Private equity and venture capital funding dropped to $17.5 billion in the first half of 2026, a 5% decline from the previous year. While total investment slowed, capital continued to flow into late-stage companies and sectors like data centers and financial services.

What Happened

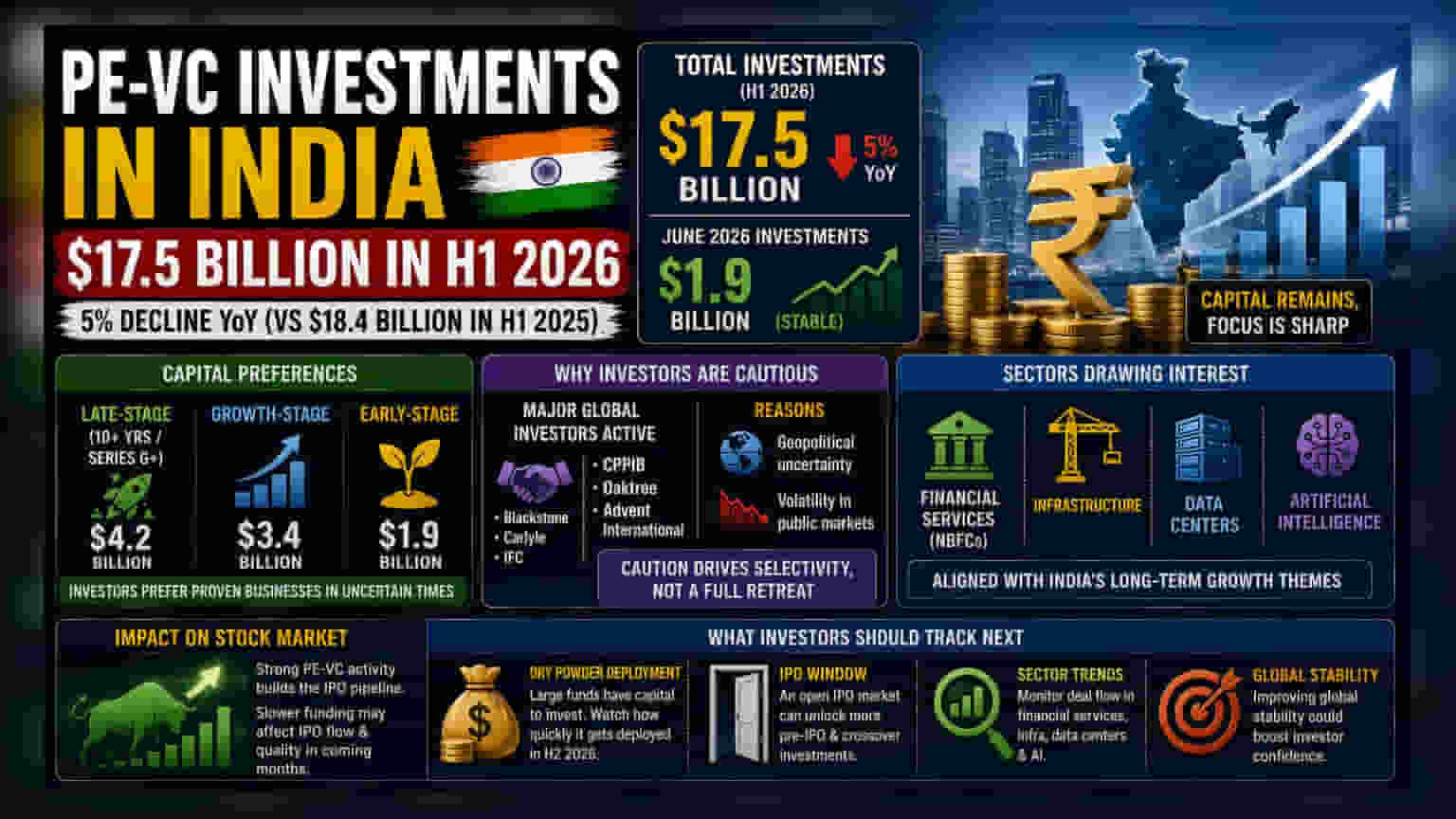

Private equity and venture capital investments in India totaled $17.5 billion during the first half of 2026. This reflects a 5% decrease compared to the $18.4 billion recorded in the same period of 2025. Data provided by the research firm Venture Intelligence highlights that the market, excluding real estate, saw a stable investment of $1.9 billion in June 2026 alone.

Where The Capital Is Going

Investors are showing a clear preference for mature businesses. Late-stage companies—those typically over 10 years old or seeking Series G or later institutional funding—attracted the largest share of capital, totaling $4.2 billion. Growth-stage companies followed with $3.4 billion, while early-stage startups secured $1.9 billion. This trend suggests that amid global volatility, investors are prioritizing businesses with established operations, proven revenue, and clearer paths to profit over high-risk early ventures.

Why Investors Are Choosing Caution

Despite the overall decline, major global investors like Blackstone, Carlyle, IFC, CPPIB, Oaktree, and Advent International remain active in the Indian market. The current caution stems from ongoing geopolitical uncertainty and volatility in public stock markets. When markets fluctuate, institutional investors often pause or reduce deal sizes to manage risk, which explains the slight dip in total deployment compared to last year.

Impact On The Stock Market

For retail investors, the level of private equity activity is often a leading indicator for the IPO (Initial Public Offering) market. A strong pipeline of PE-VC investments usually suggests that more companies will eventually seek to list on stock exchanges to provide exit opportunities for these investors. If PE-VC funding remains selective or slow, it may influence the frequency and quality of new company listings in the coming months.

Sectors Drawing Interest

While the total volume is down, capital is not drying up. There is a focused interest in specific sectors that align with India's growth themes. Financial services, particularly non-banking financial companies (NBFCs), continue to attract capital. Additionally, infrastructure, data centers, and artificial intelligence remain key focus areas. These sectors are seen as essential for long-term economic growth, which helps them maintain investor interest even when the broader funding environment is tighter.

What Investors Should Track Next

The key factor for the coming months will be the deployment of what the industry calls "dry powder." This refers to the substantial amount of money that funds have already raised from their investors but have not yet spent. Because these funds have a time limit to invest, they are under pressure to deploy this capital. Investors should track whether this capital starts flowing more freely in the second half of 2026, particularly if the IPO window opens up, as this could stimulate more pre-IPO and crossover investments.