The Income Tax Department has released the ITR-3 utility for the 2026-27 assessment year. This form is essential for individuals and HUFs with business or professional income. The update includes new reporting requirements for F&O traders and specific deductions, making timely preparation crucial to avoid compliance risks.

What Happened

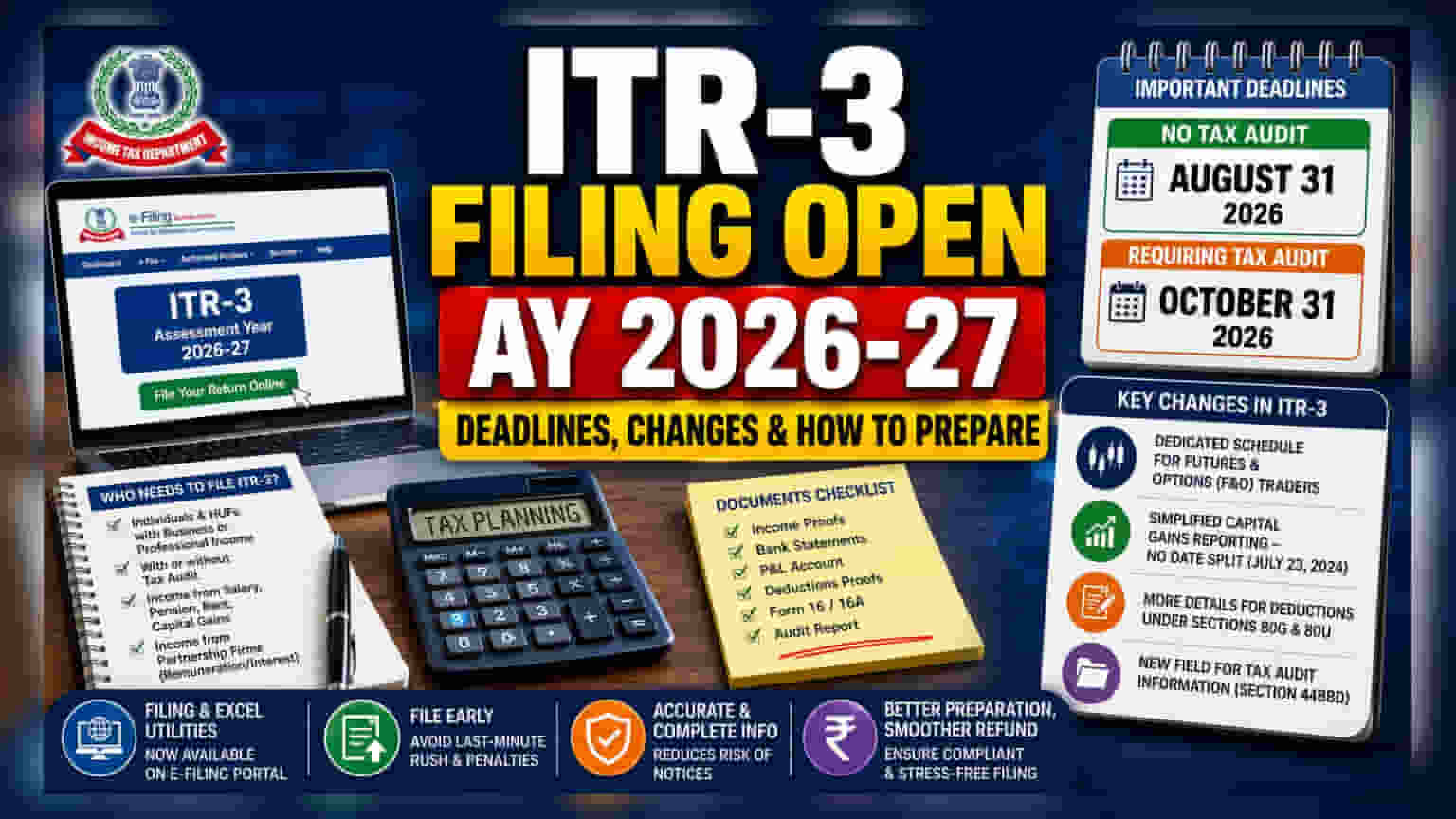

The Income Tax Department has officially released the online filing and Excel utilities for ITR-3 for the Assessment Year (AY) 2026-27. This launch completes the rollout of major tax filing tools for the current assessment year, following earlier releases of utilities for ITR-1, ITR-2, and ITR-4. Taxpayers can now access these tools on the official e-filing portal.

Who Needs to File ITR-3

ITR-3 is the designated form for individuals and Hindu Undivided Families (HUFs) who earn income from business or professional activities. This applies whether the business or profession requires a formal audit or not. The form is comprehensive and covers various income sources, including salary, pension, rental income, and capital gains. Individuals earning from partnership firms, such as remuneration or interest, are also required to use this form for their tax reporting.

Important Deadlines

Compliance with deadlines is a key part of the tax filing process. For taxpayers who do not require a tax audit, the deadline to submit the ITR-3 return is August 31, 2026. For those who are subject to a mandatory tax audit, the filing deadline is extended to October 31, 2026. Keeping track of these dates is important to avoid potential penalties or late fees.

Key Changes and What to Watch

This year's ITR-3 includes several updates that taxpayers should be aware of before filing. One of the most significant changes is the introduction of a dedicated reporting schedule for Futures and Options (F&O) traders. This shift suggests a move toward more transparent reporting for stock market traders using derivative instruments.

Additionally, there have been adjustments regarding how capital gains are reported. The requirement to distinguish between capital gains transactions based on the date of July 23, 2024, has been removed, simplifying that section. Taxpayers planning to claim specific deductions, such as those under Section 80G for donations or Section 80U for disability, must now provide more detailed information. The form also includes a new field for capturing tax audit information as per Section 44BBD.

How to Prepare Your Filing

Preparation is essential for a smooth filing process. Taxpayers are advised to gather all necessary financial documents and income records well before the deadline. Providing accurate and granular information, especially for deductions and business-related income, can help reduce the chances of receiving notices for further clarification.

Starting the process early allows for enough time to reconcile bank statements and profit-and-loss accounts with the figures being reported. Taking a systematic approach to filing helps in maintaining compliance and ensures that refunds, if any, are processed without unnecessary delays or scrutiny. When in doubt, taxpayers should ensure their documentation is complete and verifiable.