With the July 31, 2026 deadline approaching, taxpayers must ensure accurate income reporting to avoid notices or refund delays. Key steps include reconciling data with AIS and Form 26AS, selecting the correct ITR form, and verifying all income sources.

As the July 31, 2026 deadline for filing income tax returns for the financial year 2025-26 nears, taxpayers are reminded that filing is a critical financial reconciliation process. While digital tools like pre-filled forms have simplified the task, the final responsibility for accuracy lies with the individual. Errors in filing can lead to processing delays, unwanted tax notices, and potential penalties from the Income Tax Department.

Form Selection and Tax Regime Choices

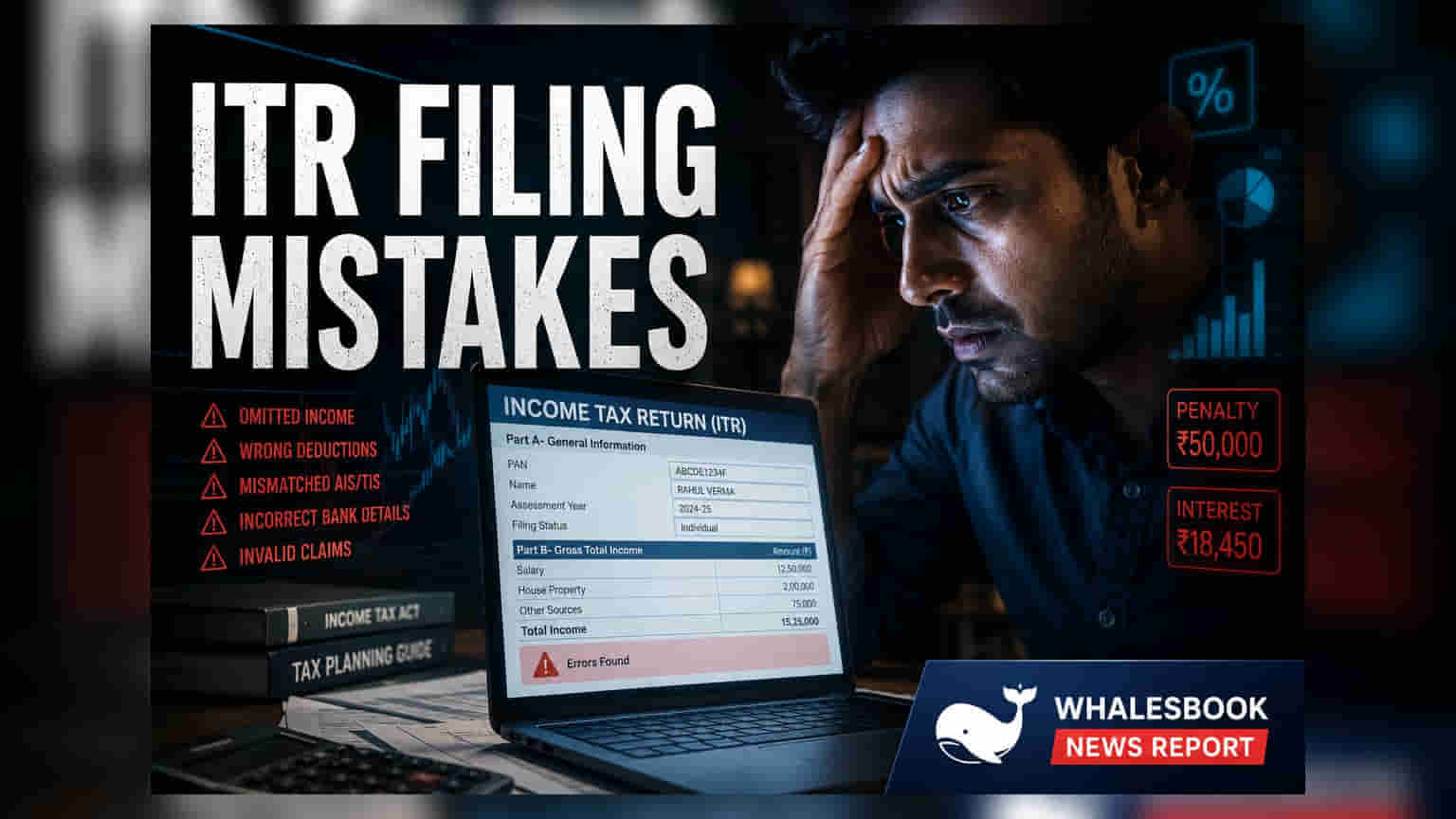

One of the most frequent errors is selecting the wrong ITR form. For instance, while ITR-1 is commonly used for basic salary and interest income, individuals with complex financial profiles—such as those earning over Rs 50 lakh or reporting capital gains from stocks, mutual funds, or property—must use ITR-2 or other appropriate forms. Furthermore, taxpayers must carefully calculate their tax liability under both the old and new tax regimes. The choice of regime can significantly impact the final tax outgo, and once a selection is made for the year, changing it later is often not possible.

Data Reconciliation and Verification

Taxpayers should not rely exclusively on pre-filled data. It is essential to reconcile personal income and tax deduction records against the Annual Information Statement (AIS) and Form 26AS. These documents provide a comprehensive view of financial transactions reported by banks, employers, and investment firms. Any mismatch between these official statements and the details provided in the return is a primary trigger for scrutiny by the tax department. Additionally, verifying that PAN, Aadhaar, and bank account details are correctly linked and updated is vital for ensuring that tax refunds are processed without unnecessary hurdles.

Comprehensive Disclosure Requirements

Accurate disclosure is mandatory for all income streams. Beyond regular salary, taxpayers must account for interest income, rental income, dividends, and freelance earnings. A common oversight involves failing to report capital gains from financial market transactions. For investors, disclosing profit or loss from equity and debt funds is necessary to remain compliant. Similarly, resident taxpayers with foreign assets or income must disclose these in the relevant schedules to avoid severe penalties. It is equally important to only claim deductions for which supporting documentation is readily available, as unsubstantiated claims are frequently flagged during audit processes.

Final Compliance Steps

The filing process is not complete until the return is verified. Taxpayers can complete the process by e-verifying their return using Aadhaar OTP or net banking, or by submitting the physical ITR-V to the Centralized Processing Centre within the stipulated time. Missing this step renders the filing incomplete, potentially treating the return as unfiled and attracting late fees.