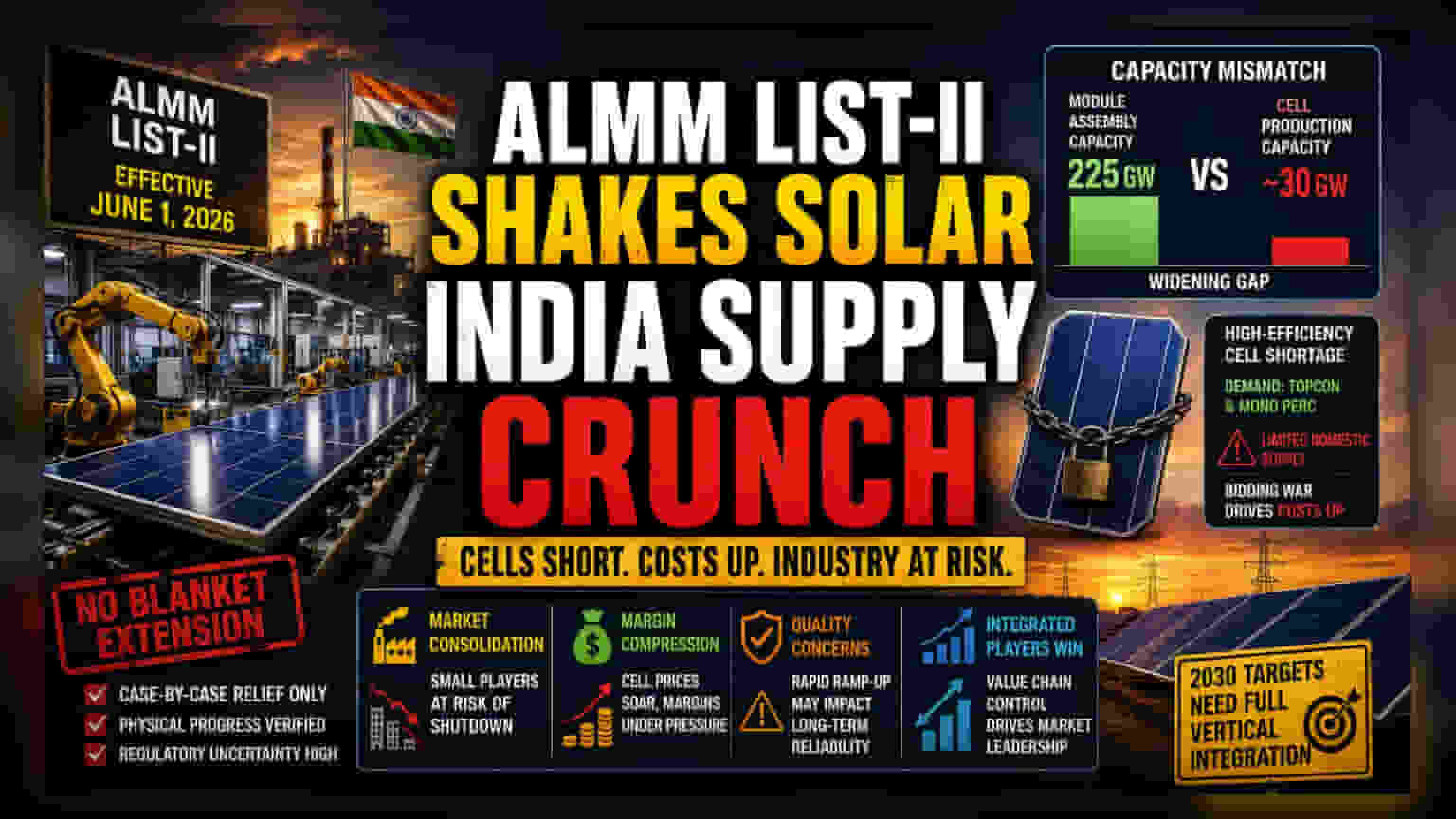

The Mismatch Catalyst

The implementation of the Approved List of Models and Manufacturers (ALMM) List-II on June 1, 2026, was designed as a definitive lever to drive domestic self-sufficiency. However, the mandate has immediately triggered a severe structural friction point. The domestic solar industry currently boasts an impressive 225 GW of module assembly capacity, yet it is throttled by a critically underdeveloped upstream: domestic solar cell production capacity languishes at approximately 30 GW. This fundamental mathematical mismatch effectively forces the domestic industry to pivot from an import-dependent model to a supply-constrained one overnight.

The Technological Bottleneck

Beyond mere volume, the crisis is defined by technology type. The current surge in utility-scale and commercial projects is heavily weighted toward high-efficiency TOPCon (Tunnel Oxide Passivated Contact) and monocrystalline cells. Data indicates that while module manufacturers have built massive assembly lines, the domestic supply of high-efficiency cells—the precise components required for these modern installations—is far thinner than the headline capacity figures suggest. Developers attempting to comply with the new local sourcing requirements find themselves in a bidding war for a limited pool of domestic high-efficiency cells. This not only inflates procurement costs but also threatens to strand projects where design specifications rely on specific imported technologies that no longer meet the regulatory bar.

The Structural Consolidation Risk

This policy environment acts as a massive accelerator for market consolidation. Smaller, non-integrated module manufacturers who lack in-house cell production capabilities are at a severe competitive disadvantage. Without the luxury of controlling their own upstream supply, these firms are now subject to the margin-crushing pricing of the few large-scale, vertically integrated players that do possess domestic cell manufacturing facilities. Expect to see a wave of distressed asset sales or operational shutdowns among smaller players who cannot bridge the gap between their expensive, high-capacity assembly plants and their inability to secure reliable, domestically manufactured cells at scale.

The Forensic Bear Case

The regulatory reality is that the Ministry of New and Renewable Energy (MNRE) has denied a blanket extension, offering only case-by-case, conditional relief for projects where significant physical progress was documented. This creates an environment of regulatory uncertainty. For investors, this signals elevated execution risk. Projects that failed to secure sufficient inventory or contractual commitments prior to the June 1 cutoff are now at the mercy of bureaucratic scrutiny and supply-chain volatility. Furthermore, the reliance on nascent domestic cell production poses a distinct quality-control risk; if the initial ramp-up in domestic cell manufacturing is rushed to meet the mandate, the industry may face systemic issues regarding long-term panel performance, potentially leading to increased warranty costs and asset underperformance over the next 24 months.

The Forward Trajectory

The path toward 2030 targets necessitates a rapid transition to full vertical integration. The current supply crunch is not merely a short-term headache but a predictable outcome of subsidizing downstream assembly without simultaneously anchoring the upstream supply chain. While this policy will ultimately serve to mature the domestic ecosystem, the interim period will be characterized by margin compression for pure-play module makers and a shift in market share toward integrated energy conglomerates that can successfully manage the entire value chain from polysilicon to finished panel.