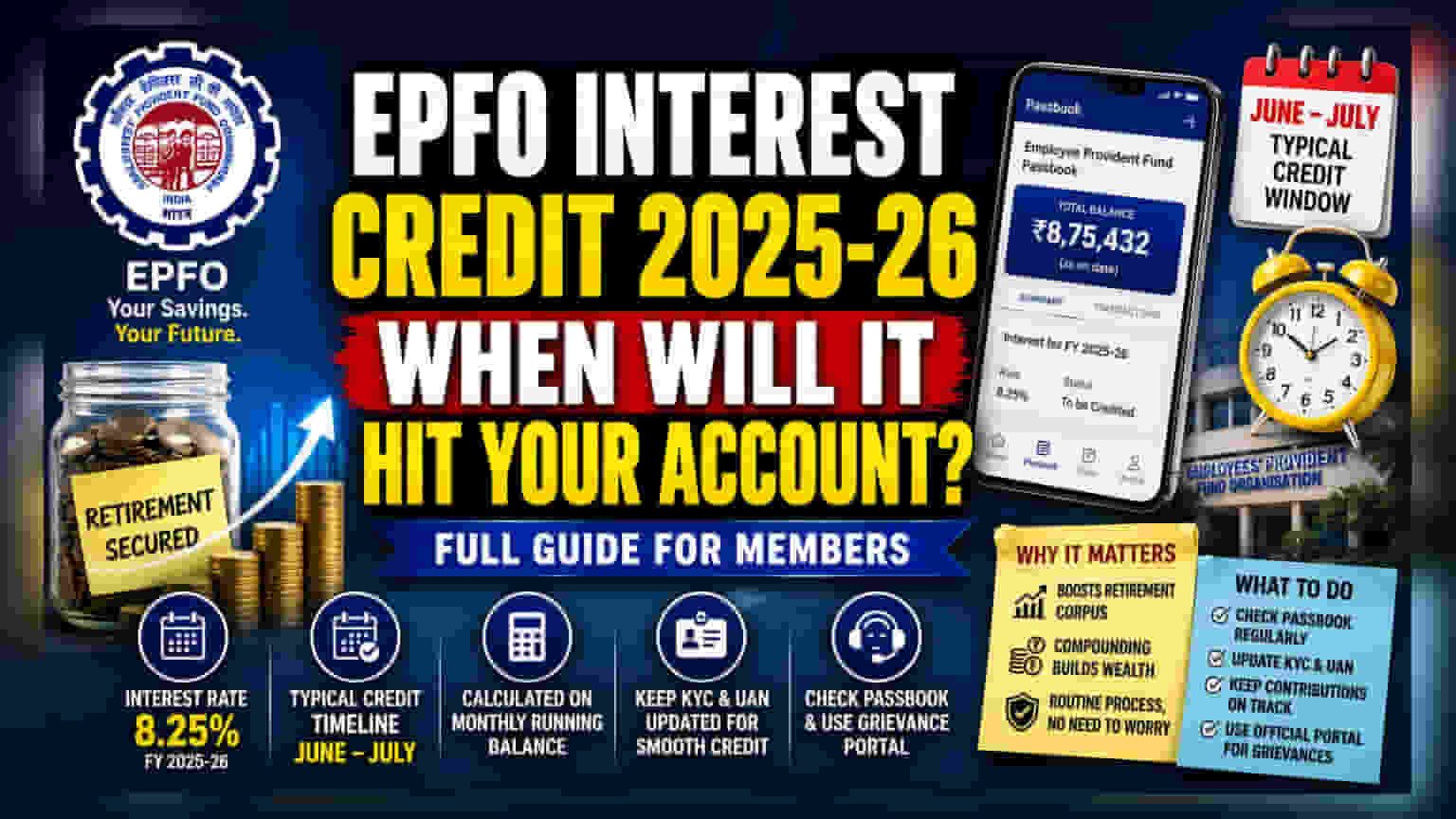

What Happened

Employees’ Provident Fund Organisation (EPFO) subscribers are currently awaiting the interest credit for the fiscal year 2025-26. The Central Board of Trustees had finalized an 8.25% interest rate for the period in early March. As of June 2026, members are looking for this interest to be reflected in their individual passbooks. This is a common annual event, and the absence of the credit in accounts at this stage of the year is part of the standard operational timeline rather than an indicator of financial trouble.

Why This Matters For Subscribers

For millions of salaried individuals, the EPF acts as a core component of retirement planning. The interest credited annually is a major driver of compounding wealth over the long term. When account balances do not reflect the expected interest, it can create confusion regarding the actual savings amount. Understanding that this is a routine administrative process can help subscribers avoid unnecessary concern regarding their retirement corpus.

Understanding the Credit Timeline

Historically, the EPFO typically credits interest between June and July. While technology has significantly improved the speed of these updates compared to several years ago—when credits sometimes appeared as late as September or October—the system still requires time for government approvals and massive account reconciliations. The process involves updating millions of individual accounts, which requires careful verification by the system to ensure accuracy.

The Calculation Method

Interest on the EPF is calculated based on the monthly running balance, rather than just the final year-end balance. This means the interest is accrued throughout the year on the funds present in the account each month. If a subscriber notices a difference between their expected and actual interest, it is rarely due to a calculation error. Common reasons for perceived gaps include delayed contributions from employers, periods where the account was inactive, or incomplete balance transfers when changing jobs.

Keeping Accounts Healthy

To ensure there are no interruptions in the interest credit process, maintaining accurate and updated records is essential. This includes ensuring that the Universal Account Number (UAN) is correctly linked to the active Aadhar and that all KYC documentation is current. If a claim is rejected, it does not mean the earned interest is lost; the account continues to accrue interest regardless of procedural hurdles. Once documentation errors, such as name mismatches or incorrect dates, are corrected, the claim can be resubmitted.

What Investors Should Track

Subscribers may regularly monitor their EPF passbooks through the official UAN member portal or the mobile application. If there is a genuine concern regarding a missing credit or a specific account discrepancy, it is helpful to keep records of contribution history, including salary slips that show the PF deductions. For resolving specific issues, the official grievance portal remains the primary channel for filing complaints. The focus for members at this time should be on ensuring administrative details like KYC are fully updated to allow the system to process the interest credit without manual intervention or delays.