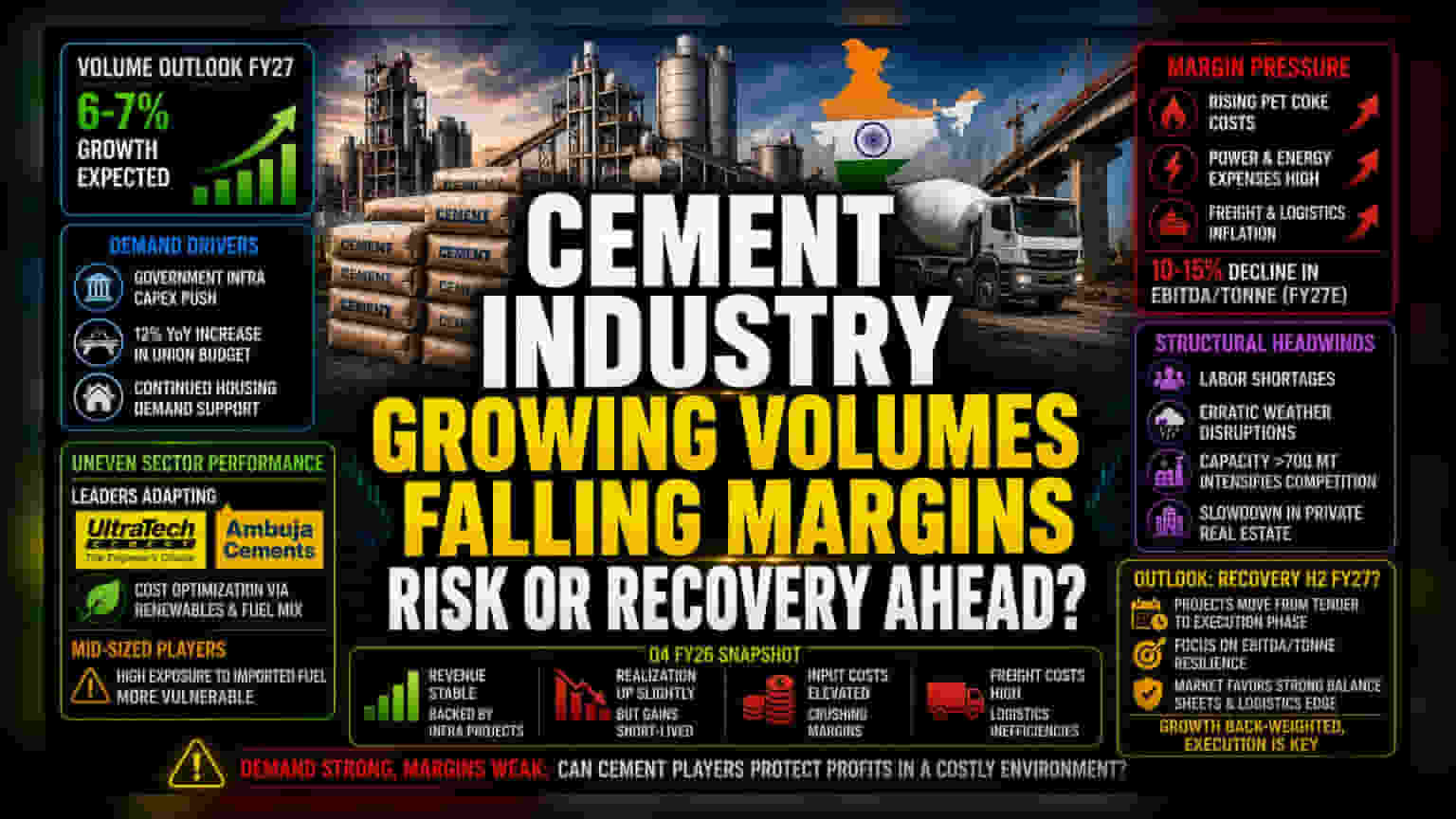

The Valuation Gap Between Volume and Earnings

The Indian cement industry is currently navigating a period of sharp divergence where robust demand signals are being undermined by operational cost pressures. While industry analysts forecast a volume expansion of 6-7% for FY27, the market is increasingly focused on the diminishing returns per tonne. Aggregate performance metrics from the most recent quarter show that while total revenue remains anchored by government-backed infrastructure projects, the industry's ability to translate this into sustained profit growth is flagging. The core issue lies in a pricing model that is failing to keep pace with an aggressive rise in input costs, particularly for pet coke and power, which have been exacerbated by geopolitical instability in West Asia.

Sectoral Divergence and Operational Hurdles

Performance across the sector is proving uneven. Industry leaders, including UltraTech Cement and Ambuja Cements, have attempted to optimize their cost structures through increased use of renewable energy and fuel-mix adjustments. Conversely, mid-sized producers and those with higher exposure to imported fuel face a more precarious path. Despite total infrastructure capital expenditure—bolstered by a 12% year-on-year increase in the recent Union Budget—stimulating consistent demand, the industry is struggling with immediate domestic operational headwinds. Labor shortages and erratic weather patterns have already contributed to a temporary deceleration in growth for the current quarter. While realization levels saw minor improvements in Q4 FY26, these gains are being rapidly eroded by elevated freight expenses and logistics inefficiencies.

The Forensic Bear Case

From a risk-averse perspective, the industry is essentially running faster just to stand still. Investors must account for the reality that the massive capacity additions executed over the past two years are now intensifying competitive pressure. With industry capacity having crossed 700 million tonnes per annum, producers lack the pricing power to fully pass on inflationary costs to the end consumer. Furthermore, the margin compression is not merely a theoretical risk; leading rating agencies have already projected a 10-15% decline in operating profitability per tonne for the fiscal year. Any prolonged disruption to shipping routes or a sustained surge in global crude oil prices would likely trigger further earnings downgrades. The sector is also vulnerable to a potential slowdown in private residential real estate, which serves as a critical secondary demand driver that has shown signs of softening in recent months.

The Future Outlook

Looking ahead, the recovery trajectory is heavily back-weighted. Expectations for healthy growth are anchored entirely to the second half of FY27, as government-funded projects transition from the tendering phase to active construction. While brokerage consensus remains cautiously optimistic, the focus has shifted toward companies that can successfully manage their EBITDA per tonne through the cycle. The market will likely continue to punish players unable to maintain margins, prioritizing those with strong balance sheets and diversified logistics capabilities over those purely focused on aggressive capacity accumulation.