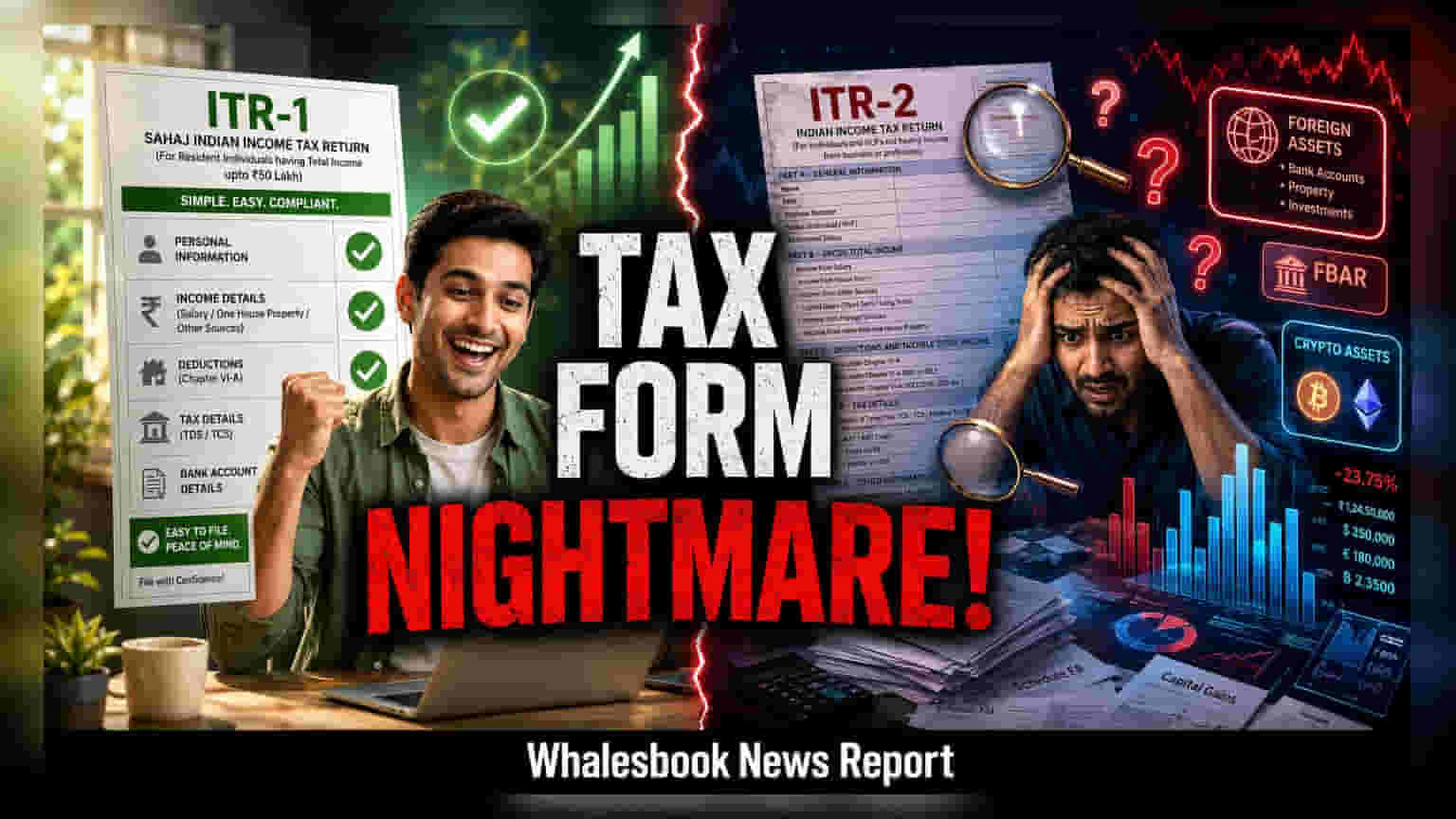

The Central Board of Direct Taxes has simplified ITR-1 to allow more retail investors to report capital gains and multiple house properties. Meanwhile, ITR-2 filers now face tougher disclosure requirements for foreign assets and virtual digital assets. These updates aim to streamline tax filing for the majority while tightening compliance for those with complex income sources.

The annual income tax return filing season, which concludes on July 31, features significant updates to filing forms for the current assessment year. The Central Board of Direct Taxes (CBDT) has focused on reducing the compliance burden for the majority of taxpayers while simultaneously increasing the detail required for more complex financial profiles.

ITR-1 Changes Benefit Retail Investors

Form ITR-1, also known as Sahaj, is the most common tax form in India, used by more than 5.25 crore taxpayers. The latest changes make this form more inclusive. Salaried individuals who earn long-term capital gains of up to ₹1.25 lakh from listed stocks can now use ITR-1. Previously, even small gains from stock market investments often required filing the more complex ITR-2. Additionally, the limit for reporting income from house properties has been increased, allowing taxpayers with up to two properties to use the simpler form. These adjustments are designed to help retail investors complete their filings more efficiently.

Efficiency Through Automated Data

To further assist taxpayers, the income tax portal has improved its pre-filling capabilities. Information regarding salary, bank interest, dividends, and capital gains reported by brokers now automatically populates in the forms using data from Form 26AS, the Annual Information Statement (AIS), and the Taxpayer Information Summary (TIS). This automation limits the need for manual data entry. Additionally, the department has introduced a 'discard return' option for Assessment Year 2024 and onwards. This allows taxpayers to delete a submitted return and file a fresh one if they discover an error before verification, which is faster than the traditional process of filing a revised return. Refund timelines have also improved, with ITR-1 filers now typically seeing refunds processed in under three weeks after e-verification.

Increased Reporting for ITR-2

While ITR-1 has been streamlined, ITR-2 has become more rigorous for taxpayers with complex income. The disclosure requirements for foreign assets, covered under Schedule FA, are now broader and include details on offshore mutual funds, foreign bank accounts, and grants from overseas parent companies. Failure to report these correctly can attract penalties under the Black Money Act.

Similarly, the reporting of Virtual Digital Assets (VDA) under Schedule VDA now requires line-by-line details of every transaction. Crypto gains remain taxed at a flat 30%, with no ability to offset losses against other forms of income or carry them forward. Furthermore, the asset and liability declaration in Schedule AL, which is mandatory for individuals with income over ₹50 lakh, is capturing more taxpayers as income levels rise. Individuals holding overseas retirement accounts must now opt for ITR-2 rather than ITR-1, reflecting the tax department’s focus on detailed international tax compliance. Investors should ensure their records match AIS data to avoid mismatch notices from the tax department.