The Income Tax Department has launched Form 168, which combines data from Form 26AS and the Annual Information Statement (AIS). This new form will become the standard starting in the 2026-27 tax year. For current filings related to the 2025-26 financial year, taxpayers must continue using the existing Form 26AS.

The Income Tax Department has introduced a new reporting document, Form 168, to its e-filing portal. This change is part of the updated Income Tax Act of 2025 and is designed to simplify how taxpayers view their financial and tax information. Understanding the timeline for this transition is important for all taxpayers to avoid confusion during the upcoming tax filing seasons.

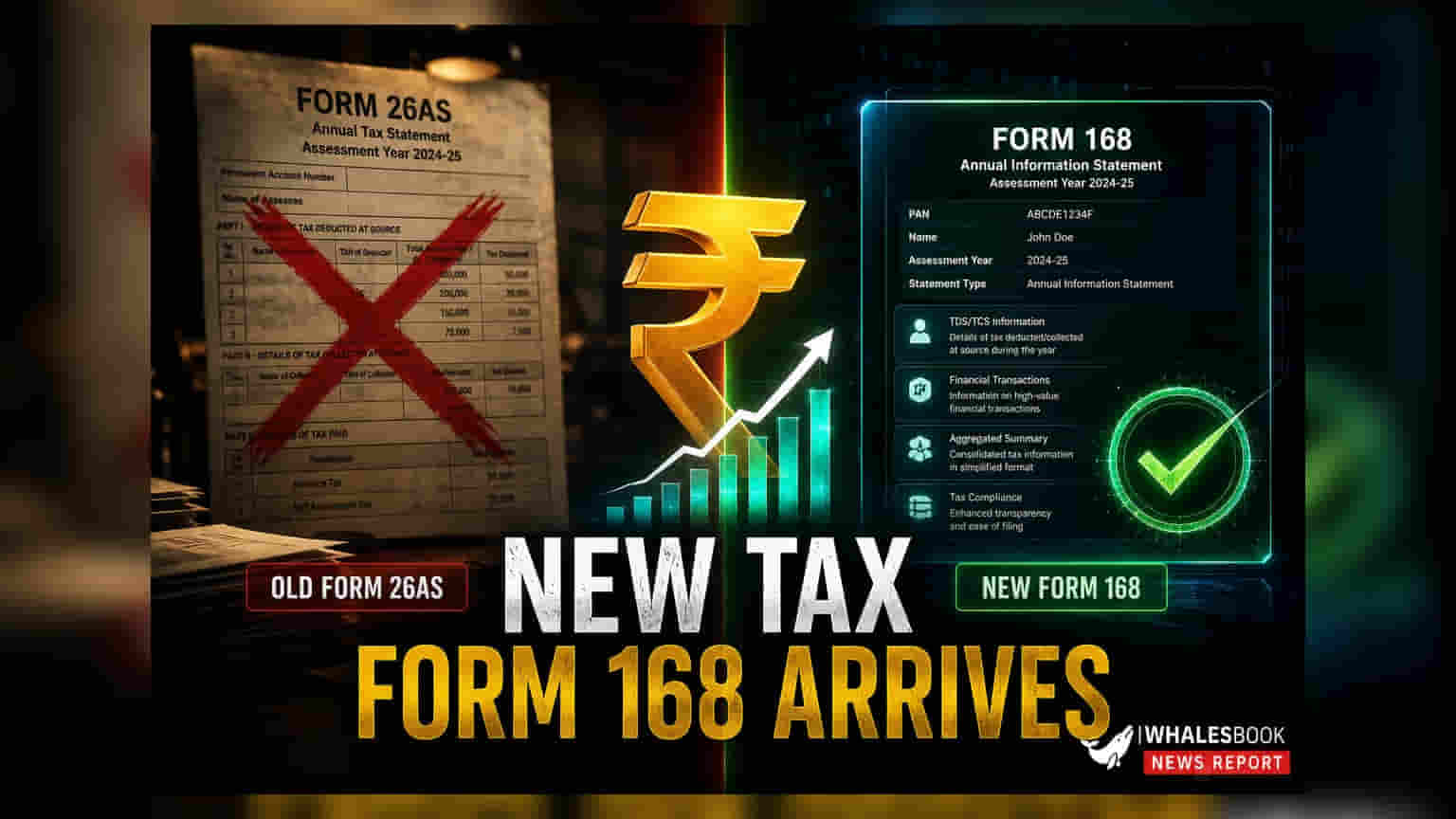

Form 168 Versus Form 26AS

For the current filing period, which covers the financial year 2025-26, taxpayers are required to stick with the established Form 26AS. The new Form 168 is specifically designated for the 2026-27 tax year onwards. While Form 26AS has traditionally provided a record of taxes deducted at source and tax credits, the new Form 168 acts as a unified document. It integrates data points that were previously spread across Form 26AS and the Annual Information Statement (AIS). By consolidating this information, the department aims to create a more efficient reconciliation tool for individual taxpayers.

What Changes for Taxpayers

The primary objective of Form 168 is to provide a single, comprehensive view of a taxpayer’s financial activity. This includes details such as taxes paid, government demands, pending refunds, and financial information reported by third parties like banks, employers, and investment institutions. Because the new form acts as a consolidated record, it reduces the need for taxpayers to track multiple documents when preparing their income tax returns. Tax experts suggest that this change will enhance transparency and make it easier for individuals to identify any mismatches in their reported income or tax payments early in the process.

Importance of Data Reconciliation

Regardless of which form is active, the core responsibility of the taxpayer remains the same: ensuring that all reported financial data is accurate. Tax professionals emphasize that taxpayers should cross-verify their salary statements, interest income from banks, TDS certificates like Form 16, and investment transactions against the data provided by the tax portal. Proactive reconciliation is essential to prevent common issues such as refund delays or receiving unexpected notices from tax authorities due to reporting errors. As the system transitions to Form 168 in the coming year, the focus for investors and taxpayers should remain on maintaining clean financial records throughout the year rather than waiting until the final filing deadline. Investors should look out for further updates on the e-filing portal regarding the specific layout and accessibility of Form 168 as the 2026-27 tax cycle approaches.