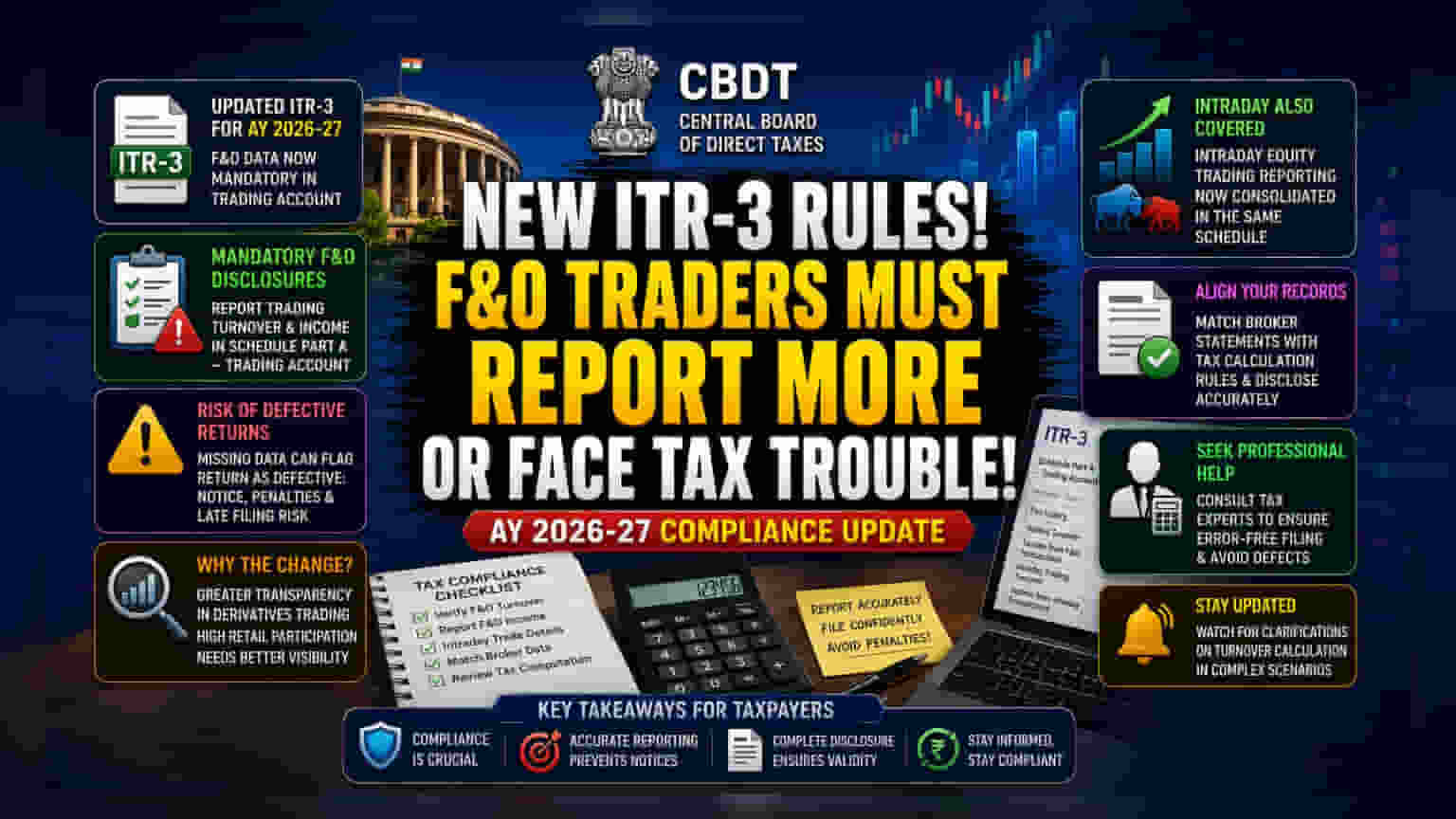

Taxpayers filing ITR-3 for Assessment Year 2026-27 now face stricter disclosure requirements for Futures & Options (F&O) trading. The Income Tax Department mandates specific reporting of F&O turnover and income in the 'Trading Account' schedule. Missing these details may result in returns being marked as defective, leading to potential penalties. This change aims to enhance data transparency regarding derivative trading activity.

What Happened

The Central Board of Direct Taxes (CBDT) has introduced updated reporting requirements for taxpayers filing ITR-3 for the Assessment Year 2026-27. Individuals and Hindu Undivided Families (HUFs) who engaged in Futures & Options (F&O) trading during the 2025-26 financial year must now provide specific, granular data. The updated ITR-3 form requires the reporting of both trading turnover and income derived from F&O transactions directly within the 'Schedule Part A – Trading Account' section. This is a shift from previous filing formats where such granular breakdown may not have been explicitly required in the same manner.

Why This Matters For Investors

For traders, the primary risk is compliance. The Income Tax Department has indicated that if these new fields are left blank or the data is missing, the submitted tax return could be flagged as defective. When a return is classified as defective, the tax department issues a notice, and the taxpayer must rectify the error within a specified timeframe. If the taxpayer fails to rectify the defect, the return may be treated as invalid, which is equivalent to not filing a return at all, exposing the taxpayer to potential penalties and late filing consequences.

The Bigger Context Behind The Change

The move aligns with a broader push for increased transparency in the Indian derivatives market. Participation in the F&O segment has surged in recent years, and market regulator SEBI has consistently highlighted, through various studies, that a significant portion of retail derivative traders incur financial losses. By mandating more detailed disclosures, the Income Tax Department can gain better visibility into derivative trading activities and improve the cross-verification of reported income against the data shared by brokers and exchanges.

Reporting Intraday Transactions

The revised filing requirements are not limited to F&O traders. The update also consolidates the reporting of intraday equity trading within the same 'Trading Account' schedule. This means that both F&O traders and those engaged in speculative intraday equity trading must now provide consistent, detailed reporting in the same section of the form. The goal is to standardize how business-related trading income is reported, regardless of the instrument used.

What Investors Should Track

Taxpayers filing ITR-3 should ensure their financial records, particularly their tax computation statements provided by brokers, align with the new disclosure requirements. It is essential to double-check that the turnover figures—calculated according to tax guidelines—are accurately reflected in the 'Trading Account' schedule of the ITR-3 form. Given the technical nature of these disclosures, many taxpayers may find it beneficial to consult with a chartered accountant or tax professional to ensure the data is captured correctly, preventing any issues with defective returns. Investors should monitor for any further clarifications from the Income Tax Department regarding the calculation of turnover in specific complex trading scenarios.