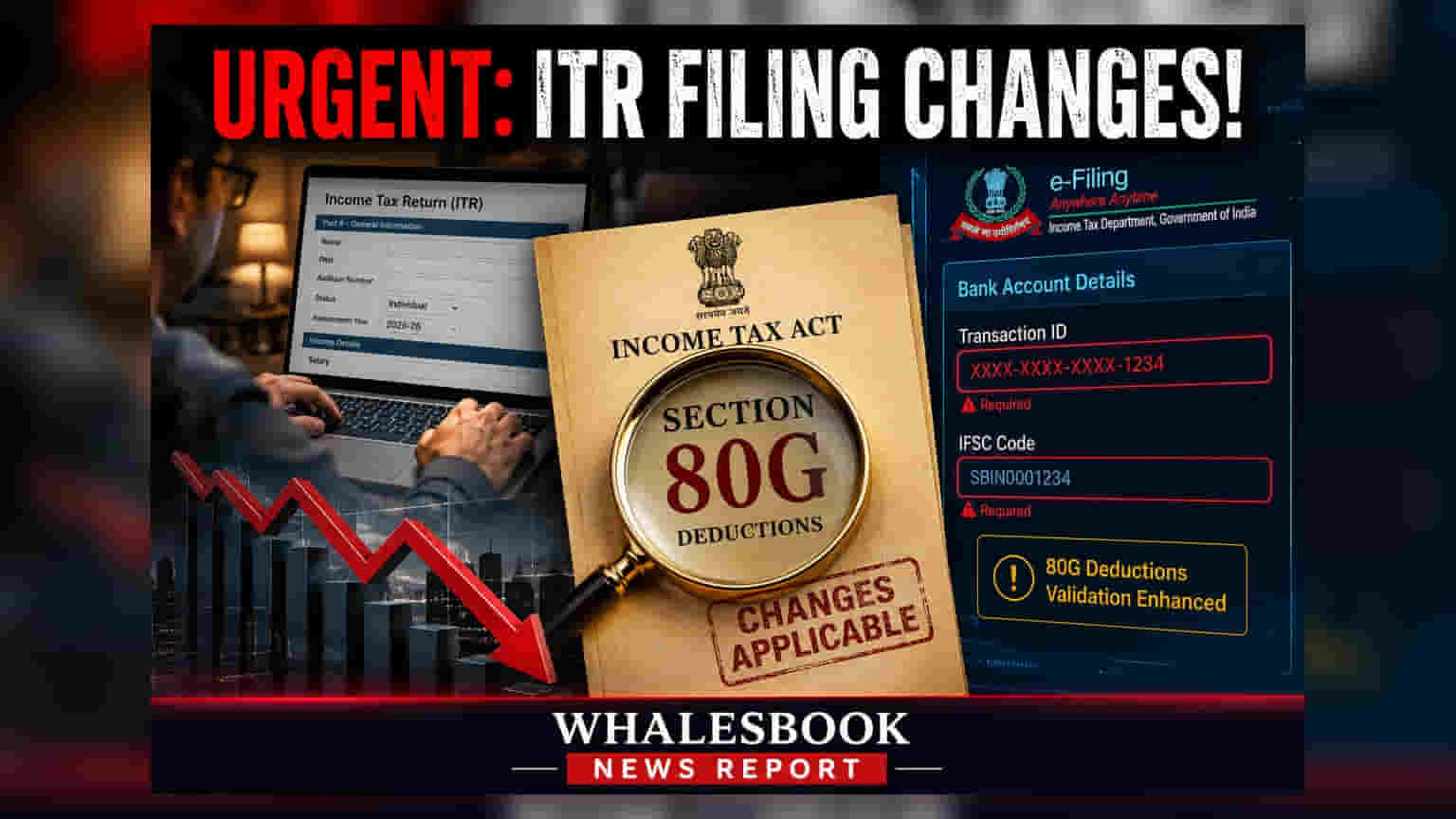

Taxpayers must now provide specific transaction details like reference numbers and IFSC codes to claim Section 80G charitable donation deductions for AY 2026-27. This change is part of an effort by the Income Tax Department to automate verification and reduce manual processing errors. Investors and taxpayers should ensure their donation receipts and bank statements match these new reporting requirements to avoid scrutiny.

The Income Tax Department has introduced stricter reporting requirements for taxpayers claiming deductions under Section 80G of the Income Tax Act for the Assessment Year 2026-27. In previous years, taxpayers only needed to declare the total donation amount to claim a tax benefit. Under the updated filing norms, claimants must now provide granular payment details, including the transaction reference number for UPI, NEFT, RTGS, IMPS, or cheque payments, alongside the IFSC code of the bank used for the transfer.

This shift is part of the tax authority's broader objective to move toward an automated, technology-driven compliance framework. By requiring a verifiable digital payment trail, the department aims to match donation claims with actual bank records automatically during the return processing phase. This reduces the reliance on manual verification and minimizes the scope for tax discrepancies.

Impact on Filing Process

The new disclosure requirements apply to the most common ITR forms used by individuals, including ITR-1, ITR-2, ITR-3, and ITR-4. Because charitable donations are not typically reflected in the Annual Information Statement (AIS) or Form 26AS—unlike salary income or TDS—the burden of proof lies entirely with the taxpayer. Consequently, taxpayers must ensure that every donation claim is backed by valid receipts and corroborated by their bank statement.

Tax experts note that this change increases the importance of maintaining accurate documentation. If the information provided in the return does not perfectly match the bank records or the receipts issued by the charitable institution, it may trigger system-generated clarification requests or lead to processing delays. In some instances, incorrect or incomplete details could lead to the disallowance of the deduction during assessment.

Practical Steps for Taxpayers

To ensure a smooth filing experience, taxpayers should organize their financial records well in advance. If specific transaction details are missing, these can typically be retrieved through internet banking portals, UPI application history, or by contacting the charitable institution for duplicate acknowledgments. It is also important to verify that the recipient organization holds a valid, active registration under Section 80G, as donations to non-approved entities are not eligible for tax benefits. For employees whose taxes are deducted at source, it is essential to cross-verify that any donations accounted for by the employer in Form 16 align with the final details entered in the ITR. Investors who frequently donate to social causes should treat these transaction records with the same level of care as their primary investment documents to avoid unnecessary tax scrutiny.