The Income Tax Department has identified approximately 20,000 cases where taxpayers may have claimed ineligible deductions or exemptions. The department is using data analytics to spot discrepancies in claims between Rs 50,000 and Rs 1 lakh. Taxpayers are advised to review their filings voluntarily to avoid future penalties, interest charges, and intense tax scrutiny.

What Happened

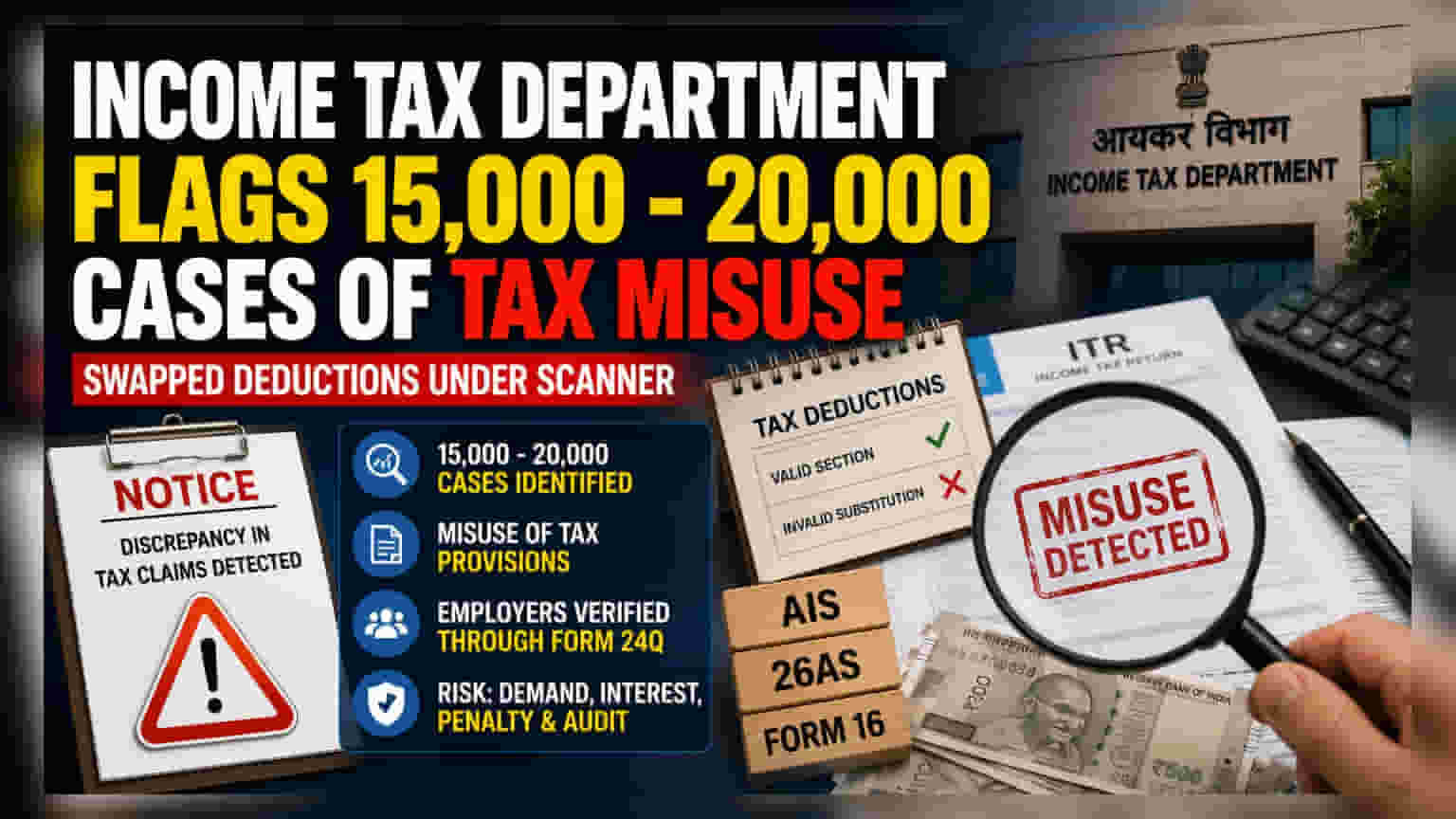

The Income Tax Department has flagged between 15,000 and 20,000 cases involving the misuse of tax provisions. The authority is focusing on instances where taxpayers allegedly "swapped" or substituted tax deductions without actually meeting the required conditions. This practice often involves claiming a tax break under a section for which the taxpayer is not eligible, in an attempt to lower their taxable income artificially.

The department is using advanced data analytics to identify these suspicious claims, specifically focusing on discrepancies in the range of Rs 50,000 to Rs 1 lakh. In addition to notifying individual taxpayers, the department has also reached out to employers to review salary-related tax filings, specifically Form 24Q, to ensure the Tax Deducted at Source (TDS) matches the claims made by employees.

Understanding the Risk

While the term "swapped provisions" is not a technical legal definition, it describes a common error where individuals try to swap an invalid exemption for a valid one without proper documentation. Tax authorities are now cross-verifying these claims against the Annual Information Statement (AIS), Form 26AS, and employer-provided data.

Because the department now has access to high-quality data from multiple sources, it is much harder for taxpayers to hide inconsistencies. The risk for those who ignore these discrepancies is significant. It can lead to formal tax demands, additional interest charges for late payments, financial penalties, and even the start of rigorous scrutiny or audit proceedings by the tax office.

How to Fix Your Filing

Taxpayers who receive a notice or suspect they may have made an error in their filed Income Tax Return (ITR) should act quickly. The first step is to perform a detailed reconciliation. Compare your ITR data against your actual salary slips, Form 16, the Annual Information Statement, and your bank statements to check for errors.

If the window for filing a revised return is still open, it is generally recommended to file a corrected return rather than waiting for further action from the authorities. If the tax return has already been processed and a notice has been received, taxpayers should respond within the given timeframe. Providing accurate documentation and paying the correct tax along with interest is the most effective way to resolve these issues and avoid further complications.

What to Monitor Next

The key for taxpayers is compliance and documentation. Since the department is using technology to automate the detection of errors, taxpayers should ensure that all claims made in their ITR are backed by genuine proof of payment or investment. Investors and employees should prioritize transparency in their filings to ensure they do not become the subject of future departmental investigations.