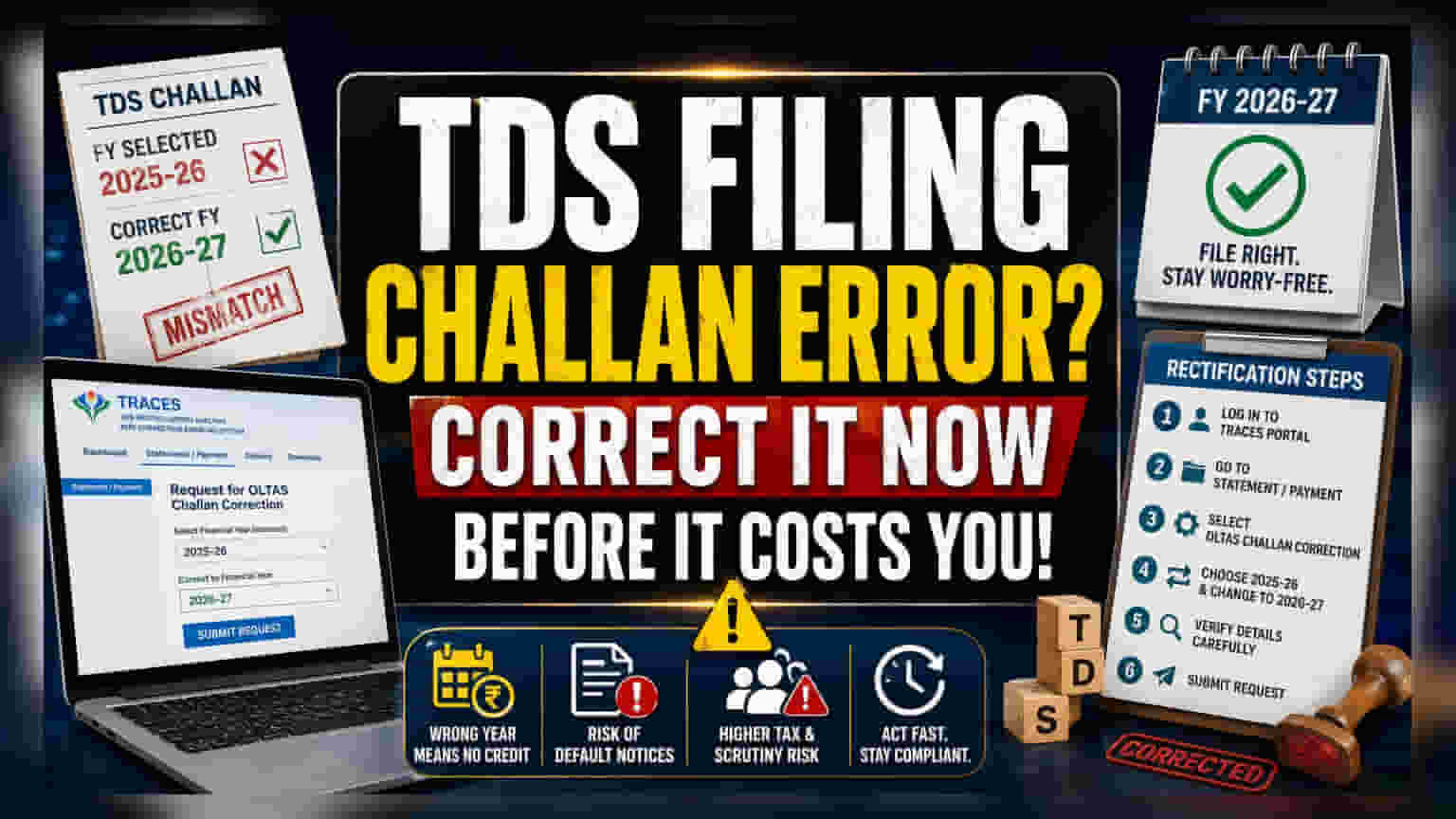

Tax deductors who mistakenly selected the wrong financial year for TDS deposits must use the legacy TRACES portal to correct them. The new Income Tax Act, 2025 portal currently does not support these specific changes. Failing to rectify these errors can result in denied tax credits and notices from the tax department.

What Happened

Tax deductors are encountering difficulties with TDS (Tax Deducted at Source) filings for the 2026-27 financial year. Some have incorrectly deposited TDS challans under the previous financial year, 2025-26, which is linked to the older Income Tax Act of 1961. The issue is that the new income tax portal, launched under the Income Tax Act, 2025, currently lacks the functionality to rectify these specific challan year mismatches. Because the system is in a transitional phase, users are being directed to the legacy TRACES portal to handle these corrections.

Why Accuracy Matters for Deductees

When a TDS challan is filed for the wrong financial year, the deductee—the individual or entity whose tax was deducted—does not receive the tax credit in their account. This mismatch can cause significant problems, including higher tax liability and potential scrutiny from the Income Tax Department. Experts indicate that these discrepancies can trigger automatic default notices, leading to unnecessary correspondence and compliance burdens for both the deductor and the deductee.

How to Fix the Challan Error

To resolve these errors, deductors are advised to log into the legacy TRACES portal. The rectification process involves navigating to the 'Statement / Payment' section and selecting the 'Request for OLTAS Challan Correction' option. Within this menu, the user must choose the incorrectly selected financial year (2025-26), change it to the correct year (2026-27), verify the details for accuracy, and submit the request. Following these steps is currently the only official way to ensure the TDS challan reflects the correct fiscal year.

What Deductors Should Monitor

Tax professionals emphasize that heightened diligence is required during this period of transition between tax regimes. Delays in correcting these errors can impede tax credit claims and complicate reporting in TDS statements. Deductors are encouraged to act promptly to ensure accurate tax filings and to avoid the risks associated with technical mismatches. Until the new system fully integrates challan correction features, the legacy platform remains the required tool for resolving these specific financial year adjustments.