High sales growth does not always mean a company is healthy. Sometimes, companies use accounting tricks to make their revenue look better than it is. Understanding common red flags—like rising sales without cash or channel stuffing—can help investors distinguish between real growth and accounting illusions.

The Gap Between Sales and Cash

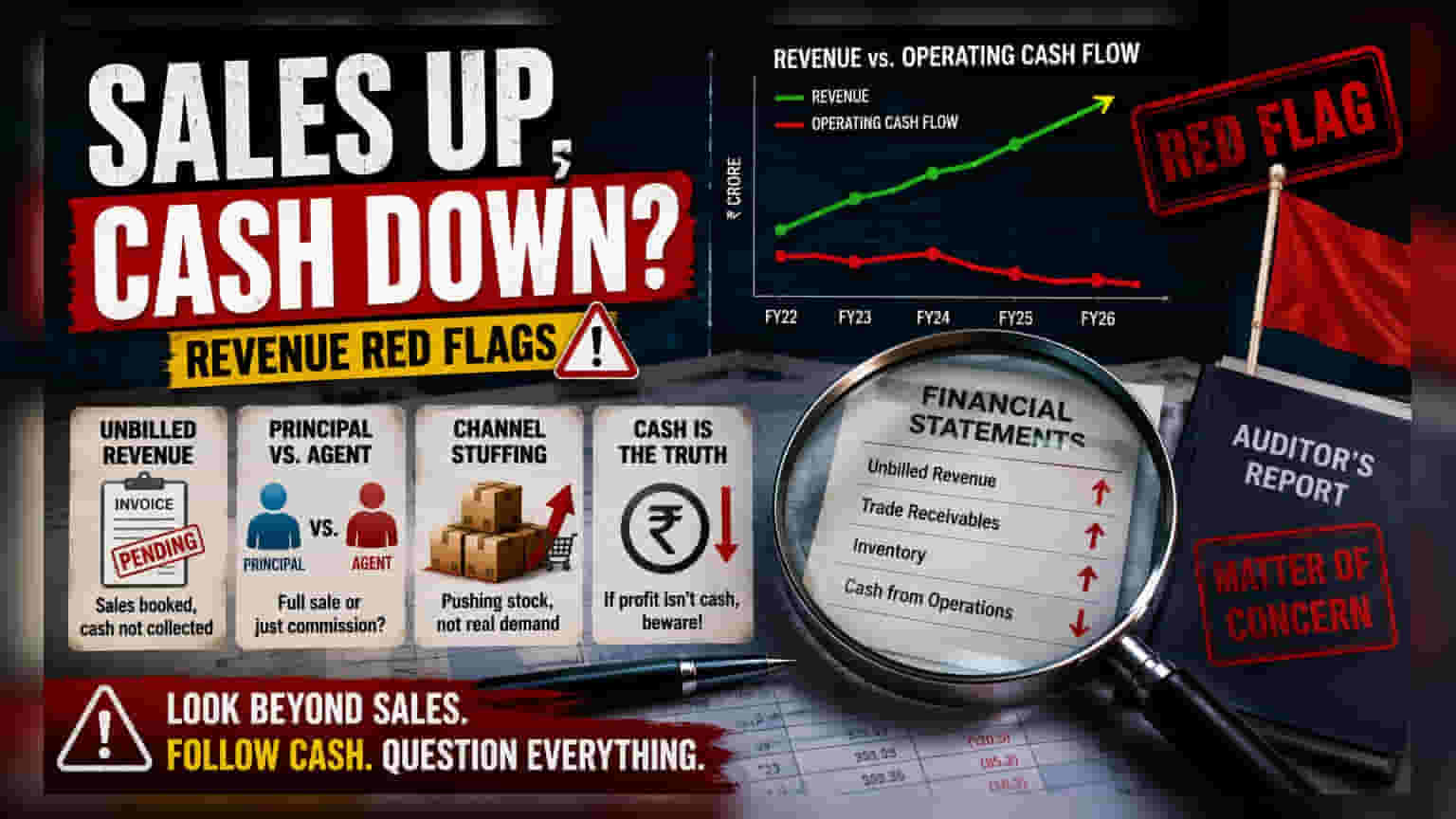

When a company reports strong sales growth, it is usually viewed as a positive sign. However, seasoned investors know that all revenue is not created equal. There is a critical difference between booking a sale on paper and actually collecting cash from the customer. A major warning sign for any investor is a company that consistently reports high revenue growth while its operating cash flow remains stagnant or negative. If the reported profit does not turn into cash, the company may be struggling with its collections, or worse, booking revenue that may never materialize.

The 'Unbilled Revenue' Trap

One common accounting tactic to watch involves 'unbilled revenue.' This occurs when a company recognizes a sale for work performed but has not yet sent an invoice or received customer certification. While this is sometimes standard in long-term construction or IT projects, a persistent increase in unbilled revenue often warrants closer inspection. If this figure keeps growing on the balance sheet, it suggests the company is booking sales for which it cannot yet collect money. Investors should check if the pace of unbilled revenue growth is significantly faster than the overall revenue growth.

Principal vs. Agent Accounting

Investors should also be careful with how a company classifies its revenue, especially in trading, logistics, or online marketplace businesses. A 'principal' controls the goods or services and records the full sale value as revenue. An 'agent,' however, merely facilitates the transaction and should record only their commission or service fee. Some companies may attempt to inflate their top-line figures by booking the full transaction value as revenue instead of just the commission. This can make the company appear much larger than its actual economic footprint.

The Danger of Channel Stuffing

Channel stuffing is a technique used to artificially inflate sales figures at the end of a quarter or financial year. It happens when a company pushes excess inventory onto its distributors or dealers, often with the promise that they can return the unsold goods later. This boosts the company’s reported sales for the current period, even if the end-consumer demand is not there. If a company shows a sudden spike in revenue near the quarter-end or if inventory levels at the dealer level are rising, it may be a sign of channel stuffing.

What Investors Should Track

Beyond the headline sales number, investors should spend time reading the notes to the financial statements in the annual report. Look for disclosures regarding revenue recognition policies, details on dealer arrangements, and the aging of trade receivables. A rapid increase in receivables, especially those that are overdue, often indicates that customers are not paying on time. Finally, pay attention to the auditor’s report. If an auditor flags concerns about revenue recognition or related-party transactions, or if there is a sudden change in auditors after such a dispute, it is a significant red flag that requires a deeper investigation.